The November U.S. presidential election could be contentious, yet the bitcoin market is pricing little event risk. Analysts, however, warn against reading too much into the complacency suggested by the volatility metrics.

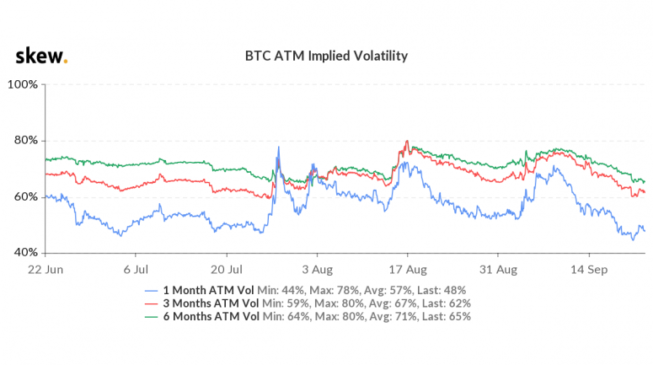

Bitcoin’s three-month implied volatility, which captures the Nov. 3 election, fell to a two-month low of 60% (in annualized terms) over the weekend, having peaked at 80% in August, according to data source Skew. Implied volatility indicates the market’s expectation of how volatile an asset will be over a specific period.

The one- and six-month implied volatility metrics have also come off sharply over the past few weeks.

The declining price volatility expectations in the bitcoin market cut against growing fears in traditional markets that the U.S. election’s outcome may not be decided for weeks. Traditional markets are pricing a pickup in the S&P 500 volatility on election day and expect it to remain elevated in the event’s aftermath.

“Implied volatility jumps around election day, pricing an S&P 500 move of nearly 3%, and the term structure remains elevated well into early 2021,” analysts at investment banking giant Goldman Sachs recently said.

One possible reason for the decline in bitcoin’s volatility expectations ahead of the U.S. elections could be the leading cryptocurrency’s status as a global asset, said Richard Rosenblum, head of trading at GSR. That makes it less sensitive to country-specific events.

“The U.S. elections will have relatively less impact on bitcoin compared to the U.S. equities,” said Richard Rosenblum, head of trading at GSR.

Implied volatility distorted by option selling

Crypto traders have not been buying the longer duration hedges (puts and calls) that would push implied volatility higher. In fact, it seems the opposite has happened recently. “In bitcoin, there has been more call selling from overwriting strategies,” Rosenblum said.

Call overwriting involves selling a call option against a long position in the spot market, where the strike price of the call option is typically higher than the current spot price of the asset. The premium received by selling insurance (or call) against a bullish move is the trader’s additional income. The risk is that traders could face losses in the event of a sell-off.

Selling options puts downward pressure on the implied volatility, and traders have recently had a strong incentive to sell options and collect premiums.

“Realized volatility has declined, and traders holding long option positions have been bleeding. And to stop the bleeding, the only option is to sell,” according to a tweet Monday by user @JSterz, self-identified as a cryptocurrency trader who buys and sells bitcoin options.

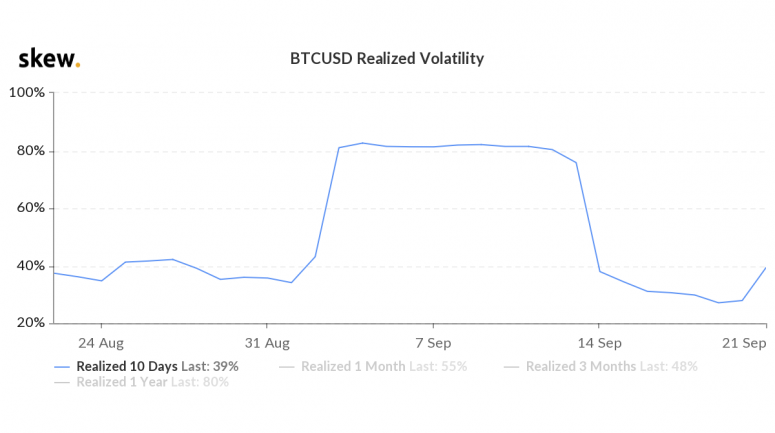

Bitcoin’s 10-day realized volatility, a measure of actual movement that has occurred in the past, recently collapsed from 87% to 28%, as per data provided by Skew. That’s because bitcoin has been restricted mostly to a range of $10,000 to $11,000 over the past two weeks.

A low-volatility price consolidation erodes options’ value. As such, big traders who took long positions following Sept. 4’s double-digit price drop may have sold options to recover losses.

In other words, the implied volatility looks to have been distorted by hedging activity and doesn’t give an accurate picture of what the market really expects with price volatility.

Moreover, despite the explosive growth in derivatives this year, the size of the bitcoin options market is still quite small. On Monday, Deribit and other exchanges traded roughly $180 million worth of options contracts. That’s just 0.8% of the spot market volume of $21.6 billion.

Activity concentrated at the front-month contracts

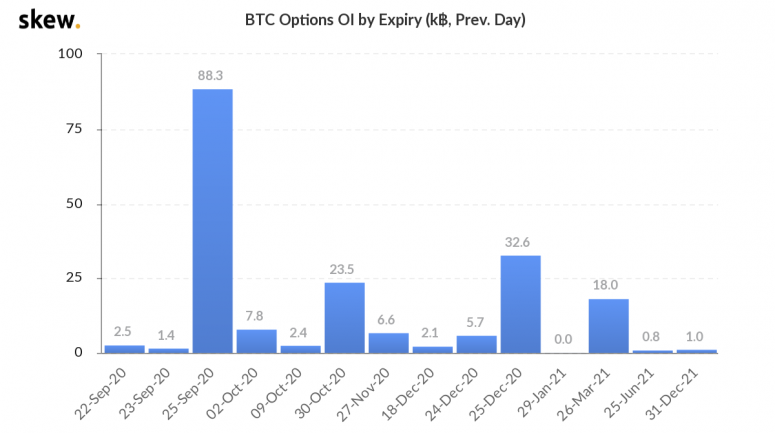

The activity in bitcoin’s options market is primarily concentrated in front-month (September expiry) contracts.

Over 87,000 options worth more than $1 billion are set to expire this week. The second-highest open interest (open positions) of 32,600 contracts is seen in December expiry options.

With so much positioning centered around the front end, the longer-duration implied volatility metrics again look unreliable. Denis Vinokourov, head of research at the London-based prime brokerage Bequant, expects re-pricing the U.S. election risk to happen following this week’s options expiry.

Spike in volatility does not imply a price drop

A re-pricing of event risk may happen next week, said Vinokourov. Still, traders are warned against interpreting a potential spike in implied volatility as an advance indicator of an impending price drop as it often does with, say, the Cboe Volatility Index (VIX) and the S&P 500. That’s because, historically, bitcoins’ implied volatility has risen during both uptrends and downtrends.

The metric rose from 50% to 130% during the second quarter of 2019, when bitcoin rallied from $4,000 to $13,880. Meanwhile, a more significant surge from 55% to 184% was observed during the March crash.

Since that massive sell-off in March, the cryptocurrency has matured as a macro asset and could continue to track volatility in the stock markets and U.S. dollar in the run-up to and post U.S. elections.