I asked some friends who were Bitcoin noobies what they wanted to know about Bitcoin, and was ready with some answers. Here’s what we came up with.

Common Questions about Bitcoin, Answered

- How does mining work?

Mining is a key component of the Bitcoin system. It helps secure the network, is integral to the issuance of new coins, and in a sense ties everything together. But how does it work?

Well, it’s slightly complicated, so I’ll try to explain it in a condensed way that is simple but not “too simple”, so you hopefully get the gist of it:

On average every ten minutes, transactions on the Bitcoin network are bundled together into a “block”. But in order for a block to be accepted by the network, the creator of the block (i.e. “the miner”) needs to prove they did the proper “work”. This is known as “proof of work”.

Think of it like this: In order to create a block, you have to solve a math puzzle. The puzzles are hard to solve, yet easy to verify (sort of like a Sudoko puzzle). When a miner sends a solved block to the network, the other miners can quickly check if it’s correct, and then everyone starts working on the next block.

Obviously, unlike Sudoko puzzles, these proof-of-work “math puzzles” are solved by computers running the Bitcoin software, rather than people using a pencil and paper.

The puzzles are solved using brute force trial and error. There are scads of combinations tried every second from miners all around the world. In fact, a single miner will be computing trillions of “hashes” per second. You may hear the word “hash” or “hashing” being thrown around quite a bit in Bitcoin conversations. (You don’t really need to know what a mathematical hash function is, but essentially it is the math puzzle I am referring to).

In the early days of Bitcoin, mining could be done on any computer, simply with the computer’s CPU. Over the years, mining moved away from CPU to GPU, then to FGPAs, and finally to ASICs (Application Specific Integrated Circuits). Today, you need a specialized ASIC piece of hardware to mine (ordinary computers are far, far too slow.)

When a miner produces a block, they have to bundle all the transactions that will be included, and also refer back to the previous block. All this gets put into the hash function. Because each block refers to the previous, together they make a chain of blocks (hence the term “blockchain”).

Since the blocks are chained together, this is what creates the security for Bitcoin. No one can build an alternate history of transactions without redoing all the work for those blocks, and if this is attempted, the attacker will be too slow compared with the rest of the network that is continuing to extend the blockchain.

In addition to the normal transactions being bundled into blocks, miners are also allowed to include a special transaction on each block, called a coinbase transaction, which awards the miner with freshly minted coins. Thus, the mining process provides an economic incentive to participate in providing security, while it at the same executes the issuance schedule.

“Network hashrate” refers to the total aggregate amount of mining being done by all miners on the chain, and this tends to follow the price of the coin. The greater the financial rewards, the more the system attracts miners to compete for those rewards.

Finally, there is a difficulty adjustment, whereby, periodically the network will make it either easier or harder to solve blocks, based on how fast (or slow) blocks have been coming in. As the hashrate goes up, the difficulty will also adjust upwards, and the system will continually keep adjusting so that the average time between blocks is ten minutes.

- What are the other major coins besides Bitcoin (BTC)?

Ethereum (ETH) is the #2 coin by market cap today. Ethereum is similar to Bitcoin in that it uses an open source blockchain system, but it is more focused on smart contracts, which are computer programs that automatically execute agreements without the need for trusted intermediaries. Ethereum is often touted as being a kind of “world computer”, and is currently a backbone of decentralized finance (“DeFi”). Ethereum also hosts other coins known as “tokens”.

XRP (XRP) is a currency that runs on Ripplenet, a creation of Ripple Labs company. It aims to be an alternative to legacy financial systems like Swift. Unlike Bitcoin and Ethereum, XRP doesn’t use proof-of-work and instead is based on trusted validator nodes, which include universities and banks. XRP coins are issued by Ripplelabs.

Tether (USDT) is a coin that is pegged to the US dollar (also called a stablecoin). It doesn’t have its own blockchain and instead is issued on other blockchains including BTC, ETH, and BCH.

The peg is achieved by the Tether company maintaining dollars in a bank account, and other assets, equivalent in value to the number of circulating tethers. Tether has claimed that the coin is fully backed by USD reserves and similar assets, but some doubt this and Tether’s reserves have never been fully audited by a third party.

Litecoin (LTC) is similar to Bitcoin and is based on the Bitcoin protocol, but introduces some small changes, including faster block times and a different hashing algorithm. This algorithm was originally intended to allow more users to mine the coin, even if they do not have access to ASICS, although today ASIC mining has taken over LTC as well. Litecoin was created in 2011, making it one of the oldest coins.

Bitcoin Cash (BCH) is another major coin, and is a fork of Bitcoin (BTC). Forks allow factions of a community to split and go their separate ways when they run into irreconcilable differences. When there is a chain-split and one version of a coin splits into two different projects, holders of the original coin will then own coins on both networks.

The Bitcoin Cash project was born out of a chain split when the Bitcoin community could not agree on scaling the network in 2017. The side known as Bitcoin (BTC) has the clear economic majority at least in terms of price, but Bitcoin Cash has strong philosophical reasons for existing — namely, to continue the Bitcoin project as was originally intended: as reliable peer-to-peer electronic cash with low fees. By contrast, BTC has a limited capacity, which results in frequent periods of congestion and high fees when too many people try to use the blockchain at the same time.

3. What is the best Bitcoin wallet?

There are many options for Bitcoin wallets, and which is “the best” depends on your goals and level of experience. The highest security and most privacy comes from running your own Bitcoin full node, but this is not practical for most users, nor is it necessary.

For many users, the “best” (in my opinion) is the Electrum wallet (or Electron Cash for BCH) because it allows you to have high security without downloading the blockchain or running your own node. A distributed set of servers handle the heaviest parts of blockchain operations, but your own private keys to your coins are never sent to servers and only sign transactions locally. The electrum class of wallets are also open source, which increases their trust.

Another nice option (super for beginners) is the Bitcoin.com wallet. It’s a great way to get started using Bitcoin. It’s safe and easy.

4. How can I store Bitcoins safely?

Generally, your bitcoins should be stored in your own wallet and not kept on an exchange. As the old saying goes, “not your keys, not your coins”. This means that technically speaking when you have your coins on an exchange, you don’t actually own any coins. Instead, what you have is an IOU from the exchange.

Although this may feel like an unimportant distinction on the surface, there are real risks of keeping your money on an exchange. These risks include the exchange refusing to return your funds (either because of malice or regulatory issues), or the exchange getting hacked or going out of business, or a hacker getting into your account. If you must keep coins on an exchange, make sure to use a strong password and two-factor authentication (2fa).

When you have your coins in your own wallet, you are immune from many of the risks, but your coins can still be lost if you don’t back up your wallet and your computer dies, or if a hacker gets access. Keeping your computer up-to-date with malware and antivirus protection is recommended.

For even better security, you can look into using a hardware wallet, a paper wallet, or a cold storage wallet. We don’t have room here to do a deep dive into each of them, but it’s an excellent place for any aspiring Bitcoiner to start researching.

- How do you know if a bitcoin transaction is legitimate?

Beginners wonder how it’s possible to know if a Bitcoin transaction is legit if it’s just a bunch of data. Can’t that be faked? The short answer is that your wallet knows whether a transaction is valid, and usually won’t even display an invalid transaction.

As to how the wallet knows this, Bitcoin transactions must follow a very specific format, and can only spend coins (also sometimes called “inputs”) that are themselves valid and only if the user (wallet) can produce the correct digital signature.

- Is Bitcoin anonymous?

Yes and no. While Bitcoin transactions are not completely anonymous, not all transactions have a clear identity associated with them.

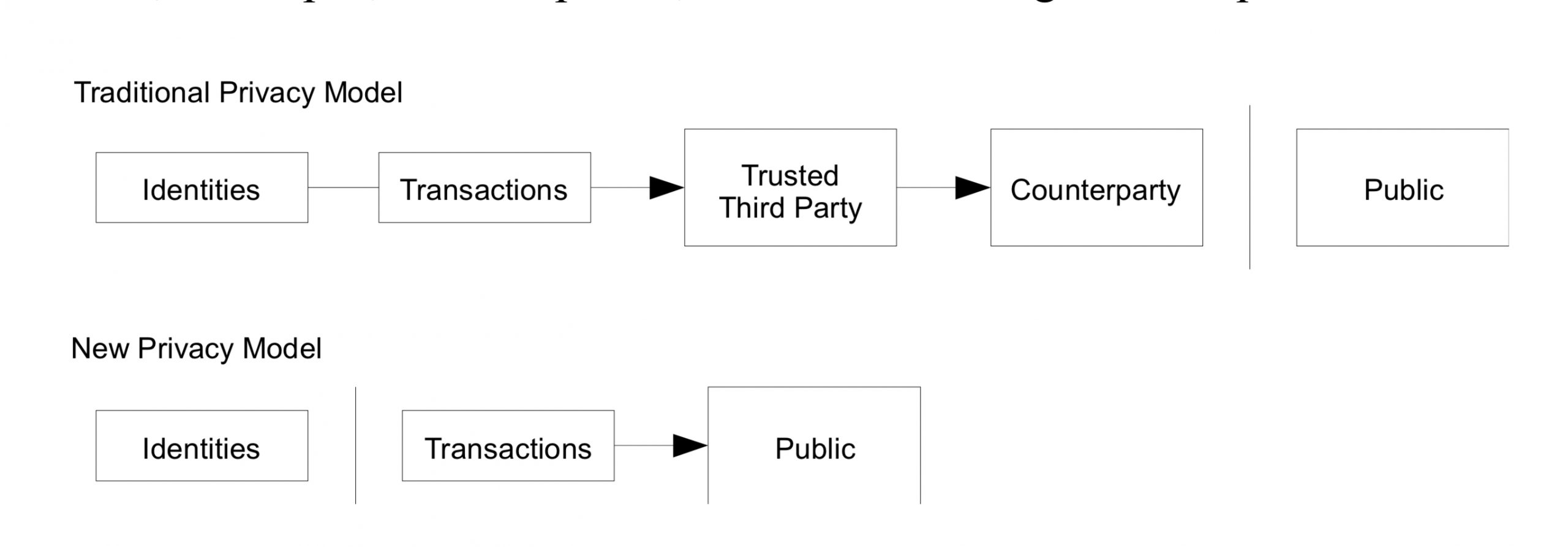

The privacy model for Bitcoin is different from traditional finance. Actually, the Bitcoin whitepaper has a nice diagram for this:

As you can see, in the traditional world of finance, transactions are shielded from public view, but “trusted third parties” know everything. Those trusted parties include banks, credit card companies, and so on.

In the Bitcoin model, the public can see all transactions, but there is no identity that is required to use the network. But in practice, can analysts use heuristics and algorithms to uncover who is behind certain transactions?

In many cases, they can. For example, if you withdraw Bitcoin from an exchange to your own wallet, the exchange knows who you are. If you then send the coins from your wallet to someone else, the second transaction can also be assumed to be from the same person.

There are several methods available if you want to make your Bitcoin transactions more private. One is to first exchange your coins for another coin that offers better privacy features (such as Monero or Bitcoin Cash), and then exchange them back to BTC.

- How are Bitcoins taxed?

Tax law is complicated and varies widely based on jurisdiction. I am not a tax professional and you should always seek professional tax advice when it comes to finances.

That said, it appears taxes on Bitcoin are not particularly different from other assets. When you sell Bitcoins, it is generally a taxable event and taxes are owed on the profits. Unrealized profits are generally not taxed (for example, if you hold coins and don’t sell).

- Where can you spend Bitcoins?

You can spend Bitcoins and other cryptocurrencies anywhere they are accepted. Often, online shops offer more cryptocurrency adoption than retail settings. One great place to find stores that accept crypto is map.bitcoin.com.

Another option is to get a crypto-based debit card. For example, this one from Bitpay. This allows you to load your coins and spend them anywhere debit cards are accepted (which is basically everywhere).

What do you think about the eight beginner questions answered? Let us know what you think about this subject in the comments section below.

Image Credits: Shutterstock, Pixabay, Wiki Commons

Disclaimer: This article is for informational purposes only. It is not a direct offer or solicitation of an offer to buy or sell, or a recommendation or endorsement of any products, services, or companies. Bitcoin.com does not provide investment, tax, legal, or accounting advice. Neither the company nor the author is responsible, directly or indirectly, for any damage or loss caused or alleged to be caused by or in connection with the use of or reliance on any content, goods or services mentioned in this article.