The total cryptocurrency market capitalization dropped by 5% between Nov. 14 and Nov. 21, reaching a notable $795 billion. However, the overall sentiment is far worse, considering that this valuation is the lowest seen since December 2020.

The price of Bitcoin (BTC) dipped a mere 2.8% on the week, but investors have little to celebrate because the current $16,100 level represents a 66% drop year-to-date. Even if the FTX and Alameda Research collapse has been priced in, investor uncertainty is now focused on the Grayscale funds, including the $10.5 billion Grayscale Bitcoin Trust.

Genesis Trading, part of the Digital Currency Group (DCG) conglomerate, halted withdrawals on Nov. 16. In its latest quarterly report, the crypto derivatives and lending trading firm stated that it has $2.8 billion worth of active loans. The fund administrator, Grayscale, is a subsidiary of DCG, and Genesis acted as a liquidity provider.

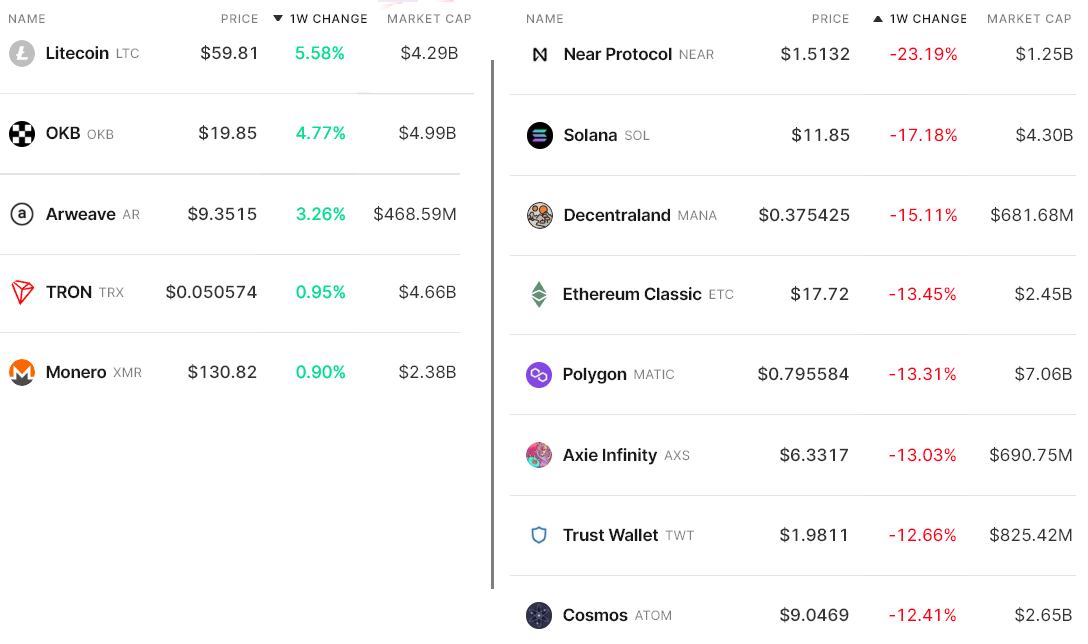

The 5% weekly drop in total market capitalization was mostly impacted by Ether’s (ETH) 8.5% negative price move. Still, the bearish sentiment had a larger effect on altcoins, with nine of the top 80 coins losing 12% or more in the period.

Litecoin (LTC) gained 5.6% after dormant addresses in the network for one year surpassed 60 million coins.

Near Protocol’s NEAR (NEAR) dropped 23% due to concerns about the 17 million tokens held by FTX and Alameda, which backed Near Foundation in March 2022.

Decentraland’s MANA (MANA) lost 15% and Ethereum Classic (ETC) another 13.5% as both projects had considerable investments from Digital Currency Group, controller of the troubled Genesis Trading.

Balanced leverage demand between bulls and bears

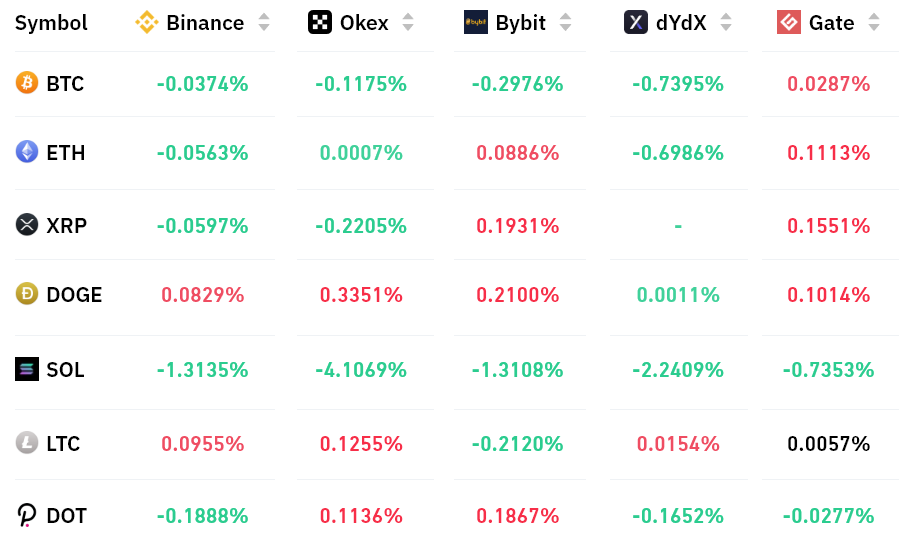

Perpetual contracts, also known as inverse swaps, have an embedded rate usually charged every eight hours. Exchanges use this fee to avoid exchange risk imbalances.

A positive funding rate indicates that longs (buyers) demand more leverage. However, the opposite situation occurs when shorts (sellers) require additional leverage, causing the funding rate to turn negative.

The seven-day funding rate was slightly negative for Bitcoin, so the data points to excessive demand for shorts (sellers). Still, a 0.20% weekly cost to maintain bearish positions is not worrisome. Moreover, the remaining altcoins — apart from Solana’s SOL (SOL) — presented mixed numbers, indicating a balanced demand between longs (buyers) and shorts.

Traders should also analyze the options markets to understand whether whales and arbitrage desks have placed higher bets on bullish or bearish strategies.

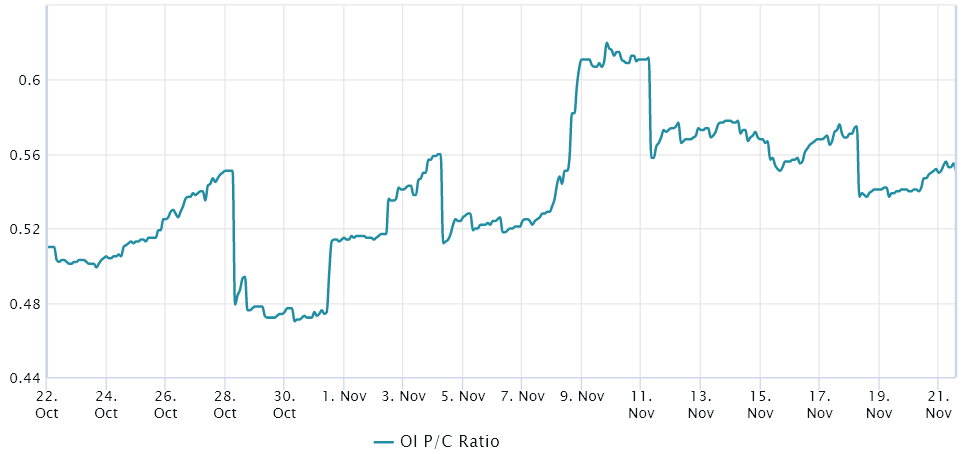

The options put/call ratio shows moderate bullishness

Traders can gauge the market’s overall sentiment by measuring whether more activity is going through call (buy) options or put (sell) options. Generally speaking, call options are used for bullish strategies, whereas put options are for bearish ones.

A 0.70 put-to-call ratio indicates that put options’ open interest lags the more bullish calls by 30% and is therefore bullish. In contrast, a 1.20 indicator favors put options by 20%, which can be deemed bearish.

Even though Bitcoin’s price broke below $16,000 on Nov. 20, investors did not rush for downside protection using options. As a result, the put-to-call ratio remained steady near 0.54. Furthermore, the Bitcoin options market remains more strongly populated by neutral-to-bearish strategies, as the current level favoring buy options (calls) indicates.

Derivatives data shows investors’ resilience considering the absence of excessive demand for bearish bets according to the futures funding rate and the neutral-to-bullish options open interest. Consequently, the odds are favorable for those betting that the $800 billion market capitalization support will display strength.

The views, thoughts and opinions expressed here are the authors’ alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.