Before crypto exchange FTX and its founder Sam Bankman-Fried (SBF) got tied down with allegations of misappropriation of users’ funds, SBF was among the most influential crypto entrepreneurs. Before FTX collapsed, a leaked email exchange with a top regulator allegedly showed SBF’s intent to get the exchange federally regulated.

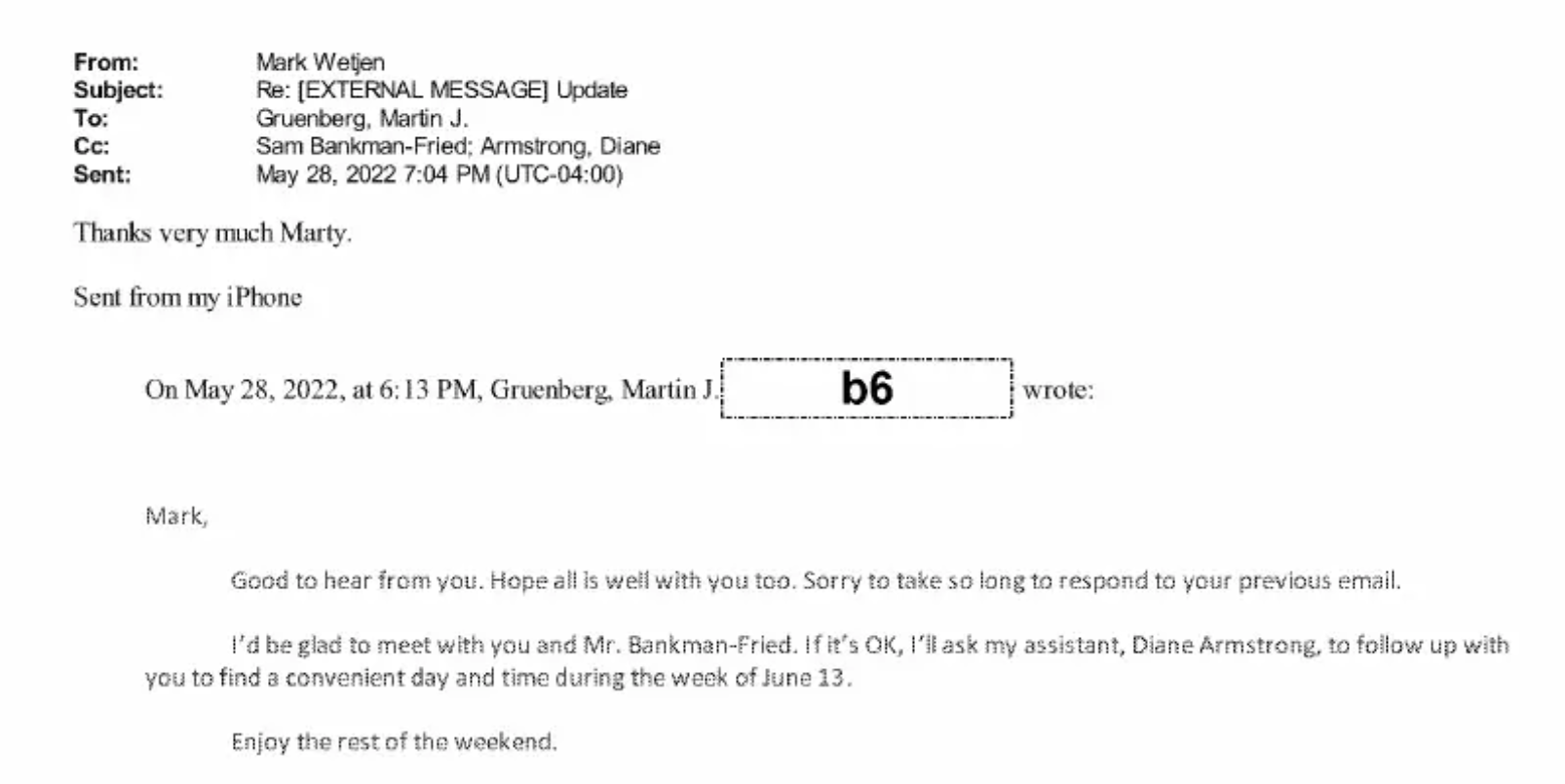

On May 28, 2022, nearly six months before FTX filed for bankruptcy and SBF resigned as the CEO, Federal Deposit Insurance Corporation (FDIC) chairman Martin Gruenberg received an invitation to meet SBF on June 13, 2022, the Washington Examiner reported. The email was mediated by former CFTC commissioner Mark Wetjen, who joined FTX US as the head of policy and regulatory strategy in November 2021.

In the latter half of the email, Wetjen told Gruenberg that FTX is in the “unusual position of begging the federal government to regulate us.” He further added:

“We have an application before the CFTC that lays out for the agency how to do so. All the CFTC has to do is approve it. Once the CFTC does, the others will follow — the other major US exchanges also have CFTC licenses.”

In response to the SBF’s request, Gruenberg agreed to meet the duo, as shown in the leaked email below.

Following the collapse of FTX, SBF’s political ties were uncovered amid parallel investigations. An FDIC spokesperson confirmed that the FDIC chairman met SBF as part of “routine courtesy visits with leaders of financial firms and institutions.”

Related: Sam Bankman-Fried to propose revised bail package ‘by next week’

Alongside federal investigations, FTX’s new management started conducting internal investigations to track missing funds.

Sharing the FTX Debtors’ press release just issued: https://t.co/r7PlneGSXF

— FTX (@FTX_Official) March 16, 2023

Recent court documents revealed that SBF and five other former FTX and Alameda Research executives received $3.2 billion in payments and loans from FTX-linked entities. SBF reportedly received the lion’s share of the funds, receiving $2.2 billion.