With key stakeholders taking profits and confidence in buying the dip staying high, traders who were overzealous about a quick Bitcoin rebound back to all-time high levels were punished with further price declines.

Although Bitcoin (BTC) has subtly bounced since dropping below $34,000 in late January, its price is still down 20% in the last 30 days. Ether (ETH) has fared worse, dropping 30% in this same timeframe. This edition of the Market Insight’s newsletter takes a deeper look at the data behind the cryptocurrency market’s performance in the past month.

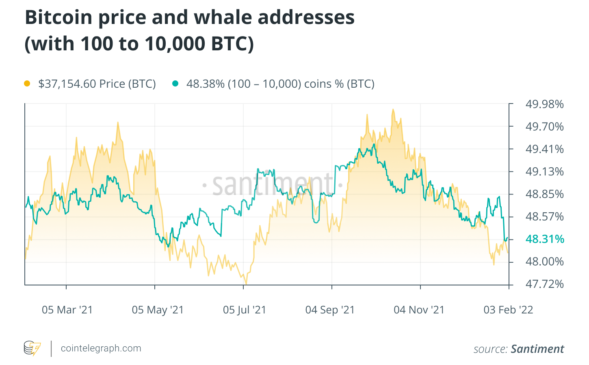

For example, Bitcoin’s key whale trader tier, typically comprising addresses holding between 100 and 10,000 BTC, has dumped approximately 150,000 BTC in the past three months.

The supply held by this group is very often used as a primary leading indicator for where prices will head next. The current supply held by these whale addresses has dropped to 47.31%, within sight of the one-year low of 47.20% held back in mid-May when prices were declining swiftly.

NVT was bearish for BTC but turned bullish in January

Santiment’s Network Value to Transactions Ratio (NVT) model measures the amount of unique BTC circulating on the network, then calculates whether that output is above, on par, or below the expected amount of circulation to justify Bitcoin’s current market capitalization.

There has been a healthy and expected amount of tokens moved since October 2021. When prices were falling during the first half of January, the month lacked the necessary circulation to keep prices above $40,000. However, on average, the month of January presented a semi-bullish signal after some dip buying and increased activity.

As a bonus, February has started off in bullish circulation territory. It can be concluded that once some other metrics align with the positive circulation divergence, prices can surge in a hurry.

FOMC impact and Bitcoin’s leading indication on S&P

Traders across several different sectors held their breaths for the United States Federal Open Market Committee’s announcement on Jan. 26. and whether or not U.S. interest rates would rise and quantitative easing would be applied. It appears that it will be a foregone conclusion that these rates will be rising about a month from now. With this news, cryptocurrency and equities markets have gradually become a bit less correlated.

Even prior to the FOMC meeting, Bitcoin had already begun its decline. And directly following the meeting, BTC’s price was the first to begin to slide. The S&P 500 has been particularly volatile and polarizing for investors and still appears to be on a notable downswing since the U.S. Federal Reserve’s meeting. Meanwhile, gold has rebounded, and Bitcoin’s price has been choppy. However, according to historical studies by Santiment, BTC price breakouts tend to happen when its price is least correlated with equities markets.

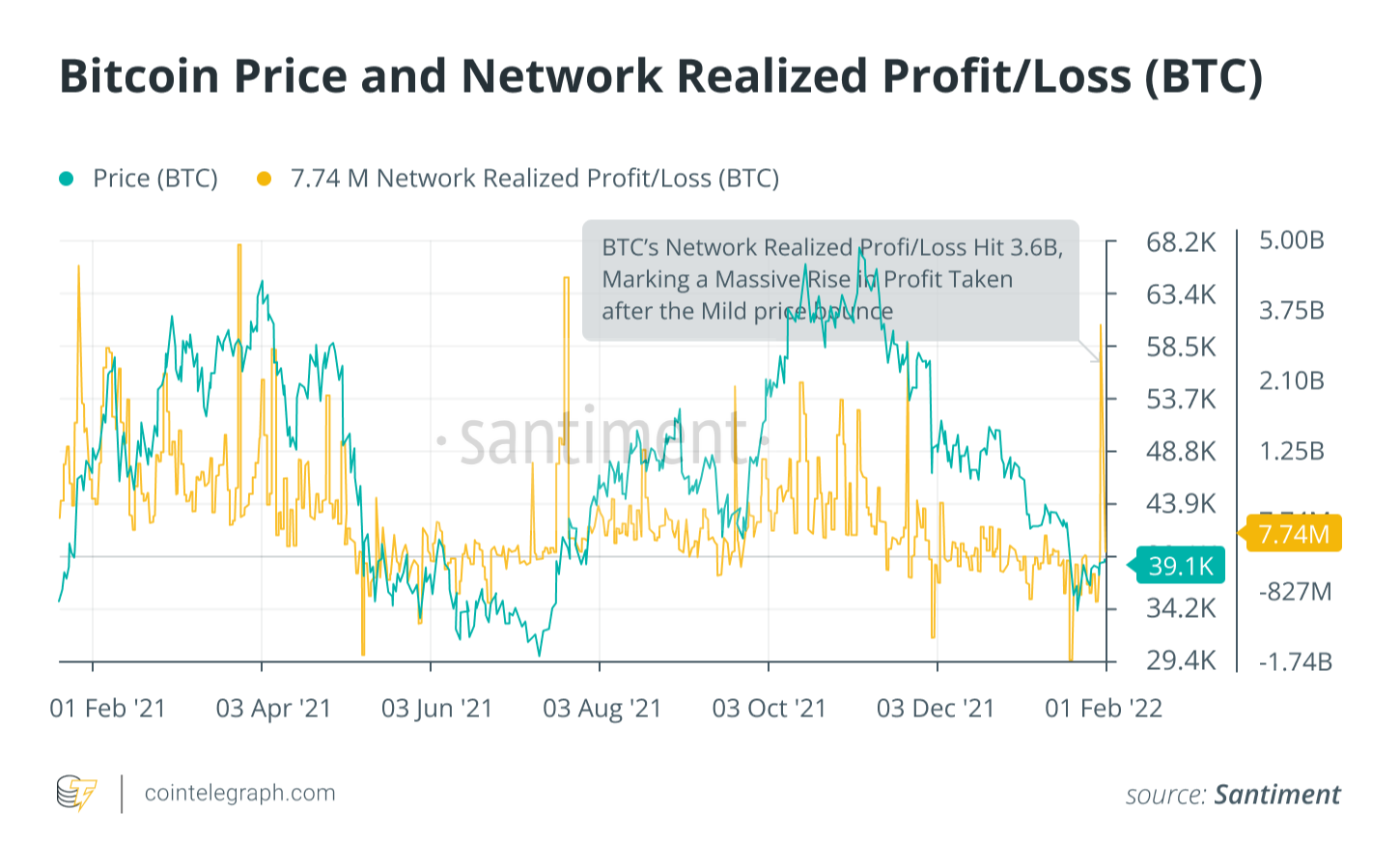

BTC network realized profit/loss spike

One of Bitcoin’s quieter days, Feb. 1 saw the fourth-highest network realized profit spike in the past year. The cumulative spike of 3.65 billion indicated a higher likelihood of a potential correction, but only if traders show disinterest.

The culprit of this massive uptick in realized profit apparently was revealed to be related to Bitcoin that was stolen in the 2016 Bitfinex exchange hack. These coins were moved on the morning of the same day, and the receiving address of these coins contains 94,643 BTC.

Negative funding rates across exchanges

From the third week of January, traders began placing large quantities of short positions, as Bitcoin’s price dropped below $34,000 for the first time since July. Various projects saw an average negative perpetual contract funding rate across multiple exchanges. With funding rates, Santiment calculates the average rates across Binance, Bitfinex, FTX, Deribit and dYdX. In some assets’ cases, a smaller combination of these exchanges is used if they aren’t listed on all five exchanges.

Generally, when there is a massive contingency of assets being shorted, liquidations occur with key stakeholders pumping prices to use the negative funding rates as rocket fuel to propel assets higher. This is exactly what ended up occurring because, on Jan. 24, the markets’ local bottom (for now) and prices quickly climbed until many of these shorts dissipated and traders began going long again.

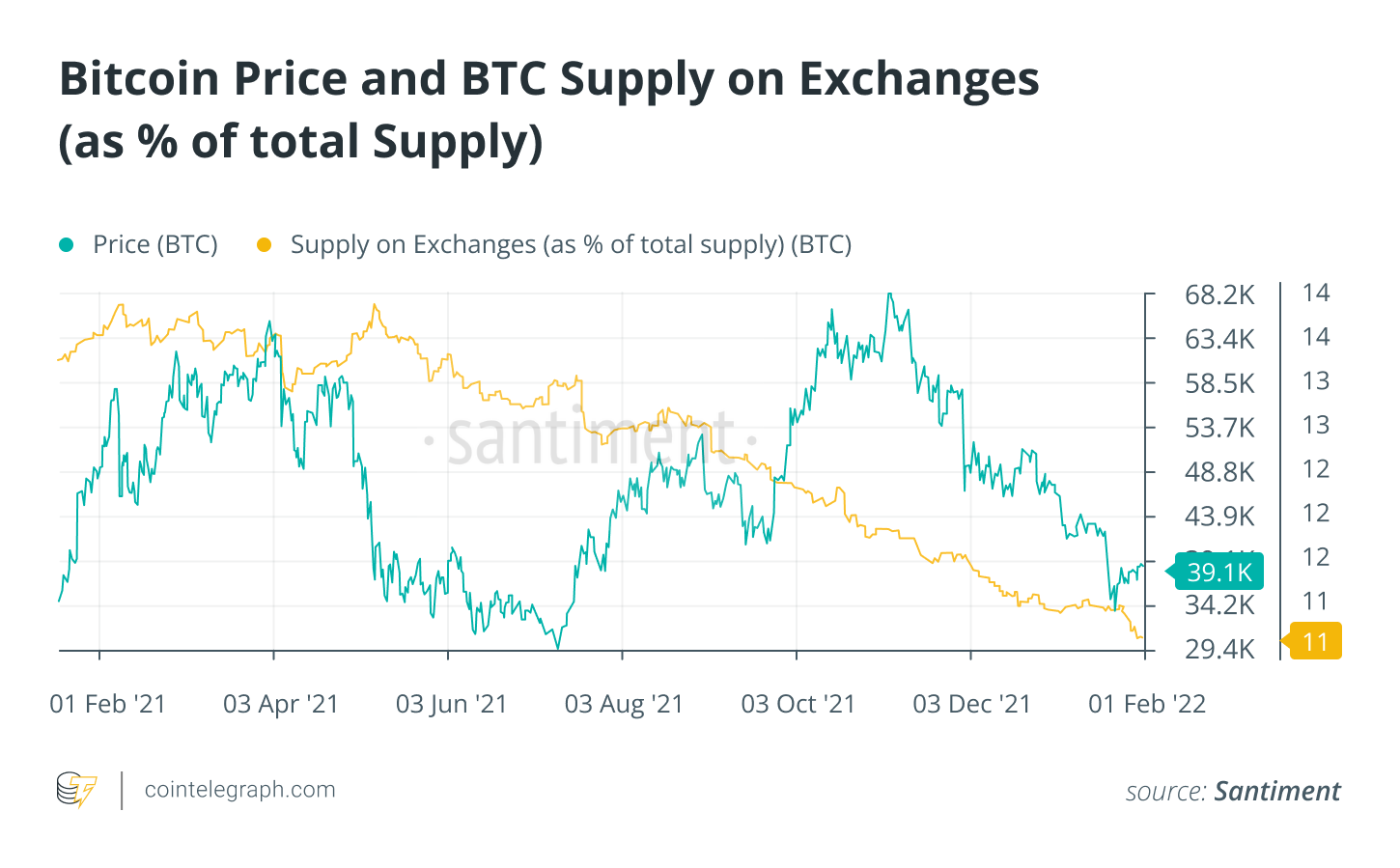

Bitcoin continues moving off exchanges

Bitcoin’s cumulative supply is down to just 11.5% sitting on exchanges at this time. Six months ago, this supply ratio on exchanges was at 13.2%. One year ago, this supply ratio was at 13.9%.

This clear downtrend in coins moving away from exchanges is generally an encouraging sign for the long-term prospects of Bitcoin’s price and market capitalization continuing to grow. With less supply of an asset available on exchanges, this limits further sell-side pressure and thus major price drop risk is mitigated.

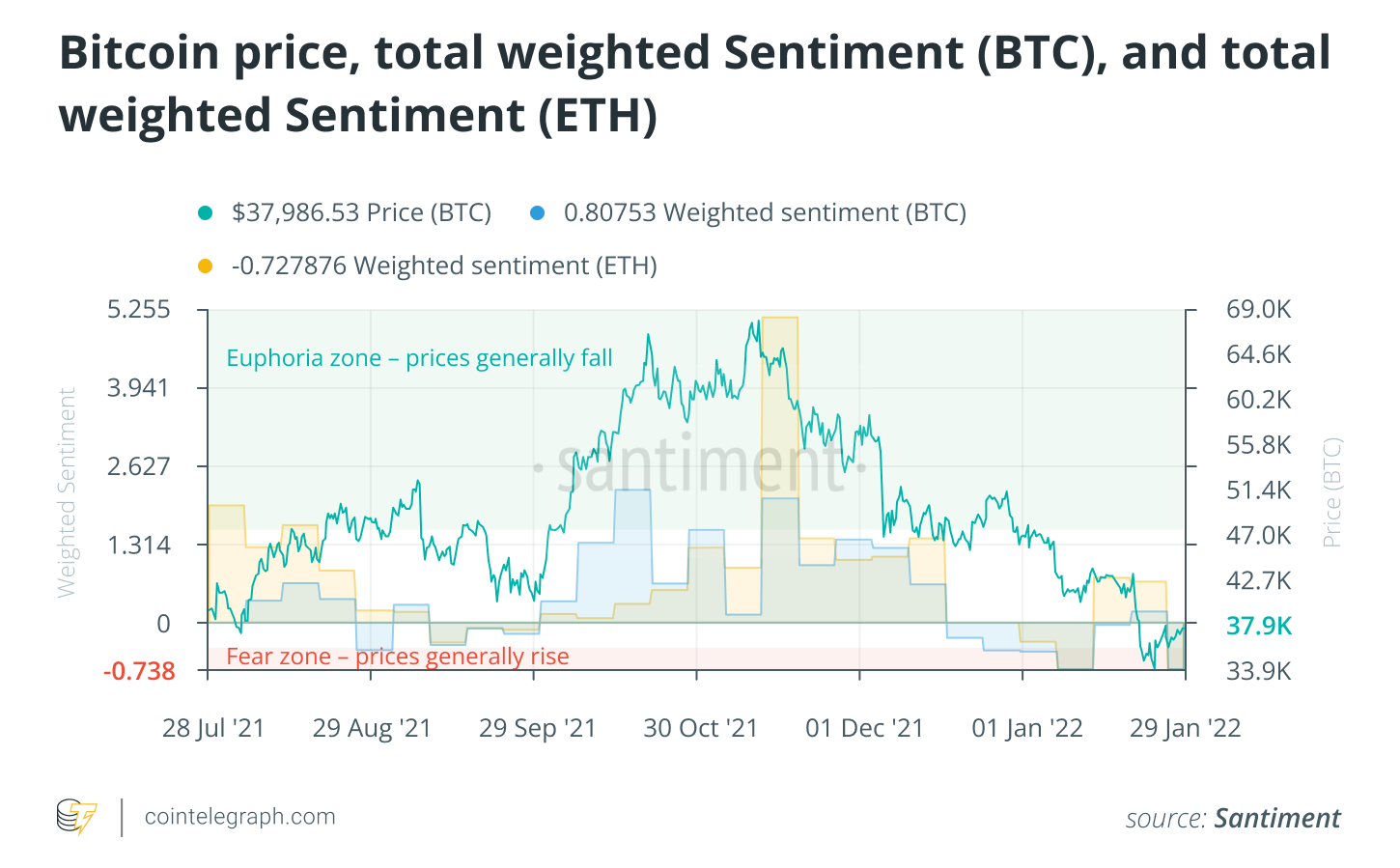

Traders show fear, marking the January local bottom

Trader sentiment toward both Bitcoin and Ether has fallen back into negative territory from mid-December to mid-January after a long stretch of euphoria from early October through mid-December. Generally, large key stakeholders wait for this crowd mindset that prices will continue to surge forever, and this is where they take profits while assets appear to be at their peak values.

Negative trader sentiment is generally a sign that price bottoms are getting close, particularly when sentiment drops into the red “fear zone,” as illustrated above.

As trader sentiment turned positive again in the second half of January, there was another price leg down that sent Bitcoin and Ether traders again into the “fear zone.” With this crowd doubting the ability of prices to rise, the probability of positive return days rises for the smaller contingency of traders who stayed patient through the volatility.

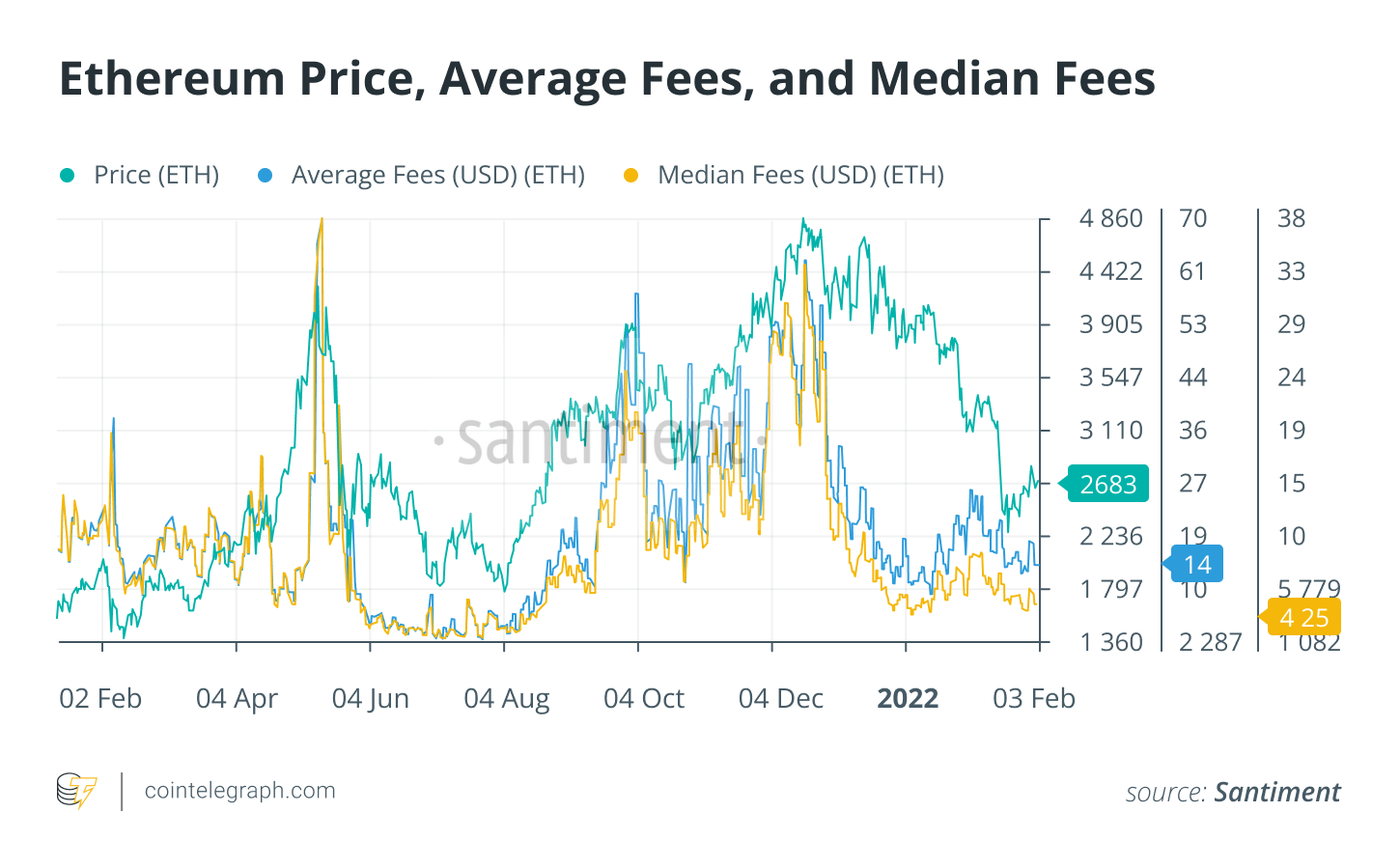

Daily average and median ETH fees

The average fee per single transaction on the Ethereum network has come back to earth in January and early February, following sky-high costs of $62.85 back at all-time high levels on Nov. 8.

Generally, Ether price corrections occur shortly after fee rates exceed $52 per average transaction or $27 per median transaction. With average fees back down to a relatively healthy $14.39 average transaction and $4.25 median transaction, it’s a promising indication that healthy utility can exist once again.

Cointelegraph’s Market Insights Newsletter shares our knowledge on the fundamentals that move the digital asset market. With market intelligence from one of the industry’s leading analytics providers, Santiment, the newsletter dives into the latest data on social media sentiment, on-chain metrics, and derivatives.

We also review the industry’s most important news, including mergers and acquisitions, changes in the regulatory landscape, and enterprise blockchain integrations. Sign up now to be the first to receive these insights. All past editions of Market Insights are also available on Cointelegraph.com.

Every investment and trading move involves risk, you should conduct your own research when making a decision.