Bitcoin (BTC) starts a “massive” week in a precarious position as key support stays out of reach for bulls.

After fresh losses across crypto markets over the weekend, BTC/USD closed the week below $26,000 for the first time in three months.

Both Bitcoin and altcoins continue to struggle thanks to legal battles raging in the United States and their impact on market sentiment.

Fragile markets will now encounter a slew of volatility triggers, however, as U.S. macro data releases accompany the next steps in the crypto legal debacle.

In what promises to be five days full of surprises, traders will likely experience none of the lackluster sideways price action characteristic of crypto markets before the recent upheaval.

How will the coming week shape up? Cointelegraph looks at the major things to consider when it comes to Bitcoin and wider crypto market price action.

Bitcoin loses key trend line, but some remain bullish

Bitcoin’s price closed the weekly candle in a disappointing position thanks to last-minute downside wiping value from crypto as a whole.

The removal of various altcoins by certain trading platforms concerned about U.S. legal ramifications sent prices tumbling, leading BTC/USD to its lowest weekly close since mid-March, data from Cointelegraph Markets Pro and TradingView shows.

In doing so, the pair also locked out the 200-week moving average (MA) as support.

“A BTC Weekly Candle Close below the 200-week MA could confirm it as a lost support,” trader and analyst Rekt Capital warned beforehand.

“In that case, $BTC could relief rally into the MA next week, potentially to flip it into new resistance. This sort of turn of technical events could precede additional downside.”

Michaël van de Poppe, founder and CEO of trading firm Eight, held similar concerns about the fate of the total crypto market cap.

Mayday, mayday.

Total market capitalization is beneath the 200-Week MA and EMA.

Needs to get back above $1.04T during this week to avoid further downwards momentum for #Crypto. pic.twitter.com/J5lb8G5APU

— Michaël van de Poppe (@CryptoMichNL) June 12, 2023

With traders’ downside targets already extending to $24,000 and below, some took the opportunity for more optimistic takes on both shorter and longer timeframes.

Daan Crypto Trades noted upside potential thanks to the weekend losses opening up a CME futures gap.

That gap stands between $26,150 and $26,500, with BTC/USD previously “filling” another within hours.

Continuing, popular trader Credible Crypto insisted that despite everything, long-term resistance levels for Bitcoin would not pose much of a problem in the end. $40,000, he repeated, was still a target of choice.

“When you have a major correction down and folks are underwater there is resistance to the upside as moves up are sold into by bag holders. When you have capitulation down and folks have been drowned (forced to sell at the bottom) that sell pressure no longer manifests as we move up because ‘there is no one left to sell,’” part of weekend Twitter commentary read.

“If bag holders dumped at the bottom then the only sell pressure above is from short term traders/profit takers and that’s not enough to stop a major impulsive move in its tracks for long. Expect ‘major resistance levels’ above to get melted through a lot faster than most are expecting.”

Bitcoin runs gauntlet ahead of “massive” macro week

The coming week offers a rare deluge of potential crypto price triggers from the broader economic and geopolitical establishment.

MASSIVE Week:

Monday:

– Deadline for Binance and Binance US to respond to SEC’s application for a temporary restraining orderTuesday:

– Motion for temporary Binance US restraining order hearing

– Hinman’s documents release (XRP)

– CPI Data ReleaseWednesday:

– US Rate…— Daan Crypto Trades (@DaanCrypto) June 12, 2023

In addition to the ongoing ramifications of the U.S. Securities and Exchange Commission (SEC) vs. multiple exchanges, macroeconomic data promises volatility of its own.

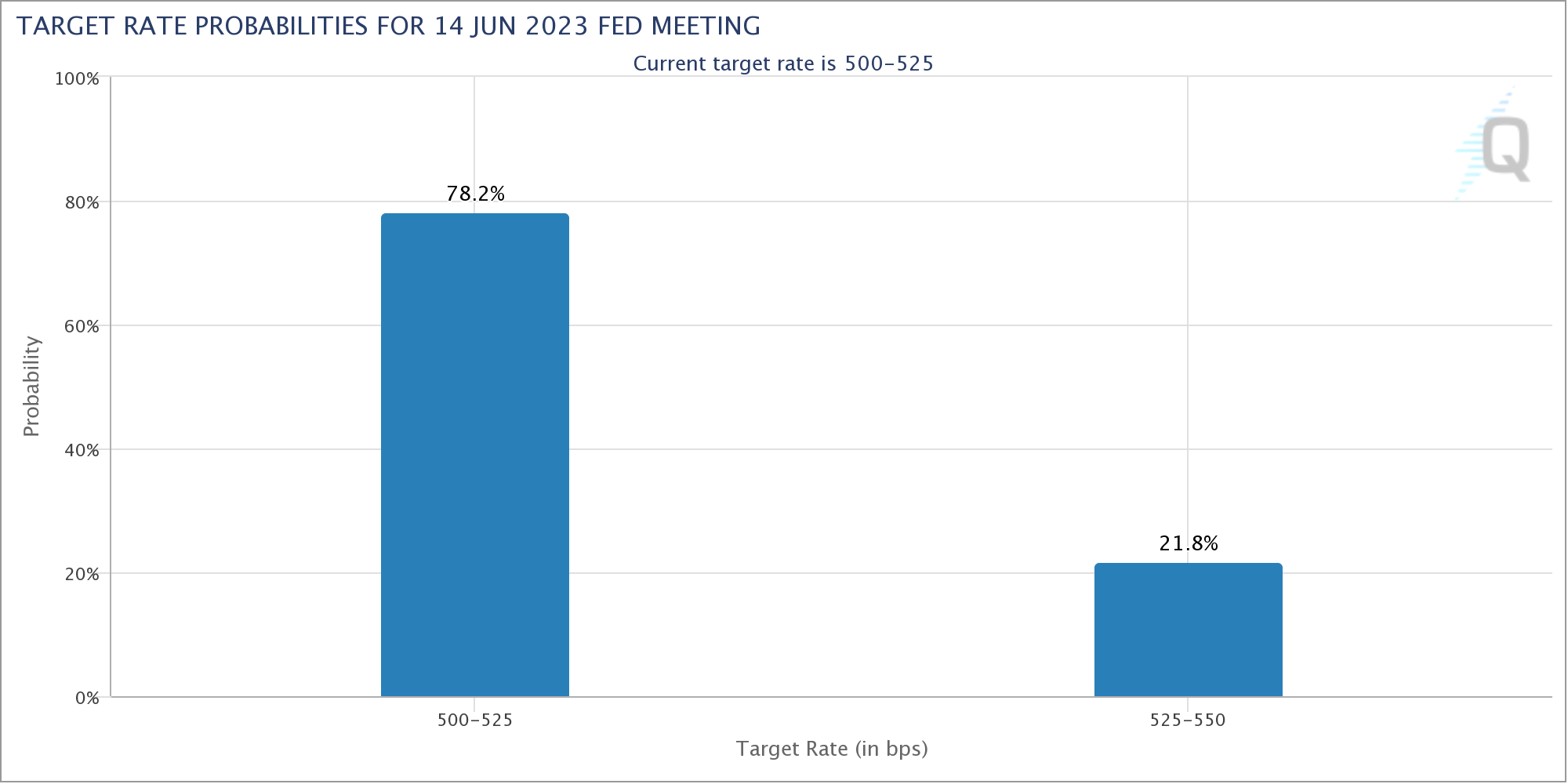

June 13 will see the May print for Consumer Price Index (CPI) inflation, and unlike last time, markets expect the Federal Reserve to pause interest rate hikes.

This would end an uninterrupted hiking cycle that began in late 2021, just as Bitcoin hit its all-time high.

According to CME Group’s FedWatch Tool, the odds of a pause stood at 75% at the time of writing on June 12.

With a loosening of economic conditions on the horizon, market commentators within crypto and beyond are considering the odds of a risk asset rally.

Biggest opportunity for equities to go higher? Rapid decline in inflation as rents and food costs come down, which allows Fed to pause int rate hikes in June and ultimately reduce rates by Y.E.

Biggest risk? Narrow breadth.

– Eight stocks account for 30% of S&P 500 market cap… pic.twitter.com/WePpRfNzxz— Gary Black (@garyblack00) June 12, 2023

“Pretty convinced that the money maker this week is A Fed Pause/Skip which sends $BTC past 30k,” popular trader Traderhc told Twitter followers.

Fellow trader Skew added that the CPI event would “likely set the mood” for the week’s price action.

In addition to CPI, meanwhile, the June meeting of the Federal Open Market Committee has the potential to spark market-moving soundbites from Fed chair Jerome Powell.

The rates decision is due June 14, alongside an announcement from the European Central Bank a day later. June 15 will see additional macroeconomic data releases.

Before all that, however, the fallout from the SEC vs. Binance and Coinbase saga may already move prices.

“Tomorrow will be a big day for the market,” Philip Swift, co-founder of trading suite DecenTrader, predicted on June 11.

“The SEC has to respond to Coinbase’s request for rulemaking… …and US district court hears SEC’s petition for temporary restraining order on binance US at 2pm. Buckle up.”

Bitcoin fundamentals to the moon

As is often the case with Bitcoin, short-term price action is meeting its match in underlying network data, which displays an altogether different trend.

This week, as with almost every week in 2023, network difficulty and hash rate are aiming for new all-time highs.

Hash rate is already higher than ever, according to some estimates, while difficulty will increase by approximately 2.5% on June 14. This will take it past 53 trillion for the first time.

Data from monitoring resource BTC.com confirms that network fundamentals are in “up only mode” despite BTC price pressures, with 2023 only seeing three difficulty reductions out of 12 adjustments in total.

“Bitcoin hashrate will not stop growing. This is insane,” Mitchell Askew, social media associate at Blockware, reacted.

“Mining is ruthless, free-market competition in its purest form.”

As Cointelegraph often reports, the concept of Bitcoin spot price following hash rate, in particular, has long been a mantra for industry stalwarts, among them the popular but outspoken BTC advocate Max Keiser.

Miner exchange inflows jump

LookIntoBitcoin founder Phillip Swift, nonetheless, described the current difficulty levels as “increasingly challenging” for all but the most robust miners.

#bitcoin Miner Difficulty just made a new all-time-high!

An increasingly challenging environment for any underperforming miners.Difficulty now at 51.2 Terahashes.

Free live chart: https://t.co/dEnNrrD4l4 pic.twitter.com/V8QNKyXAPv

— Philip Swift (@PositiveCrypto) June 9, 2023

Data from on-chain analytics firm Glassnode meanwhile tracks the onboarding of miners in real time.

“Despite an uncertain Macroeconomic environment alongside intensifying regulatory pressure, ASICs continue to come online as the Bitcoin Hash Rate (7DMA) reaches an ATH of 381 EH/s,” researchers commented on a chart of hash rate.

“This is equivalent to 381 quintillion guesses attempted every second to solve the Block puzzle.”

Glassnode data meanwhile appears to show miner inflows to exchanges hitting their highest daily levels since 2019 last week.

Across the past week, #Bitcoin Miners have been sending a significant amount of coins to Exchanges, with the largest inflow equal to $70.8M.

This is the 3rd largest inflow on record, -$30.2M less than the peak inflow of $101M recorded during the primary bull market of 2021. pic.twitter.com/w4fNFMcxr4

— glassnode (@glassnode) June 11, 2023

Following up, James Straten, research and data analyst at crypto news and insights platform CryptoSlate, flagged mining pool Poolin as the likely main contributor to the flows.

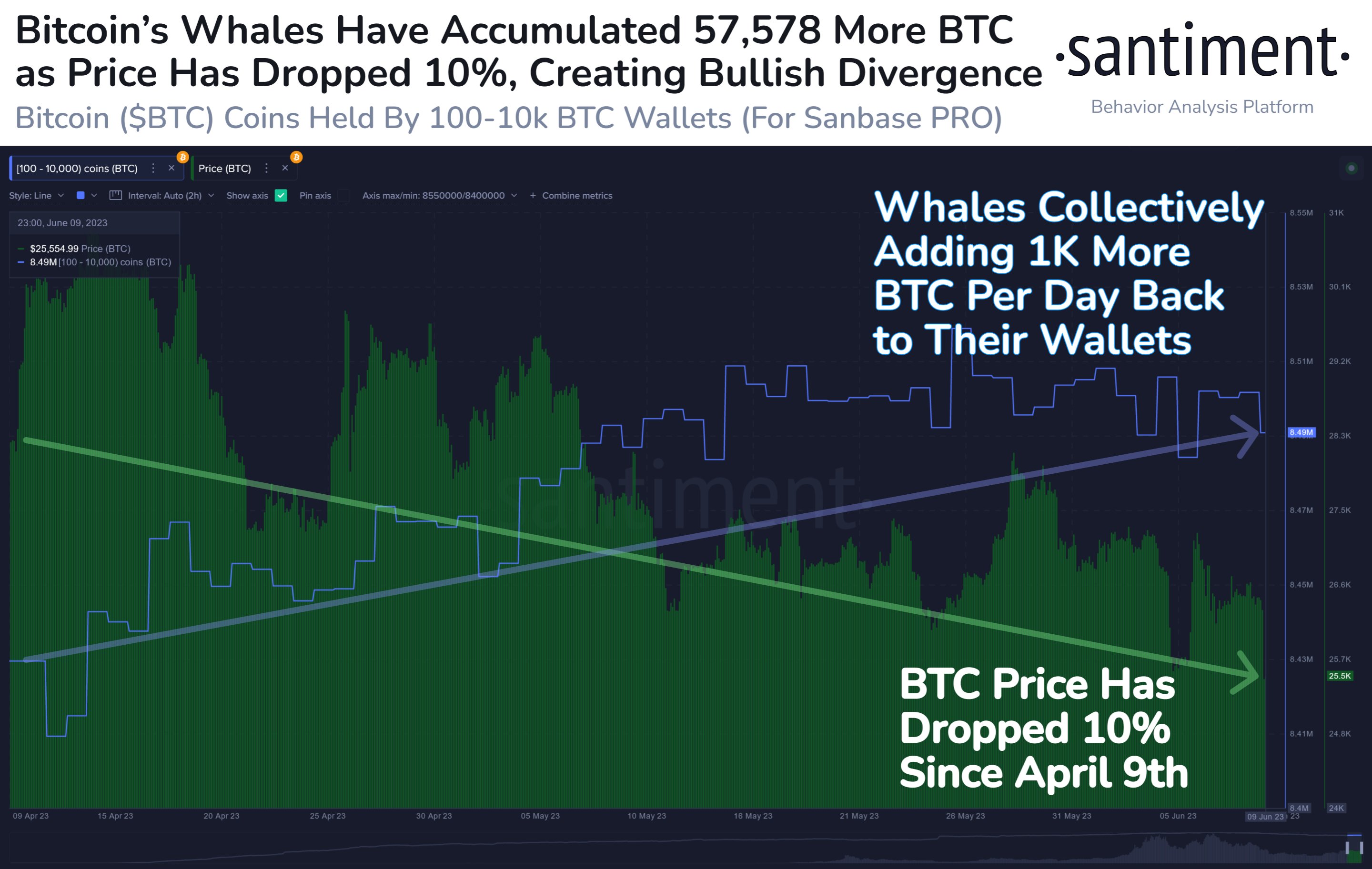

Whales boost BTC exposure during altcoin sell-off

Analyzing the impact of the latest crypto market upheaval, research firm Santiment saw cause for bullishness.

Related: A sideways Bitcoin price could lead to breakouts in ETH, XRP, LDO and RNDR

This, it argued in findings published on June 11, is thanks to the buying conviction of Bitcoin’s largest-volume investor cohort — the whales.

As Cointelegraph previously reported, the largest class of whales has diverged from the rest of the investor base since May, accumulating while others distribute BTC.

With altcoins tumbling at the weekend, whales appeared to take the opportunity to increase, rather than decrease, BTC exposure.

“As altcoin madness has ensued, there quietly is a bullish divergence between Bitcoin’s accumulating whales and falling price,” Santiment commented.

“With whale holdings moving up by ~1K $BTC per day while prices fall, there is reason to believe a strong rebound can occur.”

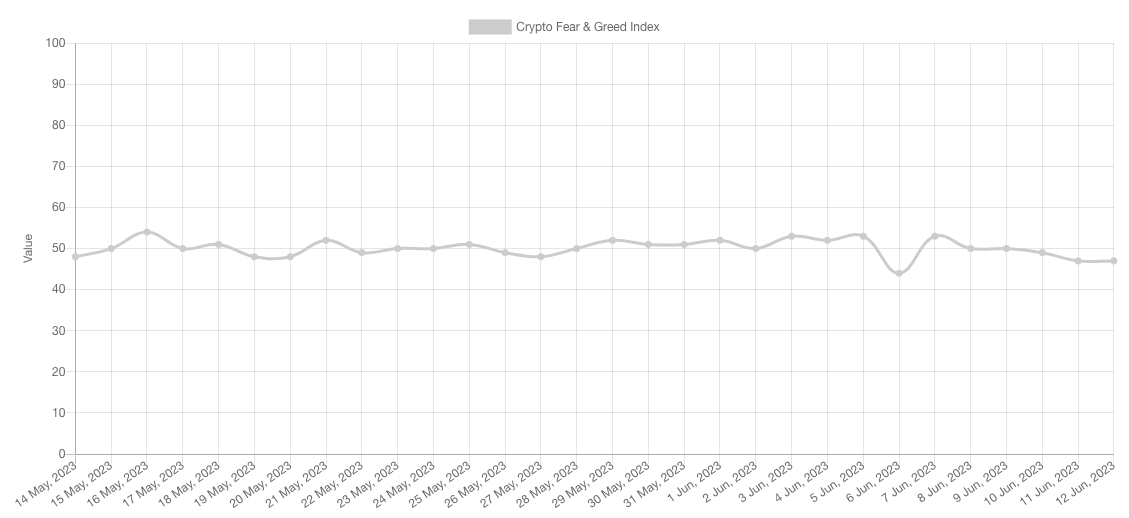

At the same time, sentiment across the broader crypto market continues to reject knee-jerk reactions to the news.

The Crypto Fear & Greed Index remains in “neutral” territory, having barely moved in recent weeks, hovering around the exact center of its 0-100 scale.

Magazine: Tornado Cash 2.0: The race to build safe and legal coin mixers

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.