The total crypto market capitalization fell off a cliff between June 10 and 13 as it broke below $1 trillion for the first time since January 2021. Bitcoin (BTC) fell by 28% within a week and Ether (ETH) faced an agonizing 34.5% correction.

Presently, the total crypto capitalization is at $890 million, a 24.5% negative performance since June 10. That certainly raises the question of how the two leading crypto assets managed to underperform the remaining coins. The answer lies in the $154 billion worth of stablecoins distorting the broader market performance.

Even though the chart shows support at the $878 billion level, it will take some time until traders take in every recent event that has impacted the market. For example, the U.S. Federal Reserve raised interest rates by 75 basis points on June 15, the largest hike in 28 years. The central bank also initiated a balance sheet cut in June, aiming to reduce its $8.9 trillion positions, including mortgage-backed securities (MBS).

Venture firm Three Arrows Capital (3AC) has reportedly failed to meet margin calls from its lenders, raising high major insolvency red flags across the industry. The firm’s heavy exposure to Grayscale Bitcoin Trust (GBTC) and Lido’s Staked ETH (stETH) was partially responsible for the mass liquidation events. A similar issue forced crypto lending and staking firm Celsius to halt users’ withdrawals on June 13.

Investors’ spirit is effectively broken

The bearish sentiment was clearly reflected in crypto markets as the Fear and Greed Index, a data-driven sentiment gauge, hit 7/100 on June 16. The reading was the lowest since August 2019 and it was last seen outside the “extreme fear” zone on May 7.

Below are the winners and losers since June 10. Curiously, Ether was the only top-10 crypto to figure on the list, which is unusual during strong corrections.

WAVES lost another 37% after the project’s largest decentralized finance (DeFi) application Vires Finance implemented a daily $1,000 stablecoin withdrawal limit.

Ether dropped 34.5% as developers postponed the switch to a proof-of-stake consensus mechanism for another two months. The “difficulty bomb” will essentially cease mining processing, paving the way for the Merge.

Aave (AAVE) traded down 33.7% after MakerDAO hvoted to cut off the lending platform Aave’s ability to generate Dai (DAI) for its lending pool without collateral. The community-led decision aims to mitigate the protocol’s exposure to a potential impact from staked Ether (stETH) collateral.

Asian traders flew into stablecoins

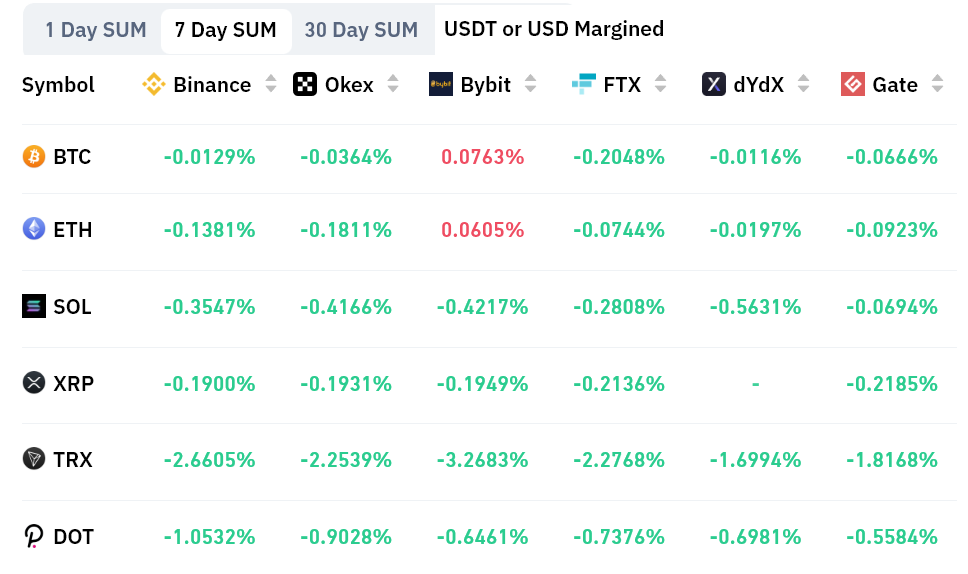

The OKX Tether (USDT) premium is a good gauge of China-based retail crypto trader demand. It measures the difference between China-based peer-to-peer (P2P) trades and the United States dollar.

Excessive buying demand tends to pressure the indicator above fair value at 100%, and during bearish markets, Tether’s market offer is flooded and causes a 4% or higher discount.

Contrary to expectations, Tether had been trading with a premium in Asian peer-to-peer markets since June 12. Despite the massive sell-off in crypto prices, investors have been seeking protection in stablecoins instead of exiting to fiat currency. This movement lasted until June 17, as the USDT paired its price versus the official foreign exchange currency rate.

One should analyze crypto derivatives metrics to exclude externalities specific to the stablecoin market. For instance, perpetual contracts have an embedded rate that is usually charged every eight hours. Exchanges use this fee to avoid exchange risk imbalances.

A positive funding rate indicates that longs (buyers) demand more leverage. However, the opposite situation occurs when shorts (sellers) require additional leverage, causing the funding rate to turn negative.

Those derivative contracts show more significant demand for leverage short (bear) positions across the board. Although Bitcoin and Ether’s numbers were insignificant, the TRX token and Polkadot (DOT) situation raise concerns.

Pokadot’s negative 0.90% weekly rate equals 3.7% per month, meaning those betting on the price decrease are willing to pay a reasonable fee to maintain their leverage positions. This is usually interpreted as a sign of confidence from bears; hence, slightly worrisome.

The market dipped by 70% and there’s still no demand from leverage longs

The big question is how backward-looking is the investors’ fear and lack of appetite for buyers using leverage despite the 70% correction since the November 2021 peak. It is encouraging to know that Asian traders moved their positions to Tether instead of exiting all markets to fiat deposits.

There likely won’t be a clear sign of a bottom formation, but Bitcoin bulls need to hold ground at $20,000 to avoid breaking a 13-year-old pattern of never breaking below the previous four-year cycle all-time high.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.