Per the request of the United States Congress, the U.S. Government Accountability Office (GAO), laid out four policy options to help policymakers implement blockchain technologies while enhancing benefits and mitigating challenges.

The technology assessment shared by the GAO acknowledged the potential of blockchain technology in improving a variety of financial and non-financial applications despite raising concerns about introducing new challenges while trying to resolve issues related to traditional systems:

“A blockchain might both increase the speed of a title registry system and lower the cost of title insurance by making title registration simpler and more trustworthy.”

However, some of the challenges highlighted in the study include uncertain benefits, data reliability and legal compliance.

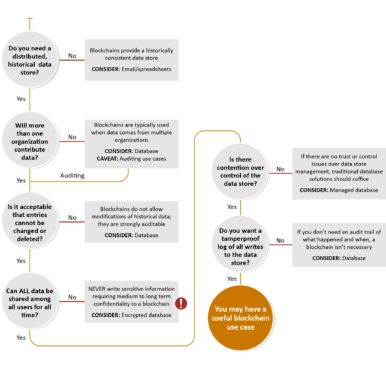

With the above flowchart, GAO aims to help policymakers — including Congress, federal agencies, state and local governments, academic and research institutions, and industry — determine the requirement of blockchain implementation.

Curious about blockchain and how it’s used? In our latest blog post, we dive into blockchain’s many uses and how to address emerging policy challenges. Find out more: https://t.co/ae21mF7IMg pic.twitter.com/F5puP4VIUJ

— U.S. GAO (@USGAO) March 24, 2022

The GAO assessment further highlighted various non-financial implementations of blockchain technology, as shown below.

While policymakers have the right to maintain the status quo, the GAO recommended four policy options to ease the decision-making process that goes behind mainstream blockchain implementation — standards, oversight, educational materials and appropriate uses.

With setting standards, GAO envisions tackling challenges around interoperability and data security. Some considerations include implementations of consensus mechanisms and establishing internationally recognized standards.

According to GAO, an oversight policy can “help address challenges with legal and regulatory uncertainty and regulatory arbitrage.” In addition, the GAO recommends the issuance of educational materials for addressing challenges around limited understanding and undefined benefits and costs.

The fourth policy option, appropriate uses, talks about mitigating challenges around risks to the financial systems and undefined benefits and costs. Highlighting the Commodity Futures Trading Commission’s (CFTC) lack of authority to collaborate with non-governmental entities, the assessment states:

“Legal or regulatory uncertainty may hinder some potential users from benefitting from blockchain.”

Related: US Virginia Senate allows state banks to offer crypto custody services

On March 5, the Senate of Virginia unanimously approved a bill amendment request that now allows traditional banks in the region to provide virtual currency custody services.

As Cryptox reported, the bill was introduced by Delegate Christopher T. Head back in January 2022, stating:

“A bank may provide its customers with virtual currency custody services so long as the bank has 26 adequate protocols in place to effectively manage risks and comply with applicable laws.”

The bill passed Senate with a sweeping 39-0 vote and is waiting to be signed into law by Governor of Virginia Glenn Youngkin.