From its early days, the crypto sector has grappled with regulation. We analyzed how the U.S. Securities and Exchange Commission (SEC) and its successive chairs have shaped crypto’s regulatory landscape over the years.

The U.S. Securities and Exchange CommissionSEC has had a less than friendly relationship with crypto, with its current chair Gary Gensler seen as the poster child for this perceived animosity.

But how did Gensler’s predecessors relate to the crypto industry? How did policies enacted under their tenures eventually shape the current regulatory environment? By delving into these historical contexts and examining how successive chairs contributed to the SEC’s rule book, we can better understand the evolution of the regulator’s approach to cryptocurrencies and the potential implications for the industry’s future.

The early days: Christopher Cox and Mary L. Schapiro

Crypto came into the limelight at the tail-end of Christopher Cox’s tenure as SEC Chair. Appointed by George W. Bush in 2005, Cox was the 28th occupant of the SEC’s topmost position, and while players in financial regulatory circles have credited him with enhancing transparency and accountability in financial reporting, he wasn’t around long enough to cast his shadow over the nascent crypto industry.

Satoshi Nakamoto, the pseudonymous inventor of Bitcoin (BTC), mined the cryptocurrency’s Genesis block on Jan. 3, 2009, two weeks before Cox left office to be replaced by Mary L. Schapiro.

Crypto largely flew under the radar during Schapiro’s tenure. The Obama appointee was understandably preoccupied with the aftermath of the 2008 financial crisis, in which many people heavily criticized the SEC for failing to detect Bernard Madoff’s massive Ponzi scheme.

However, under Schapiro, the agency embarked on one of its most comprehensive rulemaking agenda since the 1930s. It implemented numerous reforms designed to protect investors and strengthen the integrity of the American money market. These reforms included improving credit rating quality, enhancing disclosure, and regulating asset-backed securities.

Schapiro also made strides in modernizing the SEC’s enforcement program. She restructured the program to encourage greater collaboration and streamlined the process for approving formal investigation orders, enabling staff to act more swiftly to detect and prevent fraud.

Since Shapiro’s tenure as SEC Chair predates the rise of cryptocurrencies, many of the reforms she implemented have shaped the agency’s approach to regulating all types of securities, including digital assets.

The epoch of change: Elisse B. Walter and Mary Jo White

The SEC’s momentous journey with digital assets began to take shape with Mary Schapiro’s exit on December 14, 2012. Elisse B. Walter initially replaced her in an acting capacity, with Mary Jo White taking over the role nearly five months later in April 2013.

Walter’s tenure, though short-lived, was marked by the regulator’s initial survey of the potential implications of digital assets on investors and the broader markets. Despite the absence of significant enforcement actions involving crypto during her reign, she sowed the seeds for a structured regulatory framework.

Her successor, Mary Jo White, took the helm from April 10, 2013, until January 20, 2017. White’s era witnessed the SEC’s proactive stance towards cryptocurrencies come to fruition. Under her stewardship, the agency made its first significant enforcement move in the crypto realm, charging a man and his company for a Bitcoin-oriented Ponzi scheme.

White’s term also saw the SEC’s watershed decision to turn down the first Bitcoin exchange-traded fund (ETF) proposal, flagging concerns over market manipulation and a regulatory vacuum in Bitcoin markets. This turning point underscored the uphill battle faced by digital assets in their quest for mainstream financial acceptance.

The crypto community had a polarized response to these developments. While some saw the SEC’s watchful eye as a speed bump on the road to innovation, others embraced it as a much-needed step towards legitimizing cryptocurrencies and safeguarding investors.

Walter and White’s times in office laid the foundation for the SEC’s ongoing dialogue with the crypto industry. They embarked on a journey through unknown territories, wrestling with the task of fitting existing securities laws into a rapidly morphing digital asset landscape.

The enforcement era: Jay Clayton

Appointed by President Donald Trump, Jay Clayton took the reins as SEC chairman between May 2017 and December 2020. As the crypto industry flourished, it fell upon Clayton to steer the SEC through the complexities of the emerging techno-financial landscape, which often shook the pillars of traditional regulatory norms.

A cornerstone of Clayton’s tenure was his stance towards Initial Coin Offerings (ICOs), a new, volatile market that reached a fever pitch in 2017. Amid the frenzied excitement, Clayton sought to ground investors by highlighting the inherent risks and underlining that tokens marketed in ICOs could potentially be securities by definition. It resulted in a heightened regulatory gaze towards ICOs, with the agency taking direct action against several crypto projects.

During Clayton’s term, many stablecoins—cryptocurrencies engineered to resist dramatic price fluctuations—debuted. While acknowledging the prospective benefits of stablecoins, the Clayton-led SEC voiced concerns regarding their regulatory difficulties, especially if deemed securities.

The question of defining cryptocurrencies as securities turned into a pivotal debate during Clayton’s era. He maintained that numerous cryptocurrencies fell under the securities umbrella, thus falling within the SEC’s regulatory purview. This viewpoint ignited continued contention within the crypto community, with some deeming it a potential roadblock to innovation.

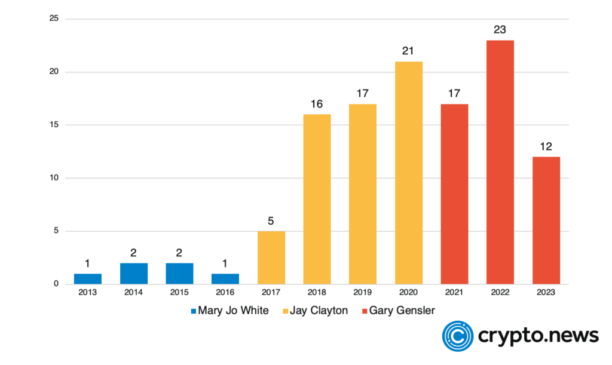

Throughout Clayton’s tenure, the SEC launched 56 lawsuits against firms operating within the crypto domain, reinforcing his dedication to upholding securities laws even in digital assets. These enforcement actions triggered a ripple effect in the crypto industry, catalyzing a surge in compliance initiatives.

Major crypto cases under Clayton

SEC vs. Telegram Group Inc.

In late 2019, Telegram Group Inc. and its affiliate TON Issuer Inc. found themselves in hot water with the SEC. The agency took legal action against them, suggesting they had sidestepped regulations when selling their Gram tokens.

Telegram, familiar to many as a messaging platform, had made a foray into the crypto domain by launching the Telegram Open Network (TON) and its associated Gram tokens. The company succeeded in raising close to $1.7 billion from token sales in the first quarter of 2018 alone.

The SEC’s contention was that the sale was tangibly a securities offering and should have been officially registered with them. They anchored their argument on the assertion that Telegram’s Gram tokens fell under the category of securities as per U.S. law, thus making their sale a violation of the Securities Act of 1933.

The regulator believed that investors were essentially banking on Telegram’s management for profits rather than just owning the Gram tokens. Telegram fired back, arguing that Grams were currencies and not securities, positioning them outside the SEC’s purview.

Nonetheless, in March 2020, the SEC secured a preliminary injunction from a U.S. District Court, stalling the distribution of Gram tokens. Following this, Telegram agreed to refund investors to the tune of over $1.2 billion and also decided to cough up an $18.5 million civil penalty.

SEC vs. Kik Interactive Inc.

In June 2019, the SEC filed a lawsuit against Kik Interactive Inc., alleging that the company’s $100 million ICO for its Kin tokens was an unregistered securities offering.

The SEC claimed that Kik had marketed its ICO to investors as an opportunity for profits, primarily from Kik’s efforts to create, develop, and support a market for the tokens.

A key precedent, in this case, was the application of the Howey Test, a standard used to determine whether an asset qualifies as a security.

The court’s decision to grant the SEC’s motion for summary judgment, ruling that Kik’s ICO was an unregistered securities offering, underscored the broad applicability of the Howey Test in the context of digital assets.

SEC vs. Ripple Labs Inc.

In the final stages of Clayton’s tenure, Ripple Labs Inc., known for its XRP tokens, became the target of a lawsuit by the SEC. The suit was launched against the company, its CEO Brad Garlinghouse, and co-founder Christian Larsen.

The regulator accused Ripple Labs of raising over $1.3 billion through an unregistered securities offering. In an unexpected redux, the SEC dusted off its interpretation of the Howey Test, asserting that XRP tokens bear the hallmark of securities under U.S. jurisprudence.

The crux of this test is whether the anticipated profitability of an investment hinges predominantly on the efforts of external entities, thereby slotting it into the security category.

Come July 2023, which marked over thirty months since Clayton left the SEC, a verdict on the litigation was handed down by a U.S. federal judge. She cast her lot partially with Ripple, decreeing that transactions involving the procurement of XRP tokens via exchanges didn’t fall under the umbrella of securities transactions.

This judgment has subsequently etched itself as a crucial yardstick in the governance of cryptocurrencies and the classification of digital assets. Yet, the SEC has dropped hints of a potential counterstrike against the ruling.

If they clinch a victory, it could pave the way for stringent oversight of select cryptocurrencies, potentially smothering the flame of innovation within the industry, according to insiders like Garlinghouse and Coinbase CEO Brian Armstrong.

The current state: Gary Gensler

On April 18, 2021, the SEC Chair’s mantle was laid upon Gary Gensler’s shoulders. From the moment he assumed his post, Gensler has held a seemingly unwavering, resolute stance on the regulation of digital assets.

Gensler has underscored the need for all entities in the crypto space to operate within the boundaries of law, demanding comprehensive adherence to regulations. This stringent view has led Gensler to categorize the majority of cryptocurrencies as unregistered securities.

His application of securities laws demonstrated a steadfast commitment to their interpretation and enforcement. This dedication has acted as a driving force behind significant SEC actions, including a high-profile case against Coinbase, which will be further explored.

Gensler’s approach has initiated a wider response towards perceived rule breakers within the crypto market. His strategy has elicited a range of reactions from the crypto community. Some commend his actions to impose structure onto an often untamed and unexplored market, while others suggest that his stringent stance may restrict innovation and create an atmosphere of regulatory uncertainty.

To rectify the perceived imbalance, certain key players within the industry have proposed that Gensler could chart a clearer path, one that reflects the relentless march of technological evolution within the sector. A faction within the community has also advocated for a shift from combative to cooperative tactics, a move that could harmonize regulation, the stimulation of growth, and the preservation of investor safeguards.

Yet, it is essential to remember the paramount duty of Gensler as the SEC Chair, to ensure the protection of investors, the fairness and effectiveness of markets, and their orderly conduct, should not be lost in the shuffle.

Legal cases

SEC vs. Coinbase

June 2021 witnessed the SEC thrust a legal challenge in Coinbase’s path. The accusation? A violation of securities laws via the exchange’s staking program. The regulator posited that Coinbase was operating as an unregistered broker, clearinghouse, and exchange simultaneously, with a list of not less than 79 crypto assets.

The grounds for the SEC’s case were rooted in the belief that these digital assets should be categorized as securities per U.S. law, thus requiring registration with the SEC.

Undeterred, Coinbase mounted a spirited defense, asserting that the cryptocurrencies featured on its platform didn’t fall under the SEC’s purview. They argued that these were not the typical “investment contracts” and hence did not slot into the securities bracket.

The crypto exchange further alleged an overreach by the SEC, accusing them of trampling upon its due process. As of July 2023, the lawsuit is ongoing, its final chapter yet to be written.

SEC vs. Binance

On June 5, 2023, the SEC launched a series of accusations against Binance, its founder, Changpeng Zhao, more commonly known as CZ, and its U.S. counterpart, BAM Trading.

The SEC claimed that, notwithstanding a public proclamation excluding U.S. customers from Binance.com, the exchange craftily allowed big-ticket American clients to carry on their trading activities on the platform.

The regulator also insinuated that Binance.US, pitched as an independent unit, was, in fact, stealthily functioning under the thumb of CZ and Binance. A further allegation revolved around the supposed misappropriation of user funds by CZ and Binance, redirecting these to Sigma Chain, another venture under CZ’s purview.

Adding to the onslaught of allegations, the SEC pointed fingers at BAM Trading and BAM Management US Holdings for painting a deceptive picture of their trading controls to investors, and purportedly funneling billions in investor money through another CZ-owned entity, Merit Peak Limited.

However, the storm seemed to subside somewhat on June 17, when Binance managed to strike a deal with the SEC to keep its U.S. operations afloat.

Pertaining to a consent order approved by Federal Judge Amy Berman Jackson in Washington D.C., it was agreed that all assets belonging to Binance’s U.S. customers would be refunded. This settlement put a leash on the defendants’ use of corporate funds, limiting them to routine business expenses, enforced SEC supervision on any expenditure, and banned the destruction of records.

The order also dictated that Binance establish new digital wallets for U.S. customers, moving their assets into these within a fortnight.

Assessing the influence of SEC chairs on the crypto industry

Our examination of the history of the SEC reveals that every chairperson that has led the agency since the advent of crypto has played a role in shaping the regulatory landscape for the industry in the United States. Let’s look at each individual’s effect on this ever-evolving industry.

- Mary L. Schapiro presided over the SEC before the rise of cryptocurrencies. However, her comprehensive rulemaking efforts set the stage for how the SEC would regulate all forms of securities, including digital assets. Schapiro aimed to safeguard investors and fortify the integrity of the financial markets, thereby laying a solid foundation for future regulations governing the crypto industry.

- During Mary Jo White’s tenure, the SEC started to adopt a proactive approach toward cryptocurrencies. She was at the helm when the agency took its first significant enforcement actions involving crypto, bringing charges against individuals and companies linked to Bitcoin-based Ponzi schemes. The denial of the first Bitcoin ETF proposal during her term underscored the hurdles digital assets faced in their quest for mainstream acceptance.

- A significant focus on ICOs and categorizing cryptocurrencies as securities marked the tenure of Jay Clayton. He underscored the importance of regulatory compliance in the crypto industry and launched several lawsuits against crypto ventures for alleged violation of securities laws. Clayton’s enforcement-centered approach sparked a wave of compliance efforts in the industry.

- A stringent approach to crypto regulation distinguishes Gary Gensler’s term as SEC Chair. He vocally advocates for compliance with securities laws and holds that most cryptocurrencies are unregistered securities. Gensler’s firm stance has led to numerous high-profile engagements with the crypto industry as he prioritizes investor protection and market integrity.

Although each SEC Chair has shaped crypto regulations uniquely, Gary Gensler’s impact appears to be the most profound to date. His determination to classify cryptocurrencies as unregistered securities and insistence on regulatory compliance has heightened market order and led to several notable engagements.

Gensler’s proactive enforcement approach and steadfast dedication to investor protection make him a significant influencer in the regulatory context for cryptocurrencies in the United States.

Nonetheless, with the rapid evolution of the crypto industry, the long-term effects of these regulatory measures may continue to unfold even after Gensler’s term.