Matthew Trudeau is chief strategy officer at crypto asset exchange ErisX. The opinions expressed in this article are the author’s own.

The following article originally appeared in Institutional Crypto by CoinDesk, a free newsletter for institutional investors interested in crypto assets. Sign up here.

Recently CoinDesk published an article titled, ‘High Frequency Trading is Newest Battle Ground in Crypto Exchange Race’ that discusses trading venues offering direct connectivity to their matching engines.

While ErisX has only recently launched its spot market, other crypto exchanges announced their intention to and/or began to enable trading firms to cross-connect (a direct network connection within the data center as opposed to a connection routed over the internet) to their matching engines at least a year ago, so this is not a new development.

Cross-connects are a standard service in global capital markets, utilized across asset classes and market participant types, so the characterization of such connectivity options as “rolling out the red carpet for high frequency traders” is peculiar. Based on the article, none of the exchanges that responded, including ErisX, actually directly offer colocation services (colocation is provided by the datacenter owners/operators).

One of our core views at ErisX is that precision in discussing any important topic is critical, be it institutional interest, custody, etc. so in this piece we are applying the same rigor when discussing “high frequency trading,” “colocation” and “data center-hosted” exchanges vs. “cloud-based” exchanges.

Because ErisX is one of the exchanges mentioned in the article as trying to attract large algorithmic traders with “colocation” offers, we want to more precisely define “algorithmic trading” and “HFT.”

We also want to explain why automated trading can be beneficial to the market and address the distinction, missing in the CoinDesk article, between “cloud” versus “data center-hosted” exchanges and why exchanges hosted in data centers present superior performance and benefits to market participants.

Defining HFT

High frequency trading (HFT) has been a topic of debate in large part because of a lack of precision and/or understanding by commentators even in traditional markets. There are different kinds of “HFT” but for this post we will define it as automation of trading strategies enabled by computers to transact a large number of orders in fractions of a second.

Leveraging algorithms, high frequency traders analyze market conditions to manage risk and execute orders based on predefined trading strategies. Blackrock, a global investment management company, did an excellent job of further distinguishing a taxonomy of HFT strategies along with their relative impact on market quality in a 2014 whitepaper US Equity Market Structure: An Investor Perspective.

We would add to the taxonomy in the graphic below a fifth category of fraudulent or manipulative strategies that are prohibited in other markets, are not limited to HFT, and have been shown to exist, although not exclusively, on many crypto exchanges as we discussed in a previous post.

In general, automated market making and arbitrage strategies create greater efficiency in the market as depicted in the above graphic by integrating information into prices more quickly and efficiently resulting in narrower bid/offer spreads, improved price discovery, and fewer and more-fleeting instances of price discrepancies across markets when an asset type, such as bitcoin, trades on multiple venues.

There is evidence that the cryptocurrency markets are experiencing these benefits on the more reputable exchanges as a result of increasing HFT participation.

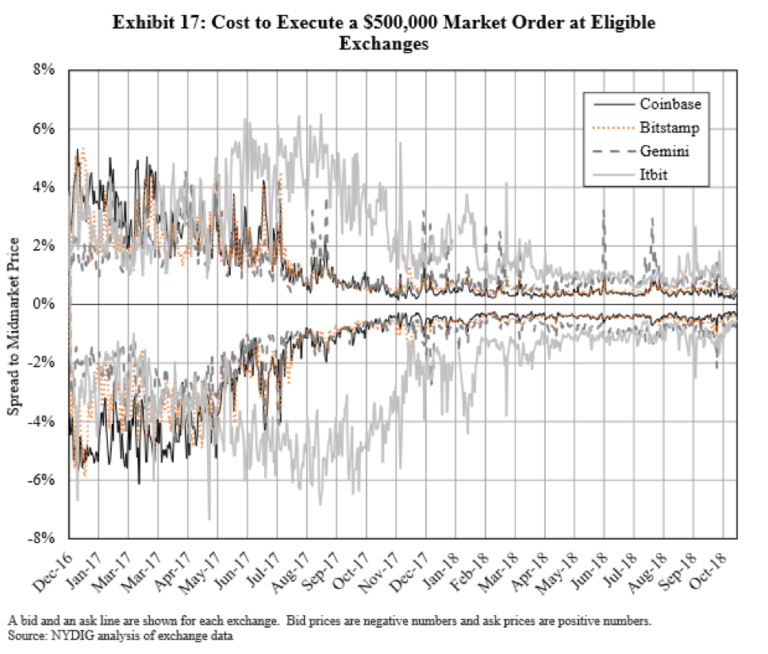

In the past 2.5 years spreads have generally narrowed and become more stable, and price discrepancies across trading venues have become less dramatic and less frequent. The below graphic from a 2019 white paper Buying Bitcoin, published by the New York Digital Investment Group, demonstrates this effect from December 2016 through October 2018.

So, while there are a variety of trading strategies that can be automated and labeled “HFT,” some contribute to market quality while some detract from it.

It is important to note our definition of market quality includes deep liquidity and tight bid/offer spreads, supported by fair access, elimination or appropriate management of potential conflicts of interest, and technology that benefits participants.

Cloud vs Data Center Matching Engine

The CoinDesk article mistakenly states that ErisX has a “hardware matching engine.”

In fact, ErisX has located the hardware (servers etc.) upon which its matching engine software runs in a Tier 1 datacenter facility in New Jersey that services a high density of major financial firms including traditional exchanges, brokers and trading firms as well as communications firms, enabling all new and traditional participants to quickly and efficiently gain access to our markets.

Participants that already have a presence in this datacenter can connect to ErisX’s matching engine via a cross-connect and our FIX API. Additionally, ErisX offers connectivity to its matching engine over the internet via Websocket API.

There is nothing extraordinary about this model. In fact, deploying an exchange in a data center gives exchange operators the greatest control of their entire infrastructure from network firewalls and switches to servers.

This control enables exchange infrastructure to be precision-calibrated to create the most reliable, consistent and performant (lowest absolute latency and variability in latency) experience, promoting fairness amongst market participants. Participants can, in turn, precision-tune their trading systems and automated trading strategies; market participants that host their trading infrastructure in a datacenter (vs. the cloud) benefit from the same level of control and precision tuning. This is a good thing.

In contrast, cloud-based exchanges have less control over their infrastructure managed by the cloud operator in a shared general-purpose environment, and as a result cannot yet achieve the same level of reliability and performance offered by data center hosted exchanges.

To illustrate, at the risk of getting into the technical weeds, a world-class data center-hosted exchange may offer round-trip latency in the sub-100 microseconds (millionths of a second) range with 99th percentile consistency and the capability to process millions of orders per second, all with 99.99 percent uptime.

Cloud-based exchanges, on the other hand, may offer latency in the tens or hundreds of milliseconds (a thousand times slower) with less reliability, consistency and throughput due to the vagaries of internet routing algorithms. Further, cloud-based exchanges may rotate the location of the system running their matching engine periodically from one cloud datacenter to another, introducing even greater latency and inconsistency.

Low and predictable latency enables market participants to better manage their risk and pricing algorithms to ensure their best possible quotes are posted to exchanges creating high quality liquidity. In contrast, long round-trip order/quote/trade times resulting from high, unpredictable latency do not allow participants to react as fast to rapidly evolving market conditions. To compensate, participants may quote wider markets and thinner liquidity.

The CoinDesk article implies that by hosting in the cloud, exchanges create a fairer access model and/or protect retail investors. In fact, wider spreads and thinner liquidity are a detriment to all investors. The article also overlooks the reality that clouds run in data centers, and latency-sensitive market participants can locate their automated trading systems within, or close to the cloud data centers with or without explicit approval from exchanges – essentially unsanctioned “colocation.”

These firms access cloud exchanges faster than other participants, just with less reliability and determinism than with a data center-hosted exchange.

Conclusion

Automated market making and arbitrage, both forms of “high frequency trading” strategies, contribute to higher quality liquidity and markets, and the performance offered by data center-hosted exchanges enables these strategies to better manage risk and react to fast-moving markets.

In conclusion, we believe that constructive automated strategies and data center-colocated exchanges provide fair and consistent market performance with benefits for all participants.

Money counter via Shutterstock