With the wild journey that is bitcoin price swings so far this year, you might have missed the accelerating rhythm of companies announcing services to support bitcoin for payments.

We’re not talking about small idealistic startups, either.

A week ago, on Visa’s Q1 earnings call, CEO Al Kelly said the company may add cryptocurrencies to its payments network. He acknowledged that bitcoin is “not used as a form of payment in a significant way at this point,” but went on to discuss a strategy to “enable users to purchase these currencies using their Visa credentials or to cash out onto our Visa credential to make a fiat purchase at any of the 70 million merchants where Visa is accepted globally.”

You’re reading Crypto Long & Short, a newsletter that looks closely at the forces driving cryptocurrency markets. Authored by CoinDesk’s head of research, Noelle Acheson, it goes out every Sunday and offers a recap of the week – with insights and analysis – from a professional investor’s point of view. You can subscribe here.

Visa also currently provides credit card infrastructure for 35 crypto companies, with the aim of making it easier for users to pay with bitcoin.

In PayPal’s Q4 earnings call this week, the first since the company started allowing the purchase and sale of a handful of cryptocurrencies via their PayPal account, the company revealed that it was planning to start allowing customers to use their crypto balances to pay for goods and services at any of the approximately 29 million merchants on the network, and that it was “significantly investing” in the crypto business unit.

Large crypto companies are also moving into payments. Last month, crypto exchange and custodian Gemini launched a credit card with a 3% reward on purchases. In December, crypto lender BlockFi announced that it would launch a similar product in early 2021.

This is just scratching the surface. Binance, Coinbase, Paxful and BitPanda are just some of the crypto exchanges that over the past few months have introduced crypto debit cards for retail spending. This week, crypto platform Uphold announced the acquisition of card issuer Optimus Cards U.K.

Also this week, Binance, the largest cryptocurrency exchange in the world in terms of volume, announced the launch of a payments system called Binance Pay, aimed at encouraging the use of crypto in cross-border payments. Binance CEO and founder Changpeng “CZ” Zhao said: “We think that payments is one of the most obvious use cases for crypto.”

Not so fast

Obviously “crypto” encompasses a range of assets, but let’s focus on Bitcoin for a moment.

The white paper that introduced Bitcoin to the world in 2008 opens with:

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.”

Whether Satoshi Nakamoto, the pseudonymous writer of the paper, meant for payments to be the main use case or not (this is a point of contention, as he* also wrote elsewhere about its potential role as a store of value), over the years it became clear that scaling limitations inherent in the protocol design made the network impractical for high transaction volumes.

(*I am not assuming Satoshi is a he, but I am using this pronoun to avoid linguistic clutter.)

Another critique of Bitcoin-as-a-payments rail is its relative lack of speed, although this can be misleading. A bitcoin payment will take around 10 minutes on average, and up to an hour for assumed settlement finality. Credit card and contactless payments are faster, but they usually don’t have settlement finality until days later. And data gathered in electronic transactions removes any financial privacy. Cash, on the other hand, is instantaneous and private, but you need to be physically present.

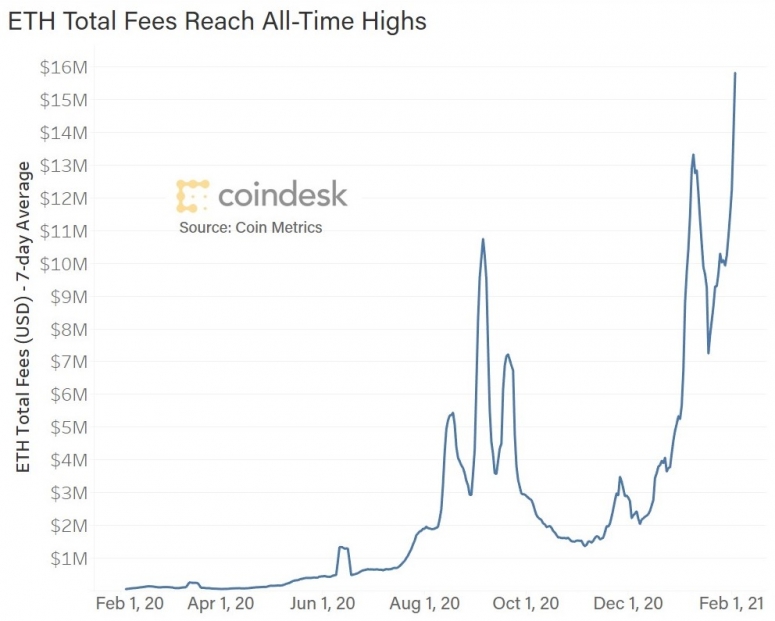

What’s more, bitcoin transactions are relatively expensive. This week the average fee reached its highest point since January 2018.

Solutions such as the Lightning Network aim to solve for these barriers by offering fast and cheap throughput on a transaction layer that anchors to the Bitcoin blockchain at certain intervals. Adoption of this technology is growing, but is still in its early stages.

The existential question

Then again, most of those that complain that Bitcoin doesn’t work for payments have access to other mechanisms that work well. That’s not the case for much of the world. Some jurisdictions have strict capital controls that block payments to other regions. Some countries don’t have sophisticated payment rails that make even simple internal transfers easy. Even some demographic groups in developed countries don’t have access to online payments and are still largely dependent on bank relationships.

For many, bitcoin is a tool for freedom in that it facilitates online payments where previously they were inaccessible. For others, using bitcoin is a way to support the network by giving the asset a broader utility.

This raises an important question: should bitcoin be encouraged to be both a store of value and a payments mechanism?

Some reasons why it should:

It can be argued that bitcoin’s worth as a store of value depends on its utility. The more there is residual demand for bitcoin as a payment token, regardless of its price, the more investors will believe that demand for it will rise in a sustainable way.

It can also be argued that it is essential for the health of the network that bitcoin’s use as a medium of exchange be encouraged. As successive halvings reduce the block subsidy (in which miners get new bitcoin as compensation for the work expended in successfully processing blocks of transactions), miner incentives will increasingly rely on transaction fees.

And current demand for this use case is not insignificant. Binance Research this week published the results of a survey of 16,000 crypto users across 178 regions, which found that 38% see bitcoin as a medium of exchange. In December, Susquehanna Financial Group revealed a survey of PayPal customers that showed 53% would use bitcoin to pay for goods, if they owned it.

Some reasons why it shouldn’t:

There is a not totally unfounded concern that, if bitcoin becomes seen by governments as a widely used payment token and a potential threat to fiat currencies, they may decide to act, and not in bitcoin’s favor.

While it may seem that governments care more about markets and asset prices, it’s payments that matter for monetary policy, consumption and wages – all things that get you votes. Investments sit there (and hopefully grow) while payments move, and both animal and regulatory instinct is to focus more on things that move.

In addition, you have the theory that if bitcoin is seen as a store of value, it will not be spent. Gresham’s Law dictates that bad money crowds out the good – if bitcoin is “good” money, people are more likely to hold onto it, and use other assets with less potential value.

The endgame?

This segues into what is perhaps the endgame of many of the crypto payments providers.

It’s perhaps not about Bitcoin at all.

Bitcoin is the crypto asset with the least regulatory uncertainty at the moment. Even stablecoins are not totally out of the regulatory woods yet. (The OCC’s letter that said banks could handle stablecoins could be walked back under a new chief.)

So, maybe Bitcoin is the safe starting point for these new rails. Ethereum will probably come next, and where Ethereum goes, so do stablecoins.

Maybe the banks and payment companies working on bringing crypto payments services mainstream have their eyes on a potentially bigger pie – that of tomorrow’s payments, the bulk of which could run on blockchains that handle a range of assets. Maybe the forward-thinking institutions are preparing for a day when we hold cryptocurrencies in our digital wallet right along with our private stablecoins and our digital dollars and our tokenized GameStop shares.

Maybe they’re all looking at a financial landscape where the user has more choice.

The crypto payment functions today serve their purpose. They offer a useful service to many, nudge along the sophistication of market infrastructure, and set the scene for mainstream adoption of a range of assets with a range of utilities.

And with more choice, it is more likely that the market will decide whether Bitcoin is a good payment rail or not. With each new service, we experiment with market adoption, and we learn more about what today’s and tomorrow’s users will value. I’m all for bringing on more experimentation.

CHAIN LINKS

This interview, in which MicroStrategy CEO Michael Saylor interviews NYDIG CEO Ross Stevens, is a must-see.

Chief economist and managing director of CME Group Bluford Putnam said that his firm has begun to notice gold’s waning appeal as a hedge against global political risk, and that he believes bitcoin is an “emerging competitor” to gold.

Visa is piloting a suite of APIs that will allow banks to offer bitcoin services such as buying, selling and custody, with a view to extending the service to include other cryptocurrencies and stablecoins. TAKEAWAY: Initiatives like this (last month, NYDIG made a similar announcement) are a step towards mainstream adoption of cryptocurrencies. The “endorsement” of traditional banks, while far from the original ethos of the industry, will go a long way toward encouraging trust in the concept from mainstream clients. This could encourage new investment in the space, both from investors and small savers as well as from startups working on improving market and payment infrastructures.

New York-based crypto exchange and custodian Gemini is now offering deposit accounts with a 7.4% APY, via a partnership with Genesis Capital (owned by DCG, also parent of CoinDesk). TAKEAWAY: The “bankification” of crypto exchange platforms is gathering steam. Gemini is a crypto asset trading platform, stablecoin issuer, credit card issuer and now also an interest-bearing deposit taker. The yield offered is sufficiently higher than traditional deposit yields and so should attract attention, perhaps even serving as an onramp into crypto asset markets.

Bitwise Asset Management has applied to publicly trade shares of its bitcoin fund on the OTCQX marketplace. TAKEAWAY: The fund aims to compete with market leader GBTC (managed by Grayscale Investments, owned by CoinDesk parent DCG), which quotes on the same exchange. GBTC’s premium to underlying value has dropped over the past few days to around 10%, from a three-month high of around 40% in mid-December. More competition should keep the premium down, giving retail investors a better deal as well as more choice. GBTC’s $24 billion market leadership position will be hard to assail, however.

We saw above in THE BRIEFING that BTC transaction fees are increasing. ETH transaction fees are spiking even more. TAKEAWAY: This reflects the ETH price increase as well as growing demand for stablecoins and decentralized finance tokens. In spite of increasing fees, transaction volume also continues to rise. (For background on Ethereum’s gas costs, see our recent metrics report.)

Cryptocurrency investment firm Arcane Crypto (ARCANE) is now listed on Sweden’s Nasdaq First North following a reverse takeover of Vertical Ventures AB. TAKEAWAY: With this, Arcane joins the growing roster of listed crypto companies, and is one of the few broad industry plays (as opposed to pure funds or market infrastructure plays) to have a transparent market valuation (approximately $200 million at listing).

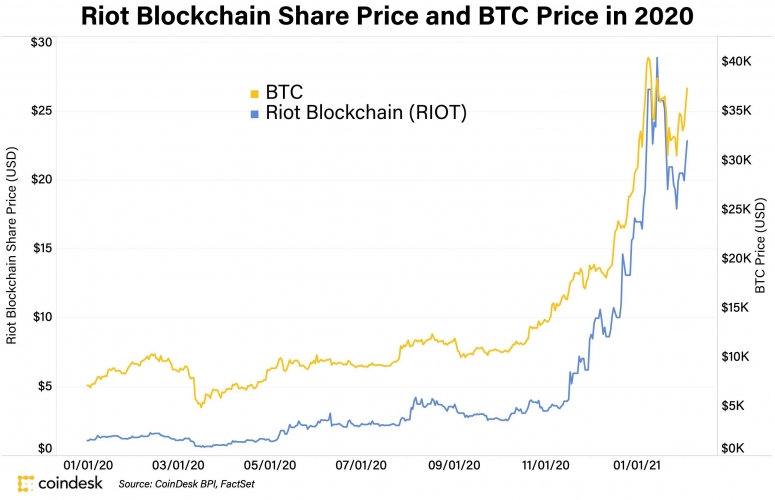

CalPERS, the largest public pension fund in the U.S., increased its stake in bitcoin miner Riot Blockchain (RIOT) nearly sevenfold over the last quarter, to $1.9 million at year-end price. TAKEAWAY: This highlights that direct ownership is not the only way to play BTC exposure. RIOT’s share price has moved up with BTC, but since Sept 30, 2020, has produced a return of over 750% vs BTC’s 250%.

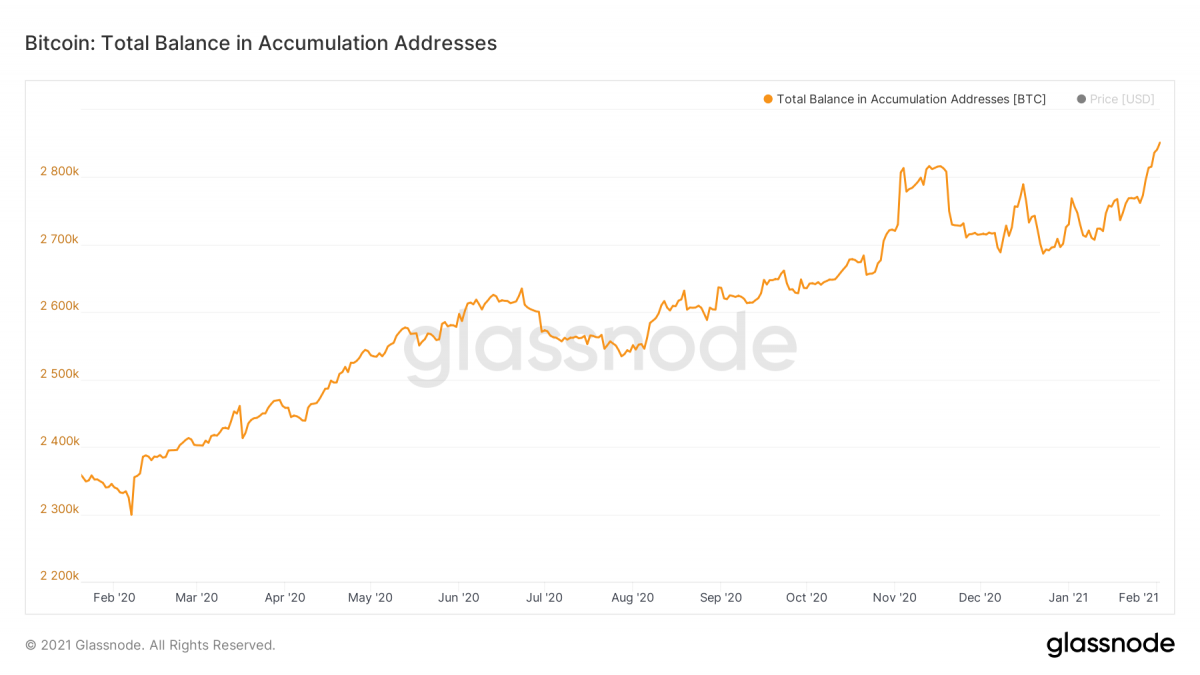

The total balance of BTC held in “accumulation addresses,” which have at least two incoming transfers over the past seven years and have never spent funds, has reached a 3.5-year high of over 15% of the total circulating supply. TAKEAWAY: As more investors buy to hold, more bitcoin is removed from circulation, which supports further price rises as new demand comes in. This type of detail is one of my favorite things about crypto asset metrics – imagine if we had this level of insight into investor behavior with traditional assets.

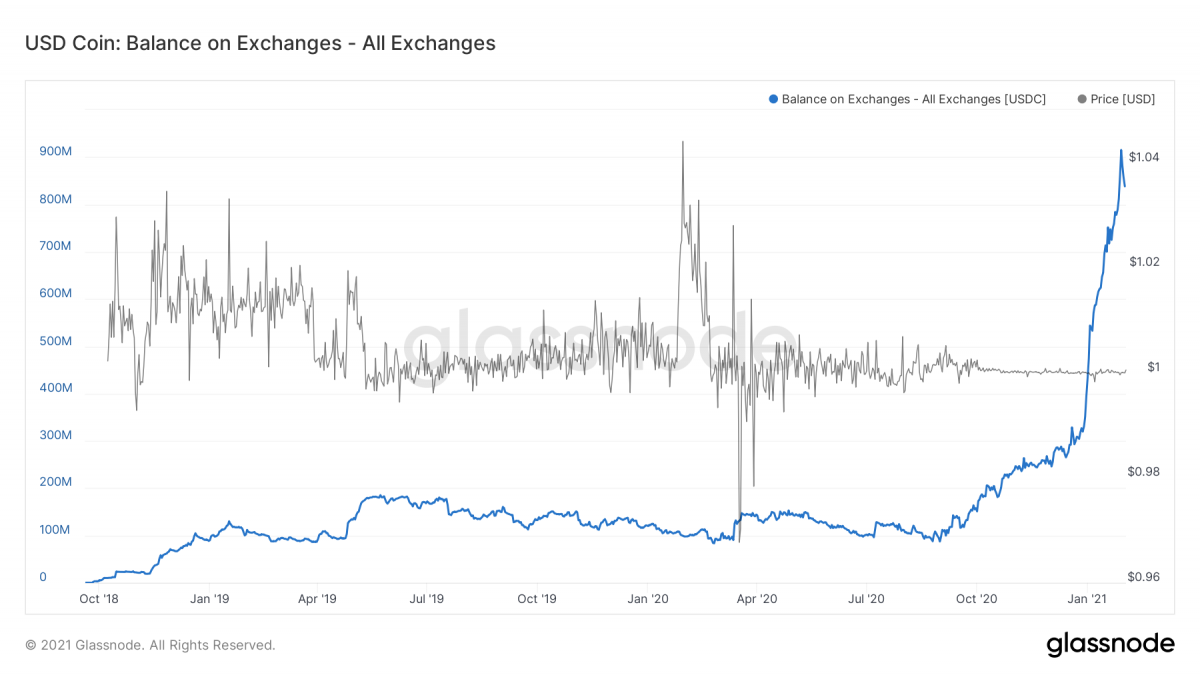

The amount of stablecoin USDC held on exchanges has soared since the beginning of the year, hinting at institutional intention to buy. TAKEAWAY: The balance of stablecoins on crypto exchanges is watched as a signal for investor intent. It does not, however, indicate which asset(s) the buyers will favor, nor is it a reliable indicator of institutional interest as many institutions prefer to (or have to) use fiat to invest in crypto assets.