Reason to trust

Strict editorial policy that focuses on accuracy, relevance, and impartiality

Created by industry experts and meticulously reviewed

The highest standards in reporting and publishing

Strict editorial policy that focuses on accuracy, relevance, and impartiality

Morbi pretium leo et nisl aliquam mollis. Quisque arcu lorem, ultricies quis pellentesque nec, ullamcorper eu odio.

In a new essay published on March 31, former BitMEX CEO Arthur Hayes lays out a case for a $250,000 Bitcoin price target by year-end, grounded in his belief that the US Federal Reserve has effectively capitulated to fiscal dominance and resumed de facto quantitative easing (QE) for US Treasury markets.

The essay, laced with vivid satire and underpinned by rigorous macroeconomic analysis, argues that the Fed’s recent shift in policy signals a structural return to fiat liquidity expansion—an environment historically beneficial to Bitcoin and other hard assets. “Powell proved last week that fiscal dominance is alive and well,” Hayes wrote. “Therefore, I am confident QT, at least regarding treasuries, will stop in the short to medium term… Bitcoin will scream higher once this is formally announced.”

QE Returns, Fiat Dies, Bitcoin Flies

Hayes centers his argument on the Federal Reserve’s March FOMC meeting, during which Chair Jerome Powell suggested that balance sheet reduction—or Quantitative Tightening (QT)—would slow considerably. Powell stated: “We strongly want the MBS [mortgage-backed securities] to roll off our balance sheet at some point. We would look closely at letting the MBS roll off but keep the overall balance sheet size constant.”

Related Reading

This policy configuration, dubbed “QT Twist” by Hayes, implies that the Fed will reinvest MBS runoff proceeds into US Treasuries, thereby supporting bond prices while holding the nominal balance sheet steady. Hayes characterizes this as “treasury QE,” even if not labeled as such.

“If the Fed balance sheet is kept constant, then they can buy: Max $35 billion per month of treasuries or annualized $420 billion,” Hayes calculated. In addition, the tapering of Treasury QT from $25 billion to $5 billion per month represents an annualized $240 billion positive shift in dollar liquidity.

To frame the Fed’s political constraints, Hayes invoked a satirical dialogue in which Powell is subjected to humiliation by Treasury Secretary Scott Bessent—a fictionalized dramatization that underscores the subordination of monetary policy to fiscal necessity. In this theatrical allegory, Powell is told by Bessent: “Next week at the FOMC, you are going to start tapering QT for my treasury bonds and announce that QE for treasury bonds will start in the near future. Do you understand?”

Hayes reinforces his point by drawing historical parallels to Arthur Burns, Fed Chair during the inflationary 1970s, who admitted in his 1979 speech “The Anguish of Central Banking” that political pressure rendered the Fed powerless to stop inflation.

Burns wrote: “The Federal Reserve was itself caught up in the philosophic and political currents that were transforming American life and culture… Monetary policy came to be governed by the principle of under-nourishing the inflationary process while still accommodating a good part of the pressures in the marketplace.”

Related Reading

Hayes sees the same dynamic today, intensified by the government’s ballooning debt burden and the need to finance deficits at low yields.

Trump’s Policy Agenda

Hayes ties the Fed’s pivot to the political realities of a second Trump administration, particularly its industrial policy goals. Trump has pledged to reduce the US fiscal deficit from 7% to 3% of GDP by 2028, while reshoring manufacturing, sustaining military spending, and avoiding cuts to entitlements.

However, Hayes argues that these objectives are mathematically incompatible without central bank support, given the scale of debt issuance required. “The maths don’t add up unless Bessent can find a buyer of treasuries at an uneconomically high price or low yield. Only US commercial banks and the Fed have the firepower to buy the debt at a level the government can afford.”

To unlock that capacity, Hayes anticipates the Fed will not only halt QT but also exempt banks from the Supplementary Leverage Ratio (SLR)—a key regulatory constraint limiting bank purchases of U.S. Treasuries.

Bessent himself hinted at such a move on the All-In Podcast, stating: “If we take [SLR] away… we might actually pull treasury bill yields down by 30 to 70 basis points. Every basis point is a billion dollars a year.”

Hayes maintains that Bitcoin is uniquely positioned to benefit from this shift in monetary regime. Unlike equities, which are entangled in the legal and political architecture of the state, Bitcoin is a bearer instrument native to the digital realm, with no counterparty risk.

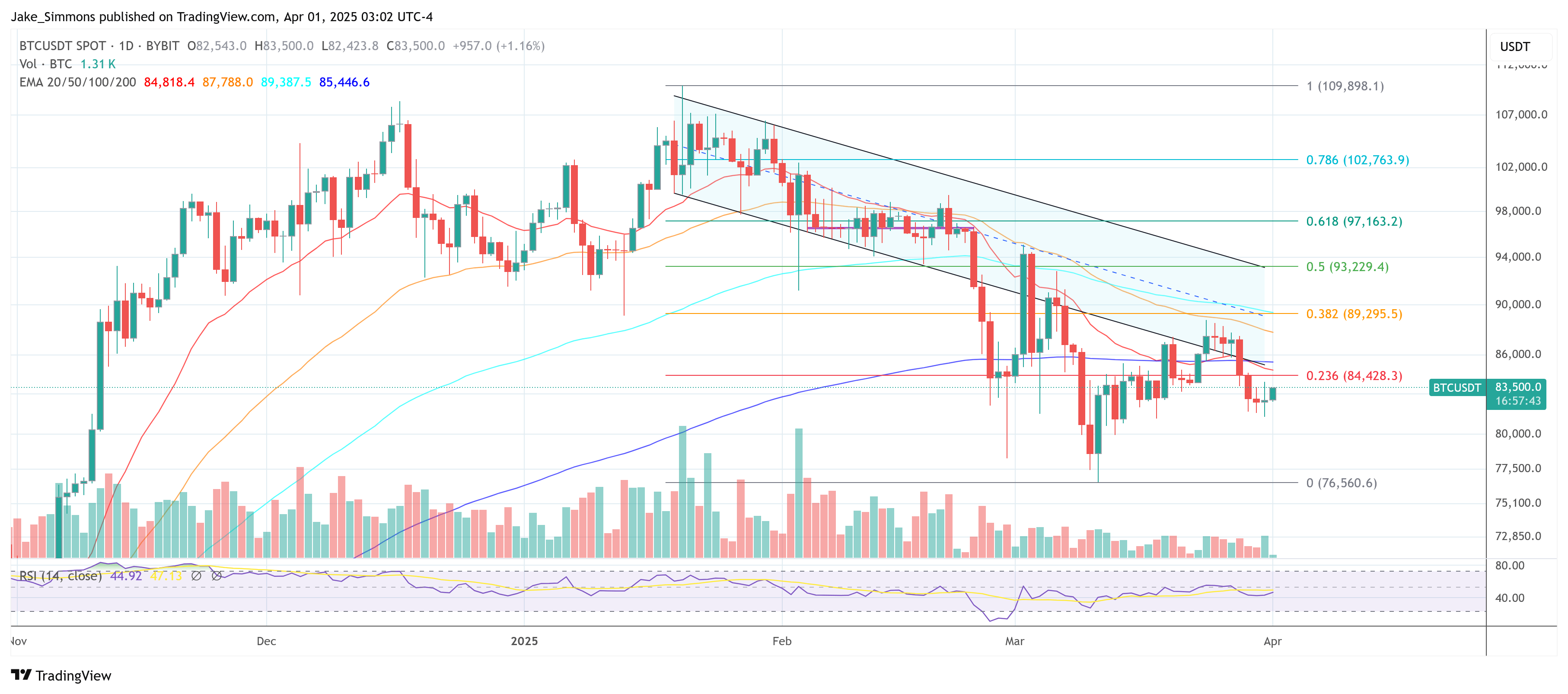

“Bitcoin trades solely based on the market expectation for the future supply of fiat,” he wrote. “If my analysis… is correct, then Bitcoin hit a local low of $76,500 last month, and now we begin the ascent to $250,000 by year-end.”

Referencing gold’s reaction to QE1 in 2008–2009, Hayes highlights how liquidity injections can lead to delayed but explosive repricing of anti-fiat assets. In his view, Bitcoin is now playing the same role gold once did—only faster and with more direct global exposure.

Hayes also offered insight into Maelstrom’s capital deployment approach. “We use no leverage, and we buy in small clips relative to the size of our total portfolio,” he said. “We have been buying Bitcoin and shitcoins at all levels between $90,000 to $76,500.”

At press time, BTC traded at $83,500.

Featured image from YouTube, chart from TradingView.com