Over the past few years, cryptocurrency has come into the public eye more than ever, as large investment firms begin to heavily invest in blue-chip cryptocurrencies like Bitcoin and Ethereum. Due to this spike in adoption from companies and the general public, governments all around the world have frantically tried to put in place proper regulations for crypto. The FCA and HMRC, which are the main bodies currently dealing with cryptocurrency regulation in the UK have been progressive in their view of crypto, the regulation it has received, and competent tax advice for the public.

Having said that, there still have been many road bumps in this process, creating a lot of confusion. We cannot expect a government to want to adopt a currency decentralized in nature with open arms so in many eyes, the UK has done as good a job as any, especially compared to other democratic countries, like Canada for example.

Let’s take a look at the problems the UK has faced with cryptocurrency, its adoption or lack thereof, and how global regulation is affecting the UK government’s decisions.

How Does the UK and HMRC Class Cryptocurrency?

HMRC recognizes cryptocurrencies as digital assets or ‘cryptoassets’, subject to capital gains or income tax depending on the event. Cryptocurrencies are not recognized as actual currencies, like the UK’s pound, instead, HMRC classes them as digital assets with four distinct categories.

- Stablecoins

- Utility Tokens

- Security Tokens

- Exchange Tokens

Current Regulation

At the start of 2020, the FCA was granted powers to view and supervise UK businesses involved in cryptocurrency about managing risk around money laundering and the prevention of terrorist financing. Businesses dealing with crypto are now required to meet all requirements set by the Money Laundering Regulations and register with the FCA (Financial Conduct Authority).

For individuals, the FCA claims to only regulate cryptoassets for money laundering reasons but specifically states that if losses are made by hacks or loss of a private key, it is unlikely services such as the Financial Services Compensation sets, with cryptoassets such as security tokens falling under the jurisdiction, as they provide rights, ownership, debts, or liabilities, the FSCS has the ability to step in.

Exchange coins, such as Bitcoin, are out of their scope, similarly to Utility coins such as Ethereum which are used to interact with a blockchain.

*The FCA has banned all exchanges from offering derivatives trading and set the requirements for Know Your Customer (KYC ) protocols on centralized exchanges.

Tax Laws

For an in-depth guide on UK crypto tax laws, take a look at our Ultimate UK cryptocurrency tax guide.

Without going into too much detail, HMRC recognizes two types of income coming from investments without the crypto space.

1. Capital Gains Tax

The most common type of income a crypto investor can have is a capital gain, which comes from the disposal of a capital asset, in most cases, this is a cryptocurrency. HMRC recognizes a gain on sold cryptocurrency to be:

Total revenue from sale – Cost basis (fair market value at the time of purchase) + fees

Capital gains tax, in correspondence to your tax bracket, is then due to be paid on the gain. Each UK investor is granted an annual capital gains allowance of £12,300 which can be used on cryptoassets.

Other types of potential capital gains which HMRC recognizes come from:

- Trading NFTs (Same of cryptocurrencies apply here)

- Selling Airdropped tokens

- Crypto-Liquidity Pool token trades

2. Income Tax

Income tax is a relatively new adoption to HMRC’s tax laws surrounding cryptoassets, and is a fairly new concept in the crypto world, all things considered. The most common type of cryptocurrency income comes from Staking, which is the protocol involved with PoS (Proof of Stake), where validators secure each transaction on the blockchain by providing liquidity. This is the alternative to PoW (Proof of Work), the validation method of Bitcoin.

HMRC assumes that income tax is payable when a service, even as small as sharing a Facebook page, is performed for cryptoassets. So, income from staking requires taxation at the relative tax bracket.

Other types of crypto income that HMRC recognize include:

- Yield farming

- Airdropped tokens

- Cryptocurrency mining

- Forks, Nodes & Lending

As mentioned before, HMRC is quite progressive when it comes to crypto taxation and has guidance on most income streams from cryptocurrency, with particular attention to different DeFi protocols. We are likely to see even more concise guidelines surrounding cryptoassets, especially with the expansion of DeFi.

The FCA’s Rocky Relationship with Cryptocurrency: Their Advice

It is important to remember that the FCA’s role is to prevent misconduct by financial service companies, and to protect its country and its people. Since crypto’s inception, it has been rife with scams and manipulation without any regulation.

It is impossible to completely avoid friction when ensuring all parties are operating fairly and legally. As the FCA has tackled the decentralized nature of cryptocurrencies, they have stumbled into a fair few battles with some of the biggest players in the game.

Examples:

In June 2021, Binance was ordered by the FCA to ‘cease all regulated activities’.

After a review, Binance announced that any UK investor using Binance’s trading platform will not have protection from the services it provides if the investment is lost or stolen.

Banning Misleading Crypto Adverts

A horde of adverts have been questioned and ultimately banned by the FCA as they are said to be misleading, not showing the full risks of investing in the crypto sphere. Regulations are currently being made to ensure advertisers fully understand what type of adverts are allowed when talking about cryptocurrency. Few investors understand it is an unregulated asset.

The Future Of Cryptocurrency in The UK

Current Adoption

The UK has made great strides in recognizing cryptocurrency as legitimate assets or electronic cash and allowing public adoption inside the UK.

For example, the UK has the most Bitcoin ATMs out of any other UK country.

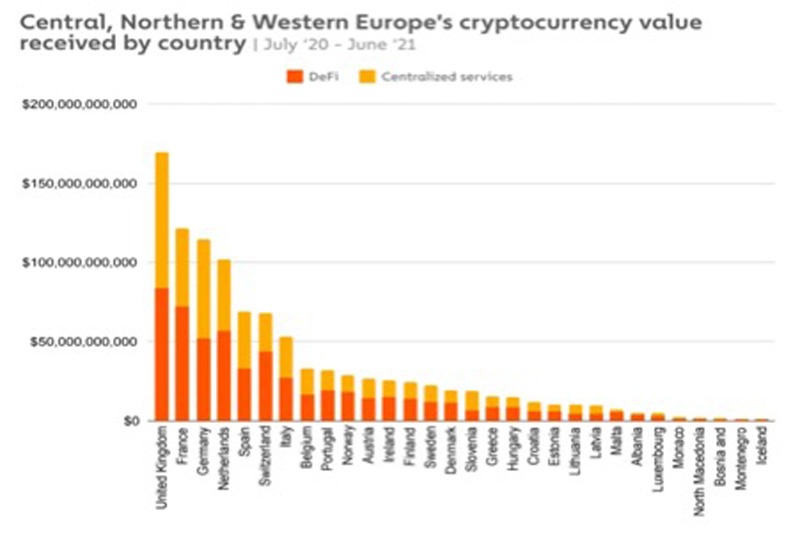

Also, the UK has become Europe’s largest transactor in the crypto market, with a total of £126bn in transactions in 2021, which was driven mainly by institutional investment.

Source: (Yahoo Finance)

To really show how crypto adoption has soared in the UK, we can look at statistics from cybercrew. Statistics such as a growth of 1.5 Million crypto owners in 2018 to 9.8 million in 2021 really show the growth in the UK market, with 30% of those owners being aged 18-29, which is expected in this risky environment.

The Future

There is no confirmed legislature proposed by the UK in the short term. As the UK continues to follow along with its EU neighbours, it’s likely we will see the UK government stop following advice from the EU, especially after Brexit.

The FCA’s Chief Executive, Nikhil Rathi, has stated on record that they are looking to put greater regulations on the DeFi world.

It is likely this upward trend of adoption continues to happen within the UK as more and more people start to become aware of the benefits of cryptocurrency and their care for privacy and security. We should not understate how the last two years of the pandemic have widened many eyes about the power a government has over its potential and their ability to impose potentially unfair rulings. It is likely to see greater adoption in the DeFi world, as investors attempt to become financially independent not just from others, but from their government.

However, adoption will almost always come with regulation, which may remove many elements of privacy from the crypto sphere, that some believe have already happened. Domestic and global regulation will have different effects on the entire crypto space. Let’s discuss how increased global regulation of cryptoassets will affect the UK.

Increased Global Regulation, What Does It Mean for the UK?

As we have seen, the UK has some of the largest crypto adoptions worldwide and the government is simply looking to regulate the crypto space, not ban its people from it. So, how will global regulation affect the relationship the UK has with crypto?

Some analysts believe that harsh global regulation will negatively affect the crypto markets and cause investors to leave. However, for some, the decentralized philosophy is deeply embedded into the investing practices that they may simply take their business off-shore. With over 30% of young Brits in the crypto space, this would be a massive loss for the UK.

- Greater regulation worldwide may also cause the UK to provide greater clarity for investors, grow the population’s trust in the crypto markets, and cause even faster adoption than we have already seen over the last three years.

There is no certain outcome that will come from greater regulation due to the lack of evidence. Although, most crypto investors simply want crypto to co-exist with fiat currency with the potential for cryptocurrencies such as Bitcoin to be allowed to pay for certain transactions online or in the real world.

Conclusion – I

Yes, crypto is legal in the UK. However, all over the world governments and agencies are scrambling to proficiently regulate cryptoassets to give investors clarity but also make gains and income from the crypto markets taxable and legal. Although some believe mass adoption is right around the corner, it may be many years before governments come to grips with the changing environment around them, relieving them of powers which they are accustomed to having.

Over the past few years, cryptocurrency has come into the public eye more than ever, as large investment firms begin to heavily invest in blue-chip cryptocurrencies like Bitcoin and Ethereum. Due to this spike in adoption from companies and the general public, governments all around the world have frantically tried to put in place proper regulations for crypto. The FCA and HMRC, which are the main bodies currently dealing with cryptocurrency regulation in the UK have been progressive in their view of crypto, the regulation it has received, and competent tax advice for the public.

Having said that, there still have been many road bumps in this process, creating a lot of confusion. We cannot expect a government to want to adopt a currency decentralized in nature with open arms so in many eyes, the UK has done as good a job as any, especially compared to other democratic countries, like Canada for example.

Let’s take a look at the problems the UK has faced with cryptocurrency, its adoption or lack thereof, and how global regulation is affecting the UK government’s decisions.

How Does the UK and HMRC Class Cryptocurrency?

HMRC recognizes cryptocurrencies as digital assets or ‘cryptoassets’, subject to capital gains or income tax depending on the event. Cryptocurrencies are not recognized as actual currencies, like the UK’s pound, instead, HMRC classes them as digital assets with four distinct categories.

- Stablecoins

- Utility Tokens

- Security Tokens

- Exchange Tokens

Current Regulation

At the start of 2020, the FCA was granted powers to view and supervise UK businesses involved in cryptocurrency about managing risk around money laundering and the prevention of terrorist financing. Businesses dealing with crypto are now required to meet all requirements set by the Money Laundering Regulations and register with the FCA (Financial Conduct Authority).

For individuals, the FCA claims to only regulate cryptoassets for money laundering reasons but specifically states that if losses are made by hacks or loss of a private key, it is unlikely services such as the Financial Services Compensation sets, with cryptoassets such as security tokens falling under the jurisdiction, as they provide rights, ownership, debts, or liabilities, the FSCS has the ability to step in.

Exchange coins, such as Bitcoin, are out of their scope, similarly to Utility coins such as Ethereum which are used to interact with a blockchain.

*The FCA has banned all exchanges from offering derivatives trading and set the requirements for Know Your Customer (KYC ) protocols on centralized exchanges.

Tax Laws

For an in-depth guide on UK crypto tax laws, take a look at our Ultimate UK cryptocurrency tax guide.

Without going into too much detail, HMRC recognizes two types of income coming from investments without the crypto space.

1. Capital Gains Tax

The most common type of income a crypto investor can have is a capital gain, which comes from the disposal of a capital asset, in most cases, this is a cryptocurrency. HMRC recognizes a gain on sold cryptocurrency to be:

Total revenue from sale – Cost basis (fair market value at the time of purchase) + fees

Capital gains tax, in correspondence to your tax bracket, is then due to be paid on the gain. Each UK investor is granted an annual capital gains allowance of £12,300 which can be used on cryptoassets.

Other types of potential capital gains which HMRC recognizes come from:

- Trading NFTs (Same of cryptocurrencies apply here)

- Selling Airdropped tokens

- Crypto-Liquidity Pool token trades

2. Income Tax

Income tax is a relatively new adoption to HMRC’s tax laws surrounding cryptoassets, and is a fairly new concept in the crypto world, all things considered. The most common type of cryptocurrency income comes from Staking, which is the protocol involved with PoS (Proof of Stake), where validators secure each transaction on the blockchain by providing liquidity. This is the alternative to PoW (Proof of Work), the validation method of Bitcoin.

HMRC assumes that income tax is payable when a service, even as small as sharing a Facebook page, is performed for cryptoassets. So, income from staking requires taxation at the relative tax bracket.

Other types of crypto income that HMRC recognize include:

- Yield farming

- Airdropped tokens

- Cryptocurrency mining

- Forks, Nodes & Lending

As mentioned before, HMRC is quite progressive when it comes to crypto taxation and has guidance on most income streams from cryptocurrency, with particular attention to different DeFi protocols. We are likely to see even more concise guidelines surrounding cryptoassets, especially with the expansion of DeFi.

The FCA’s Rocky Relationship with Cryptocurrency: Their Advice

It is important to remember that the FCA’s role is to prevent misconduct by financial service companies, and to protect its country and its people. Since crypto’s inception, it has been rife with scams and manipulation without any regulation.

It is impossible to completely avoid friction when ensuring all parties are operating fairly and legally. As the FCA has tackled the decentralized nature of cryptocurrencies, they have stumbled into a fair few battles with some of the biggest players in the game.

Examples:

In June 2021, Binance was ordered by the FCA to ‘cease all regulated activities’.

After a review, Binance announced that any UK investor using Binance’s trading platform will not have protection from the services it provides if the investment is lost or stolen.

Banning Misleading Crypto Adverts

A horde of adverts have been questioned and ultimately banned by the FCA as they are said to be misleading, not showing the full risks of investing in the crypto sphere. Regulations are currently being made to ensure advertisers fully understand what type of adverts are allowed when talking about cryptocurrency. Few investors understand it is an unregulated asset.

The Future Of Cryptocurrency in The UK

Current Adoption

The UK has made great strides in recognizing cryptocurrency as legitimate assets or electronic cash and allowing public adoption inside the UK.

For example, the UK has the most Bitcoin ATMs out of any other UK country.

Also, the UK has become Europe’s largest transactor in the crypto market, with a total of £126bn in transactions in 2021, which was driven mainly by institutional investment.

Source: (Yahoo Finance)

To really show how crypto adoption has soared in the UK, we can look at statistics from cybercrew. Statistics such as a growth of 1.5 Million crypto owners in 2018 to 9.8 million in 2021 really show the growth in the UK market, with 30% of those owners being aged 18-29, which is expected in this risky environment.

The Future

There is no confirmed legislature proposed by the UK in the short term. As the UK continues to follow along with its EU neighbours, it’s likely we will see the UK government stop following advice from the EU, especially after Brexit.

The FCA’s Chief Executive, Nikhil Rathi, has stated on record that they are looking to put greater regulations on the DeFi world.

It is likely this upward trend of adoption continues to happen within the UK as more and more people start to become aware of the benefits of cryptocurrency and their care for privacy and security. We should not understate how the last two years of the pandemic have widened many eyes about the power a government has over its potential and their ability to impose potentially unfair rulings. It is likely to see greater adoption in the DeFi world, as investors attempt to become financially independent not just from others, but from their government.

However, adoption will almost always come with regulation, which may remove many elements of privacy from the crypto sphere, that some believe have already happened. Domestic and global regulation will have different effects on the entire crypto space. Let’s discuss how increased global regulation of cryptoassets will affect the UK.

Increased Global Regulation, What Does It Mean for the UK?

As we have seen, the UK has some of the largest crypto adoptions worldwide and the government is simply looking to regulate the crypto space, not ban its people from it. So, how will global regulation affect the relationship the UK has with crypto?

Some analysts believe that harsh global regulation will negatively affect the crypto markets and cause investors to leave. However, for some, the decentralized philosophy is deeply embedded into the investing practices that they may simply take their business off-shore. With over 30% of young Brits in the crypto space, this would be a massive loss for the UK.

- Greater regulation worldwide may also cause the UK to provide greater clarity for investors, grow the population’s trust in the crypto markets, and cause even faster adoption than we have already seen over the last three years.

There is no certain outcome that will come from greater regulation due to the lack of evidence. Although, most crypto investors simply want crypto to co-exist with fiat currency with the potential for cryptocurrencies such as Bitcoin to be allowed to pay for certain transactions online or in the real world.

Conclusion – I

Yes, crypto is legal in the UK. However, all over the world governments and agencies are scrambling to proficiently regulate cryptoassets to give investors clarity but also make gains and income from the crypto markets taxable and legal. Although some believe mass adoption is right around the corner, it may be many years before governments come to grips with the changing environment around them, relieving them of powers which they are accustomed to having.