During the last few years, cryptocurrencies have been integrated into traditional finance tools like automated teller machines (ATMs), loadable debit cards, point-of-sale devices, and direct payments for all kinds of goods and services. Digital assets have also been added to retirement account offerings issued by financial giants like Fidelity. In recent times, cryptocurrencies can be further capitalized to put a down payment on a mortgage or get a conventional home loan using bitcoin as collateral.

Crypto-Backed Conventional Home Loans

These days, at least in the United States, banks require at least 20% down if a person or a couple wants to purchase a home by leveraging a conventional loan. Typically, people use cash for collateral or a down payment, but Americans can also utilize things like business equipment, inventory, invoices, blanket liens, and even other forms of real estate to secure a traditional mortgage.

As of April 8, 2022, the median home price in the U.S. was $392,000, which means a buyer needs $78,400 in collateral to secure a conventional bank loan. While crypto assets can be utilized to load debit cards and pay for items via point-of-sale commerce, there’s not many firms that allow people to use digital currencies for a crypto-backed loan.

However, there are a couple of companies right now, either offering loans that utilize crypto assets for collateral or that are planning to do so in the near future. Moreover, some firms that planned to offer crypto-backed loans gave up on the idea shortly after.

For instance, the second-largest mortgage lender in the U.S., United Wholesale Mortgage, announced it would accept bitcoin (BTC) for mortgages at the end of August 2021. However, a few months later, United Wholesale Mortgage revealed the company decided not to offer the crypto services.

The company’s CEO, Mat Ishbia, told CNBC in October 2021 that the lender did not think it was worth it. “Due to the current combination of incremental costs and regulatory uncertainty in the crypto space we’ve concluded we aren’t going to extend beyond a pilot at this time,” Ishbia explained to CNBC’s MacKenzie Sigalos.

Crypto-Backed Home Loans Provided by Abra and Milo

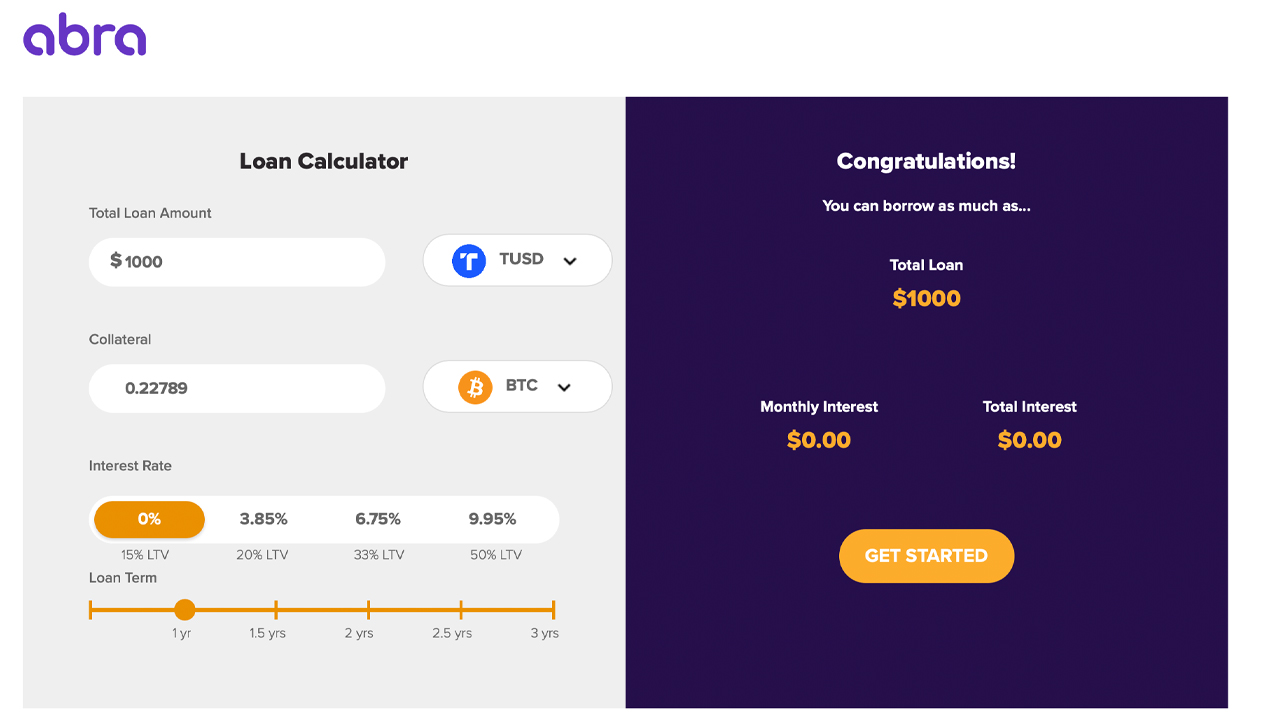

Meanwhile, a financial services firm that just recently announced crypto-backed home loans is the cryptocurrency firm Abra. The company, founded in 2014 by former Goldman Sachs fixed income analyst Bill Barhydt, has provided digital asset trading services and a cryptocurrency wallet for over seven years.

On April 28, 2022, Abra announced it has partnered with the company Propy and homebuyers can secure a home loan using crypto as collateral via the Abra Borrow platform. The Abra lending application has various interest rates, depending on how much crypto collateral is added, from 0 to 9.95%.

“While digital asset investment has skyrocketed, most investors are unable to use their cryptocurrency holdings to directly fund the most important purchase in their life, a home,” Abra’s CEO Bill Barhydt explained during the announcement. “Our partnership with Propy solves this and is a major step in bridging the gap between crypto and real estate,” the Abra executive added.

In addition to Abra, a company called Milo is offering crypto-backed mortgages for people interested in purchasing real estate. Milo is a Florida-based startup that raised $17 million on March 9, 2022, in a Series A funding round. The California-based venture capital firm M13 led the funding round and QED Investors and Metaprop participated.

Milo offers 30-year loans for borrowers looking to leverage up to $5 million. Milo accepts stablecoins, bitcoin (BTC), ethereum (ETH), and interest rates are between 5.95% and 6.95%, with loans that have two to three-week closing times. When Milo raised $17 million last March, Milo CEO Josip Rupena said the company’s efforts aim to enable crypto participants.

“This [funding] round of financing is a validation of Milo’s vision to empower global and crypto consumers and the opportunity to bridge the digital world with real-world real estate assets,” Rupena said at the time. “This is a multibillion-dollar opportunity, and we are proud to be pioneering the efforts in the U.S. for consumers that have unconventional wealth.”

Ledn and Figure Technologies Plan to Offer Crypto-Backed Mortgage Products

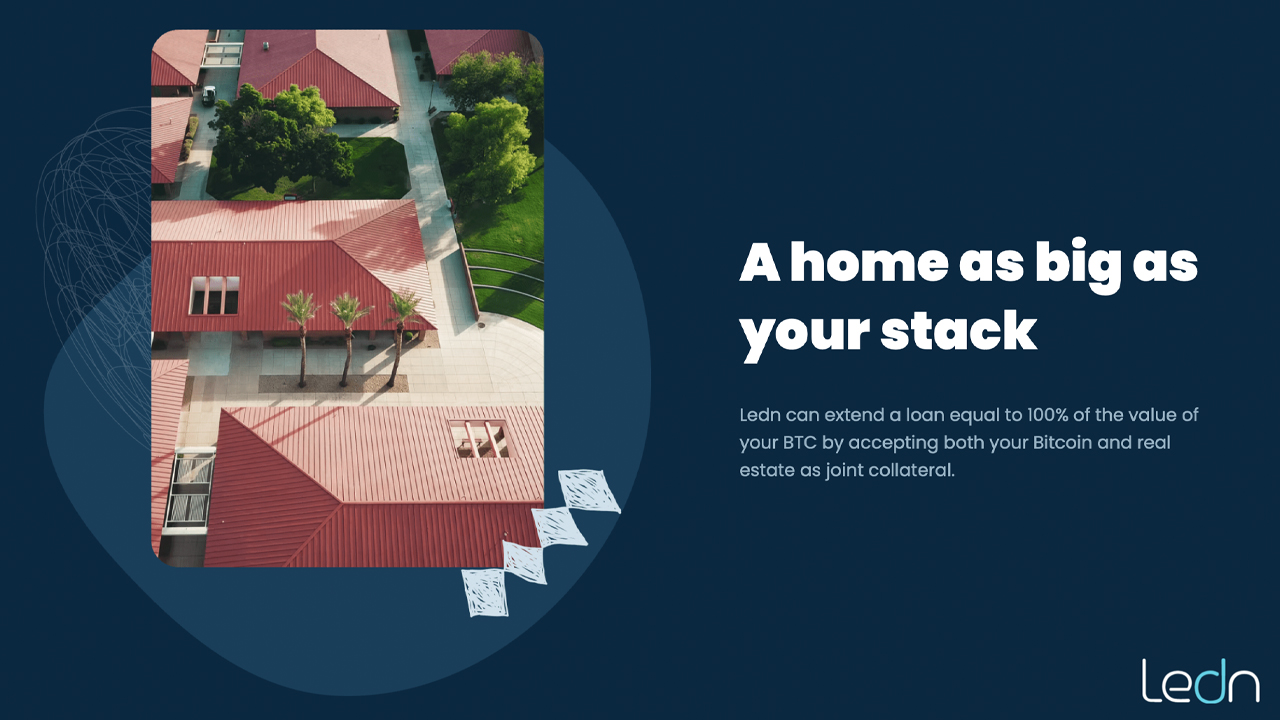

The crypto lender and savings platform Ledn revealed in December 2021 that it was readying “the impending launch of a bitcoin-backed mortgage product.” At the same time, the firm said that it raised $70 million from a handful of well-known investors.

Ledn was founded in 2018 and the company has raised a total of $103.9 million to date. At the time of writing, Ledn’s bitcoin-backed mortgage is not yet available, but people can sign up for Ledn’s mortgage product waitlist.

“By combining the appreciation potential of bitcoin with the price stability of real estate, this first-of-its-kind loan offers a balanced blend of wealth-building collateral,” Ledn’s mortgage web page says. “With the Bitcoin Mortgage, you can use your holdings to buy a new property, or finance the home you already own. Get a loan equal to your bitcoin holdings, without selling a satoshi.”

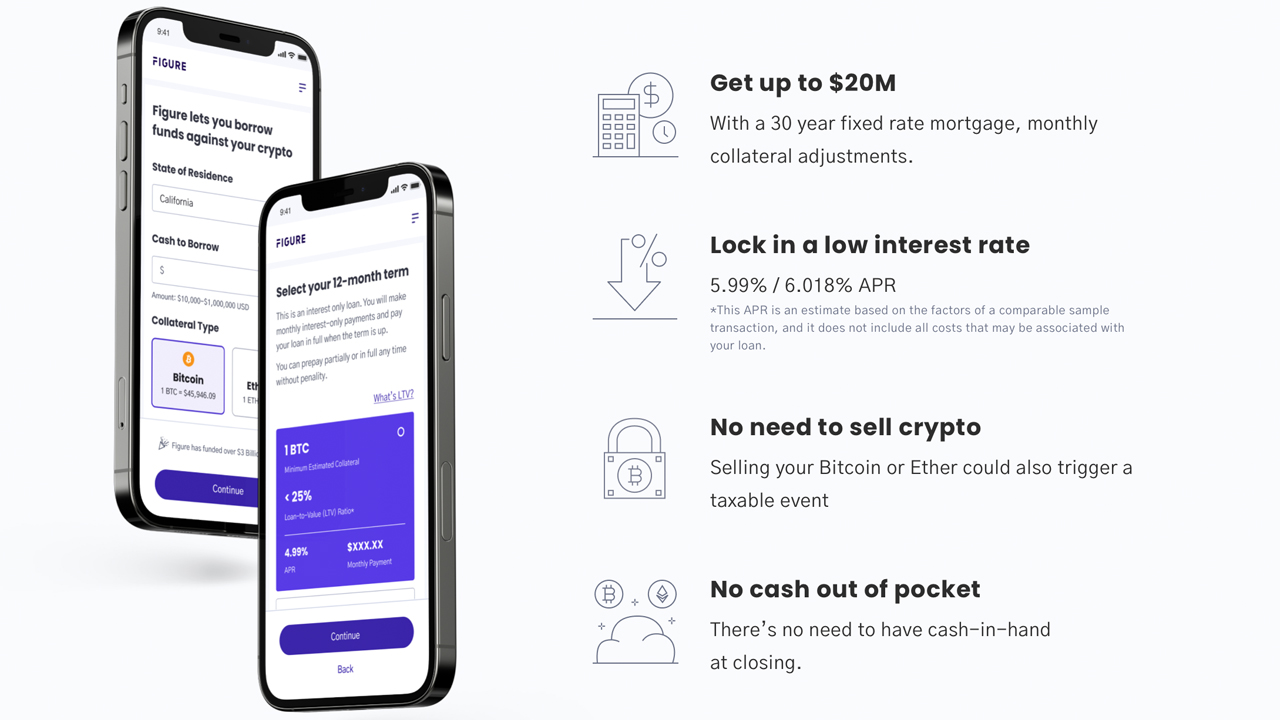

Figure Technologies also plans to provide a crypto-backed mortgage and people can sign up for a waitlist in order to access Figure’s upcoming product. Figure’s co-founder Mike Cagney explained at the end of March that the company was launching the mortgage program.

“Figure is launching a crypto-backed mortgage in early April,” Cagney said at the time. “100% LTV – you put up $5M in BTC or ETH, we give you a $5M mortgage. No painful process, no cash-out, any amount up to $20M, for a 30-year mortgage. You can make payments with your crypto collateral. And we don’t rehypothecate your crypto.”

While there’s not that many crypto-backed mortgage products today, the trend is starting to become a bit more prominent in 2022. If the trend continues, like crypto’s integration with ATMs, debit cards, and the myriad of traditional financial vehicles, the concept of buying a home with bitcoin will likely become a mainstay in society.

What do you think about the concept of crypto-backed mortgage products? Let us know what you think about this subject in the comments section below.

Image Credits: Shutterstock, Pixabay, Wiki Commons

Disclaimer: This article is for informational purposes only. It is not a direct offer or solicitation of an offer to buy or sell, or a recommendation or endorsement of any products, services, or companies. Bitcoin.com does not provide investment, tax, legal, or accounting advice. Neither the company nor the author is responsible, directly or indirectly, for any damage or loss caused or alleged to be caused by or in connection with the use of or reliance on any content, goods or services mentioned in this article.