The bigger you are, the bigger the splash when you jump in the water. And when it comes to mainstream payments companies, there are few bigger than PayPal.

In case you’ve been totally avoiding the headlines over the past few days (and who could blame you), PayPal (NASDAQ: PYPL) this week confirmed its entry into the crypto asset industry with the announcement that it was enabling the buying, selling and holding of cryptocurrencies on its platform. Within the next few weeks, users in the U.S. will be able to trade bitcoin (BTC), ether (ETH), litecoin (LTC) and bitcoin cash (BCH) using their PayPal accounts. The service will be rolled out to Venmo, a PayPal company, and to other geographical areas in the first half of next year. Users will also be able to use these cryptocurrencies to purchase goods at 26 million merchants within the PayPal network.

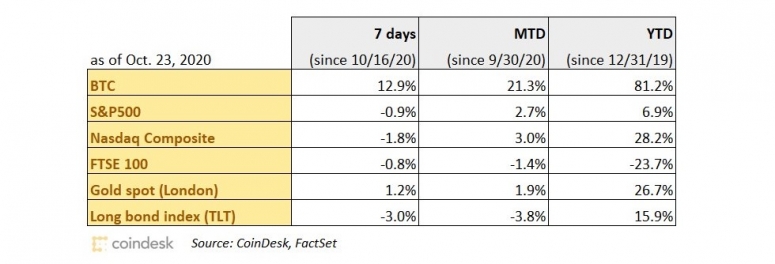

The market took it as good news, evidenced by the almost 15% increase in the BTC price (at time of writing) since the announcement was made. The other cryptocurrencies supported by PayPal also saw weekly returns of 10-15%.

A cheerful rally is generally good news, and this one seems to have energized a market that had been slipping into sentiment doldrums. Indeed, the PayPal news is positive for the industry as a whole. But the news is not the boost to the fundamental outlook for bitcoin and peers that many market observers seem to think.

Looking beyond the numbers

First, the news is not a surprise. We reported on this a few months ago, later adding that the actual cryptocurrency trading would be handled by Paxos.

What’s more, the details that have been added to our reporting are disappointing.

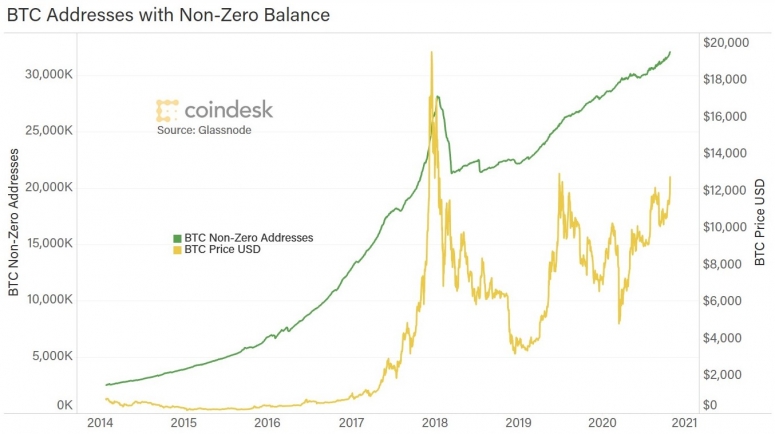

PayPal does bring over 340 million users to the crypto table. For context, Bitcoin currently has 32 million non-zero addresses (only 5 million of which are active), according to data firm Glassnode. But PayPal’s crypto users would not necessarily add to the address count, as they would not have access to their own private keys. What’s more, users will not be able to transfer their crypto holdings out of their PayPal account, nor will they be able to send crypto to other PayPal users. In other words, PayPal more or less dictates what users can do with their cryptocurrencies, and could presumably freeze accounts if they see fit, at least for now – not exactly in line with the industry’s origin and ethos.

Another aspect that has many excited is the network of 26 million merchants at which users will be able to spend their cryptocurrencies, with PayPal handling the fiat-crypto conversion. Over the years, however, the “buying stuff with crypto” use case has attracted relatively little attention, as the investment use case became more predominant. Why would people spend an investment asset, forgoing any potential gain? True, in some countries it might be easier to pay via PayPal using bitcoin, for instance, than dollars. But just because the service is now available does not mean that people will use it in significant numbers.

Got the blues

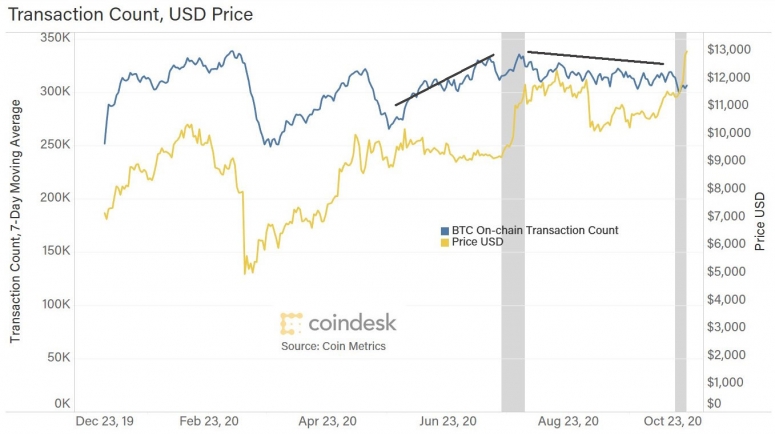

On top of the disappointing details, the rally burst into life amid relatively bearish sentiment. For context, it helps to compare this week’s rally with the sharp price spike at the end of July of this year, when BTC rose almost 30% over 10 days.

In the weeks prior to the July rally, the transaction count on the Bitcoin network had been rising, indicating growing activity. In the weeks preceding this rally, the transaction count was sloping down.

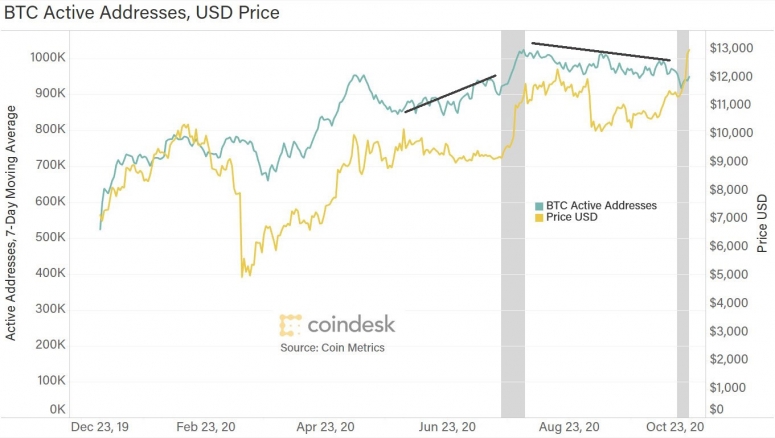

In a similar vein, the number of active addresses on the Bitcoin network was increasing into the July rally, but was decreasing at the time of this week’s jump.

Both metrics hint at declining network activity, perhaps a result of dwindling trader and investor interest given the relatively narrow band in which the price had been hovering.

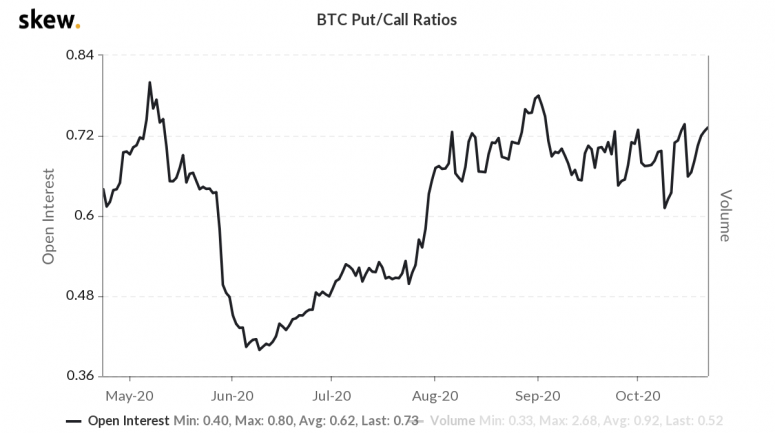

The derivatives markets also indicated some bearish sentiment, with the funding rate for bitcoin perpetual futures turning negative at the beginning of September. A negative funding rate implies more short positions than long ones. In contrast, the funding rate had been mostly positive since early summer when the July rally began, indicating a more positive outlook for the market on the part of traders and investors.

Tailwinds accumulating

However, crypto markets react quickly, and the above metrics are adjusting as we speak. As we have seen, sentiment can turn on a dime, totally changing market indicators in a FOMO-fueled frenzy of catching up. The different “mood” heading into this rally could in part explain the rapid rise of asset prices as traders caught unawares scrambled to adjust positions. It could also mean that the rally could be short-lived, as the PayPal novelty wears off and the bearish sentiment returns.

The nature of the bearish sentiment, though, and the bigger implications of PayPal’s announcement, indicate otherwise.

The waning interest of the past few weeks seems to have been more a result of boring price action than negative fundamentals. Indeed, the case for investment in bitcoin has been gaining momentum with inflation concerns encouraging not just traditional fund managers but also corporate treasurers to hedge against fiat debasement.

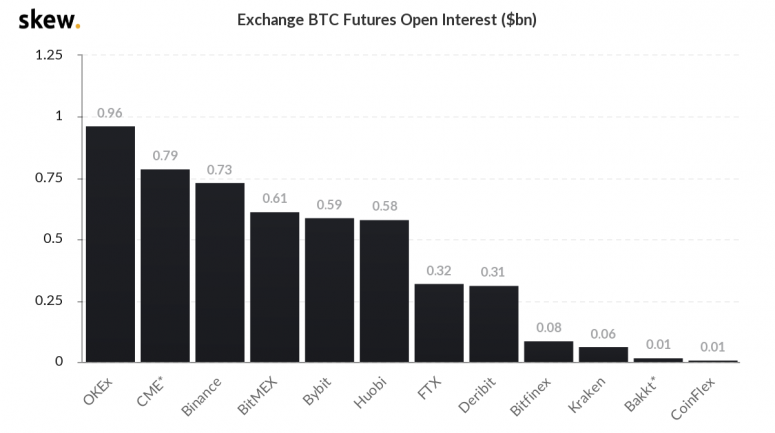

In the derivatives markets, institutional activity has been steadily building. The Chicago Mercantile Exchange (CME), the largest U.S.-regulated crypto derivatives venue and often taken as a proxy for institutional involvement, now boasts the second-highest amount of open interest in BTC futures in the market – just three months ago, it was fourth.

And the number of non-zero addresses on the Bitcoin network, an indicator of adoption, continues to reach all-time highs.

Now the important part

Perhaps even more significant than these and other market indicators that point to a quiet accumulation of interest is the message that the PayPal news sends.

It’s not so much that a company which a few years ago froze accounts dealing in cryptocurrency is now wholeheartedly embracing the concept. PayPal is far from the only corporation to realize that it was wrong. It’s more that a member of the Fortune 500 is publicly endorsing the concept of cryptocurrency. It’s also that the move puts bitcoin in mainstream headlines without the words “hack,” “ransomware” or “money laundering.” This is big-time public validation from a household name.

Yet the underlying message is even bigger, and this is the part that I find most intriguing: PayPal is signaling that a digital currency world is inevitable.

The functionality of its cryptocurrency service may be limited for now – but it is not necessarily going to stay that way. PayPal has authorization to transact in cryptocurrency on behalf of its clients in 49 states, but there are no doubt many more regulatory hoops to jump through before the service can comply with KYC/AML rules on a global basis. We can assume it is working on these. We can also assume that it will iterate its service in response to customer feedback and actual revenue figures. And the company is apparently exploring the acquisition of other crypto companies, presumably to diversify and support its activity in the crypto space.

Beyond that, it seems that what PayPal is really getting ready for is a financial system that has to juggle not only fiat but also central bank digital currencies (CBDCs). In this, it is not alone.

This week, Japan’s LINE Corporation, best known for its eponymous popular messaging app, revealed that it was working on a platform to support CBDC development. In September, Mastercard (NYSE: MA) announced something similar with a CBDC testing platform. In July, Visa (NYSE: V) hinted that it also was working with global organizations and policy makers to help shape the evolution of CBDCs, which – whatever form they take – will need access to the target users.

This raises an interesting question: Is bitcoin an onramp for CBDCs? I confess I had assumed it would be the other way around. I thought that citizens having to manage blockchain wallets in order to transact in the digital currencies issued by their government would open up new markets for decentralized cryptocurrencies and tokens. PayPal could be signaling that, first, users need to get used to the idea.

Either way, this week’s big announcement feels significant not just for the jolt of energy it has given a lackluster market. It is important for what it hints about what’s coming. Signals from other financial infrastructure and social reach companies are saying the same thing. It’s not the inflow into crypto markets that’s the big deal here.

It’s that finance is changing in front of our very eyes. Fast.

(Note: We use Bitcoin with uppercase when talking about the network, and bitcoin with lowercase, or BTC, when referring to the asset.)

Anyone know what’s going on yet?

In a week of lackluster market moves amid U.S. election concerns, the lack of a stimulus package and an uncertain Q3 reporting season, bitcoin totally shone.

A potential break from traditional market correlation shackles was no doubt partly due to PayPal’s wholehearted embrace of cryptocurrencies. It was also probably the result of a quiet build-up of macro factors that position bitcoin a wise hedge against inflation rather than a risky bet on technology.

CHAIN LINKS

Pioneer hedge fund manager Paul Tudor Jones II said in an interview on CNBC earlier this week that he was more bullish on bitcoin than ever. TAKEAWAY: Bullish statements from investors who are long are to be taken with a grain of salt (of course they have a bullish stance, else they’d probably have sold). But Jones’ comment about the “intellectual capital” behind bitcoin deserves highlighting, as I haven’t heard it mentioned nearly enough. Few understand that bitcoin is more than an alternative asset – it is also an idea that draws from philosophy, economics, sociology, technology and history, pulling in the curious and the innovative who are asking the right questions and feeling their way towards answers that reflect some of the deepest conflicts known to man. The crypto industry is where the smartest minds of today are actively thinking about and building for tomorrow.

A note published this week by JPMorgan’s Global Quantitative and Derivatives Strategy team posits that bitcoin has proven itself to be a risk asset, not a safe have, with “considerable” potential upside. TAKEAWAY: The term “safe haven” has to be one of the most widely misconstrued in all of finance (along with “uncorrelated” and “fair value”). Short term, of course bitcoin is not “safe” – just look at the volatility. It is a hedge against fiat debasement, however, much like gold. The term “hedge” is often erroneously conflated with “safe haven” – gold is often referred to as a safe haven, for example, but at times it is more volatile than the S&P 500. And longer term, hedges can become safe havens. Meanwhile, positioning bitcoin as an either/or thesis does it a disservice. It can occupy many portfolio roles simultaneously. That aside, the note correctly focuses on the millennial generation’s looming influence on the global financial system, their growing interest in bitcoin, and “strong growth” in institutional investor interest.

Bloomberg’s quarterly note on crypto assets posits BTC at $100,000 by 2025. The team also expects the price to break $14,000 soon, possibly this year, and singles out hashrate and active addresses as the metrics to watch for signs of growing adoption. TAKEAWAY: Bloomberg analysts are no doubt extremely qualified and well-informed, but this report reminds me of the saying: “If you’re going to predict, predict often.” In their previous quarterly crypto report, they had $20,000 as the end-of-year price target. That’s not really material, however – what is interesting is that Bloomberg clients obviously want this type of coverage. Interest from traditional investors seems to be getting broader and deeper.

Bitstamp, one of the world’s oldest and largest cryptocurrency exchanges, has introduced an insurance policy that covers the theft and other losses of user funds held on its platform. TAKEAWAY: Insurance has been a thorny subject for crypto exchanges and custodians, as most insurers have shied away from the additional complications and risks involved in insuring bearer assets that run on a new technology. The evolution of crypto asset insurance policies for market infrastructure players underlines the growth of the industry in terms of a broader understanding of crypto businesses and their underlying risks. What’s more, it’s a virtuous circle. Better insurance policies means more robust market infrastructure, which means greater institutional comfort and confidence, which means more incentives to continue improving insurance policies and market infrastructure.

My colleague Omkar Godbole interviewed Philip Gradwell, chief economist at the blockchain intelligence firm Chainalysis, about the numbers that he thinks are essential to understand market sentiment. TAKEAWAY: The five most significant metrics, according to Gradwell, are:

- Exchange inflows (indicates readiness to trade)

- Trade intensity (the number of times an inflowing coin is traded)

- Interexchange flows (hints at institutional involvement by differentiating fiat buyers vs. crypto buyers)

- Liquidity (those that sit on holdings vs. those that circulate them)

- Value transfers across blockchains (speaks to demand for a cryptocurrency)

This sounds like a fun exercise. Excuse me, off to think about what my top five are. (For more of Philip Gradwell’s insights into Bitcoin metrics, check out the recording of our webinar “How to Value Bitcoin: Addresses”.)

Podcast episodes worth listening to

We’re pleased to announce a new podcast series: On Purpose. Hosted by independent registered investment adviser Tyrone Ross, it explores the emerging world of bitcoin and cryptocurrency for the modern financial professional.