The idea of a digital U.S. dollar had an early behind-the-scenes advocate inside the Trump administration in the president’s son-in-law, newly unearthed documents show.

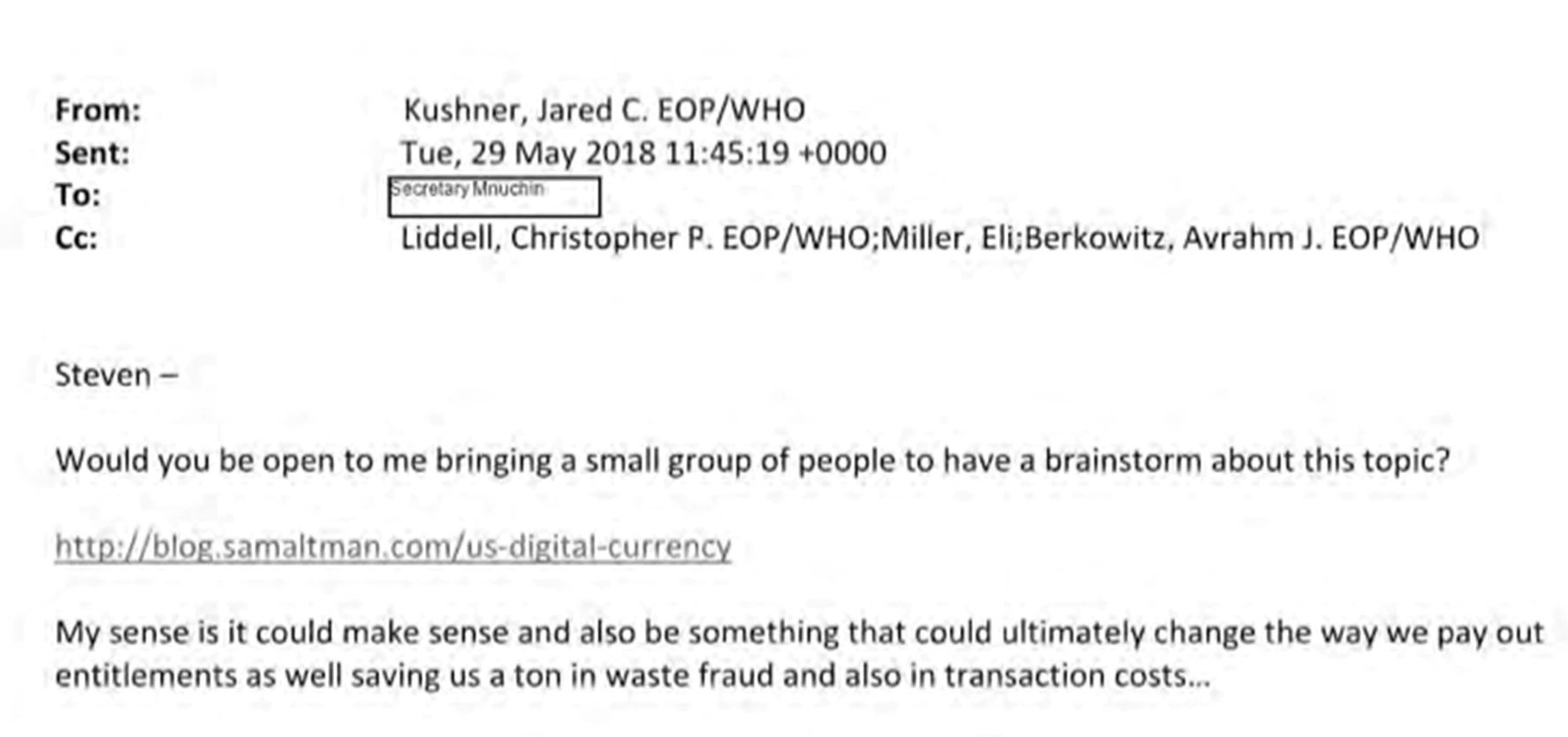

On May 28, 2019, Jared Kushner, special adviser to the president and Ivanka Trump’s husband, emailed Treasury Secretary Steven Mnuchin. The message included a link to a blog post by Sam Altman, former head of Y Combinator, the Silicon Valley startup incubator.

The title of the post: “U.S. Digital Currency.”

“Steven – Would you be open to me bringing a small group of people to have a brainstorm about this topic?” Kushner wrote.

“My sense is it could make sense,” Kushner continued, “and also be something that could ultimately change the way we pay out entitlements as well saving us a ton in waste fraud and also in transaction costs…”

Kushner took on many duties during his time at the White House. He had a major role in foreign policy spanning from Mexico to Iraq, as well as assignments to oversee criminal justice reform and an overhaul of the government itself. Some critics saw that broad workload as untenable, but Politico has credited Kushner with real progress on stabilizing the Middle East.

But Kushner’s interest in digital currencies, national or otherwise, was previously unreported (except the time someone tried to extort bitcoin from him). It’s one of several insights gleaned from a 250-page trove of Mnuchin’s crypto-related correspondence during his four years at Treasury.

Obtained by CoinDesk through a Freedom of Information Act (FOIA) request, the documents also shed light on the challenges presented to the crypto industry by international sanctions and the controversy over Mnuchin’s eleventh-hour proposal on user-controlled wallets. They also contain some unintended comedy as crypto VIPs met with D.C. power players.

Kushner seems to have been meaningfully ahead of the curve in contemplating a digital dollar. Discussion of central bank digital currencies (CBDCs) didn’t pick up broadly until late 2019, after the announcement of Facebook’s Libra project was met with ferocious backlash and China got serious about its digital yuan.

The U.S. Federal Reserve, for its part, has been studying the issue of CBDCs, but it has yet to publish any of the long-promised reports detailing the central bank’s position on technological and policy considerations for a digital dollar. Much of the push for a U.S. CBDC has come from the private sector.

It’s also interesting to look back at Altman’s thinking, including his proposal that a U.S. digital currency “would be evenly distributed to U.S. citizens and taxpayers – something like everyone with a social security number gets two coins.”

That jibes with Altman’s current plan for WorldCoin, a token intended to be distributed globally as a form of universal basic income.

It is unclear whether the meeting Kushner proposed to Mnuchin happened. Through an intermediary, Mnuchin declined to comment for this story. Kushner did not respond to requests for comment, nor did Altman.

A plea from Ukraine

In the FOIA request, submitted last March, CoinDesk asked the Treasury for any emails from Mnuchin’s time in office (February 2017 to January 2021) that included the word “cryptocurrency” or several synonyms (“virtual currency,” “digital asset,” etc.) or mentioned prominent companies in the industry like Coinbase or Ripple.

Nine months later, a Treasury FOIA officer sent CoinDesk 100 pages in full and 133 pages in part. The officer completely withheld 13 pages, citing the federal disclosure law’s exemption for trade secrets and personal privacy.

Even so, the documents offer a new window into how a key corner of the U.S. government approached global crypto policy under Trump.

It was an administration often criticized for neglecting America’s partners abroad. Sometimes that tendency carried over to crypto.

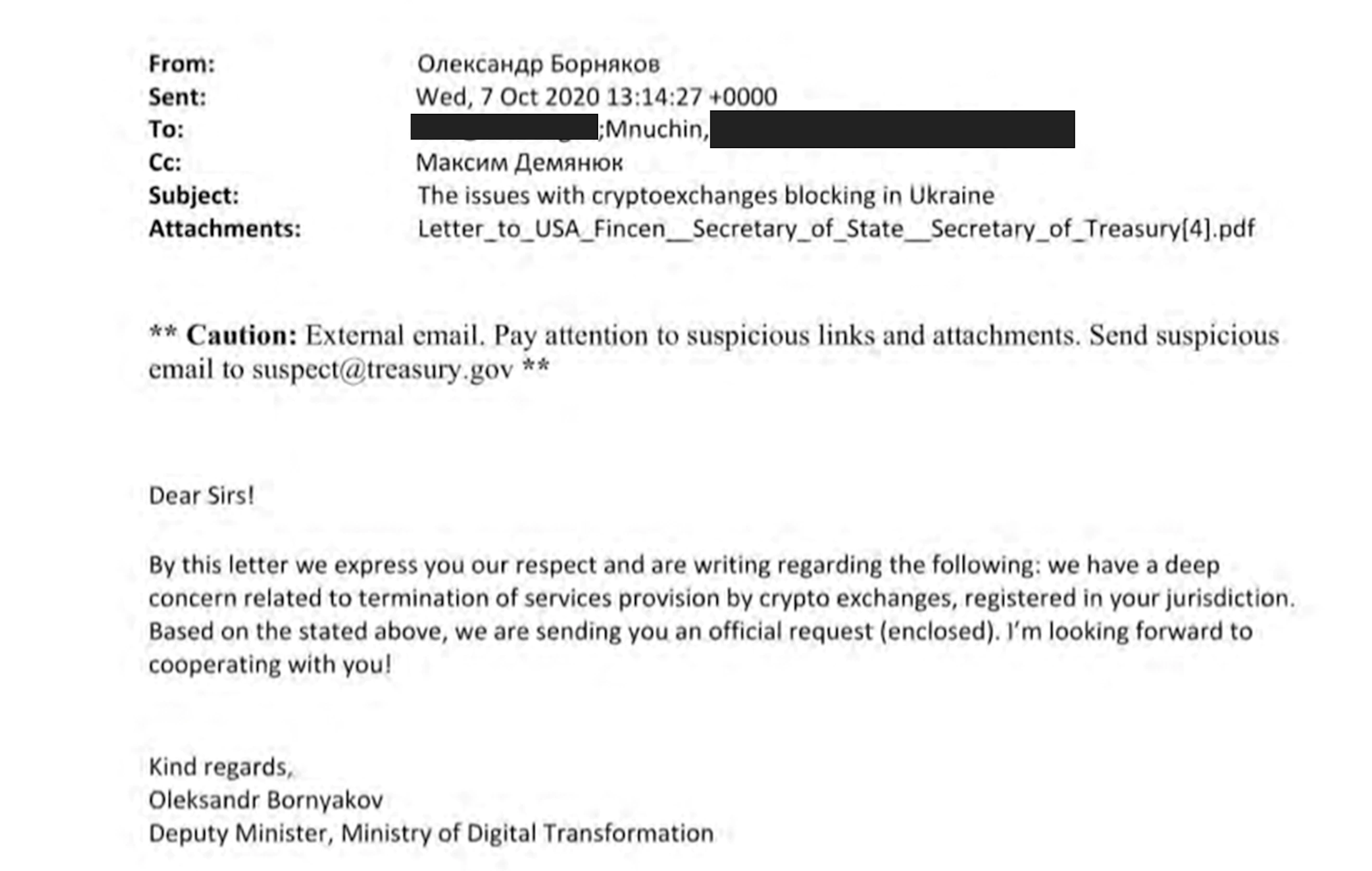

On Oct. 7, 2020, Oleksandr Bornyakov, Ukraine’s deputy minister of digital transformation, sent an email to Mnuchin asking for assistance with an unusual problem: U.S. cryptocurrency exchanges Coinbase, Bittrex and Gemini had pulled out from Ukraine.

“We have a deep concern related to termination of services provision by crypto exchanges registered in your jurisdiction,” read the email, addressed to Mnuchin and Mike Pompeo, then Secretary of State.

One of the exchanges Bornyakov mentioned in his correspondence was Bermuda-registered Bittrex. In a 2020 blog post, Bittrex vaguely blamed the “current regulatory environment” for its decision to discontinue service to Ukraine and a handful of other countries and declined to elaborate when contacted by CoinDesk the following year.

Bornyakov reached out to Bittrex, which told him it had concerns about potential users from the Crimean Peninsula, he told CoinDesk last May. Russia annexed Crimea from Ukraine in 2014, but most countries still don’t recognize the peninsula as part of Russia. The U.S. and European Union imposed sanctions on Russian individuals and companies that were related to the annexation or benefited from it. The EU also restricted imports and investments in the economy of Crimea by European companies.

Bittrex told the Ukrainian government it couldn’t identify Crimea residents specifically, which meant the company was at risk of violating sanctions on the peninsula if it continued to serve Ukraine.

But it wasn’t Ukraine that was under sanctions, Bornyakov emphasized in his letter.

“Please rest assured that we do respect all the laws and regulations, adopted in the USA,” Bornyakov wrote. He insisted that Ukraine’s 44 million citizens shouldn’t become collateral damage in a sanctions war targeted at Crimea, population 2 million.

“This is why there is a strong need of issuing the respective clarification” to U.S. crypto exchanges that would “eliminate any misunderstandings” and bring service back online, Bornyakov wrote. He asked for an update on “next steps.”

Bornyakov never heard back from the Treasury about his request, he told CoinDesk recently.

Asked for Mnuchin, got Muzinich

The trove of documents also shows the lengths the blockchain industry went to discourage Mnuchin from pursuing the Trump administration’s widely panned, last-minute proposal on user-hosted cryptocurrency wallets. These are wallets where the funds are controlled by the individual, not a company subject to regulation – more like a leather wallet full of cash than a bank account.

Mnuchin had warned during Congressional testimony in February 2020 that “significant new requirements” for cryptocurrency would be coming “very quickly.” But he gave no details then, and the proposal did not come until the waning days of the administration.

The lobbying efforts began at least a month before the proposal finally dropped. On Nov. 17, 2020, Kristin Smith, executive director of the Blockchain Association, emailed the Treasury Department asking to meet with Mnuchin about self-hosted wallets. Her organization had just released a 50-page policy report on the topic, she noted.

“We had heard for [a] few months prior that Treasury had concerns over self-hosted wallets,” Smith told CoinDesk recently. “At the time, we had hoped to use the report as a way to educate policymakers in the new year, but the timeline accelerated when we learned that Treasury was pursuing a midnight rulemaking.”

A week later, Coinbase CEO Brian Armstrong tweeted that the Treasury intended to impose onerous requirements for self-hosted wallets.

The Financial Crimes Enforcement Network (FinCEN), a bureau of the Treasury that combats money laundering and terrorism financing, formally proposed the rule and solicited public comment on Dec. 18, 2020, a week before Christmas. The rule would have required crypto exchanges to collect counterparty information, including names and addresses, from anyone hoping to transfer or receive cryptocurrencies to or from self-hosted wallets. FinCEN said it was concerned that the lack of information about users of such wallets created a blind spot in the government’s efforts to combat terrorism financing.

“Mnuchin was heavy on national security,” said a former Treasury staffer. “That was his big focus.”

“Mnuchin was heavy on national security,” said a former Treasury staffer. “That was his big focus.”

The proposal, which insiders say was likely instigated by Mnuchin rather than FinCEN itself, was met with widespread opposition from the industry. Participants worried it would be impossible to comply when the counterparty is an automated smart contract with no name or physical address, and others were concerned about burdensome compliance requirements.

After FinCEN issued the proposal, Smith re-upped her request, offering in a follow-up email to bring some of the association’s member entities on a call with Mnuchin.

An undisclosed Treasury official forwarded the request to Justin Muzinich, then the Deputy Treasury Secretary and two other undisclosed officials, writing, “Didn’t Justin [Muzinich] speak to them? Do you know why this might be coming back up to stm [Secretary Treasury Mnuchin?]”

One of those other officials responded, cryptically, “DELIBERATIVE” in an email that was otherwise redacted.

Mnuchin does appear later on the thread, authorizing Muzinich to take the call.

That call “lasted about five minutes,” Smith later told CoinDesk. “I recall that he called my mobile directly so I wasn’t able to loop in any of our association members. I was able to walk through some high-level talking points, but I remember feeling that this was just a check-the-box type call.”

‘De facto ban’

The trade group didn’t give up. Paul Clement, an attorney with the law firm Kirkland & Ellis LLP, wrote another letter to Mnuchin on the Blockchain Association’s behalf at the end of December 2020, explaining his concerns with the process of creating the proposed rule.

He echoed broader industry concerns about the 15-day public comment period (this was later extended several times) FinCEN provided for input. It is customary for U.S. regulatory agencies to give the public at least 30 and usually closer to 90 days to comment on proposed rule changes.

“The notion that stakeholders could meaningfully engage with a rule that touches on more than 24 separate subjects in such a highly truncated period would be doubtful even in the ordinary course,” the letter says.

“Thus, what purports to be just a reporting requirement may well operate as a de facto ban,” Clement wrote.

He warned that the rule might not stand up to a court challenge, providing examples of case law that suggested the proposal was being rushed unnecessarily.

Read more: Self-Hosted Bitcoin Wallets Become Front Line in Fight Over Crypto Regulations

Nor was the Blockchain Association the only group trying to address the wallet rule concerns.

The rule appears again in a Dec. 22, 2020 email sent to Mnuchin, Keith Abouchar, who appears to be a staffer for Rep. Steny Hoyer (D-Md.) and the Biden transition team. While the “from” field is redacted, this email contains a public letter originally published by the Electronic Frontier Foundation (EFF).

The proposed rule appeared rushed, could prevent broader adoption of crypto and wouldn’t allow for cash-like transactions due to the privacy implications, the email said. An EFF employee said no one from the foundation sent the email, but anyone could have copied and emailed the public letter.

A Jan. 21, 2021 email from an undisclosed sender also “urged” Mnuchin to remove the counterparty information requirement from the unhosted wallet rule, saying it could result in “a more burdensome standard” on cryptocurrency transactions than exists for cash and checks.

In the end, the rule was quietly shelved under the Biden administration. FinCEN extended the comment period several times before announcing it would review the rule months later. The rule hasn’t come up again.

No +1s allowed

Much of the crypto-related traffic in Mnuchin’s inbox is more human-sized, sometimes to an amusing degree.

For example, sorting out security clearance for an eagerly awaited Treasury-hosted crypto summit of March 2, 2020, appears to have been tricky.

Increasingly frantic email exchanges highlight the complexity that went into this unprecedented gathering of high-ranking government officials from the Treasury, FinCEN, the FBI and other agencies, who met face-to-face with a gaggle of crypto bigwigs from firms like Coinbase, Xapo, Square and Fidelity.

At the time, the Treasury announced that the meeting happened but didn’t provide any details about who was involved.

The Treasury’s searching and unpredictable know-your-crypto-industry-guest protocol apparently caused the most wrinkles to the entourage of then-Twitter boss Jack Dorsey, who went in his capacity as CEO of Square (now known as Block).

For instance, Mike Brock, head of strategic development at Square, was knocked back, despite brandishing the requisite driving license. Sounding like a character from a spy movie, one of Dorsey’s handlers messaged through that Brock’s attempt to clear security had been denied. “I told him to hold tight,” Square executive assistant Caitlin Friel Rabil said. “He’s outside the building waiting by the Secret Service booth. Is there any way you can let me know when he should try again?”

“We have learned that Coinbase, Xapo and Chainalysis all have been allowed to bring +1s and we would like to ask the same for Jack. Can you please let me know if Jack can bring a member of his staff with him on Monday?”

Square executive assistant Caitlin Friel Rabil

When it came to Dorsey himself, a couple of special requests were relayed over by his team. First, some additional guests were asked for, because word had got out that other delegates had been granted that courtesy.

“We have learned that Coinbase, Xapo and Chainalysis all have been allowed to bring +1s and we would like to ask the same for Jack. Can you please let me know if Jack can bring a member of his staff with him on Monday?” Rabil wrote on Feb. 28, the Friday before the meeting.

Dorsey’s handlers also asked if he could be driven up to a side door in order to hide his identity. (Kind of understandable; Dorsey is definitely more recognizable than your average businessman.)

“I noted on the invite that you suggest Jack go in through the North gate. Is there any way he can get closer via car just so he’s less visible, given the sensitivity of the meeting?” his assistant said.

The reply from Treasury was polite but firm: “As of right now no +1s will be allowed to join the meeting, it will be the invited principals only. I’m afraid he will have to be dropped off at the corner of 15th & New York Ave. and proceed on foot to the north entrance. There is no parking at the building.”

The only crypto VIP invited to the March 2 summit who did not attend was billionaire PayPal co-founder, venture capital investor and Trump supporter Peter Thiel, according to preparatory emails among Treasury officials.

CoinDesk reached out to Thiel and Dorsey but didn’t receive a response from either by press time.

What might have been

The March 2020 crypto summit was meant to kick off a series of working groups involving government and industry. The incipient crypto engagement program, however, was stopped in its tracks by the outbreak of the coronavirus pandemic, according to a source who worked at the Treasury at that time.

“We brought in a lot of industry leaders and we wanted a strong and friendly line of communication. Of course this all got put on the back burner because of Covid,” the Trump administration source told CoinDesk.

“I would say that now you just don’t see that level of engagement” under Biden, the former Treasury official said. “It’s almost zero from what I’ve seen. Instead, I think there’s a high level of antagonism right now.”

Indeed, Securities and Exchange Commission (SEC) Chairman Gary Gensler has continued, if not heightened, his predecessor’s antagonism toward the crypto industry. The regulator has continued serving enforcement actions and issuing subpoenas to individuals in the business. The SEC even subpoenaed a stablecoin founder right before he went onstage during a conference in New York late last year.

Industry participants are further concerned that the Treasury Department under Mnuchin’s successor Janet Yellen might bring the hammer down on crypto this year, when it explains how it will enforce a controversial tax provision in last year’s infrastructure bill that seeks to collect taxes from crypto brokers.

“I don’t think [Mnuchin] ever did anything that was especially good or especially bad for crypto, until that moment when he did something terrible.”

Jerry Brito of Coin Center

On the other hand, other parts of the Biden administration have been building bridges. Biden’s Commodity Futures Trading Commission (CFTC) chairman Rostin Benham, for example, put Jason Somensatto, formerly of decentralized exchange developer 0x Labs, in charge of the agency’s financial technology division, LabCFTC. Also, Yellen’s Treasury has focused its fight against ransomware on sanctioning exchanges, and that specificity has come as a relief to many crypto lobbyists.

Moreover, Mnuchin was far from solicitous toward the industry near the end of his tenure, when he tried to rush through the proposed rule requiring crypto businesses to verify the identity of counterparties with self-hosted wallets.

“I don’t think he ever did anything that was especially good or especially bad for crypto, until that moment when he did something terrible,” said Jerry Brito, executive director of Washington-based think tank Coin Center.

“We can never replay the videotape and see how it would have turned out if we hadn’t had a pandemic,” said Brito, one of the attendees at the March 2, 2020 meeting.

“One story is, you would have had a series of more roundtables with industry that would have resulted in great regulation,” he said. “Another possibility is that we would have had the unhosted wallet rule soon after. Hopefully, if you had had many more meetings, [Mnuchin] would have realized over the course of those meetings that was not a smart thing to do.”

It’s who you know

The trove of emails also underscores why, despite crypto’s disruptive promise, companies in the field have been hiring veterans of the legacy financial industry.

Coinbase Chief Financial Officer Alesia Haas “has a personal friendship with Secretary Mnuchin”, according to an email to the Treasury department from Kara Calvert, then a partner at the exchange’s D.C. lobbyist Franklin Square Group and now in-house. (Haas was previously CFO at OneWest, the bank Mnuchin ran.)

For that reason, Haas got added to a Treasury conference call with Brian Armstrong in May 2020 at Coinbase’s request, the email said.

Finally, and fittingly for the blockchain industry, the very first email in the 250-page pdf Treasury provided to CoinDesk is an investment pitch addressed to Mnuchin.

“Would you be interested in investing in our early stage round for accredited investors?” Dave Cohen, CEO of Taekion, wrote to the Treasury Secretary on Jan. 10, 2019. “If so, we can send detailed company info.”

Cohen described his company as “the first AI and blockchain based platform that will disrupt the global cybersecurity industry.”

It’s unclear if Mnuchin responded to Cohen, who didn’t reply to CoinDesk’s request for comment.

Nathan DiCamillo contributed reporting