Bitcoin (BTC) price recovered by 27% just three days after testing the $31,000 support and earlier today bull recaptured the $40,000 level.

This quick recovery occurred despite the digital asset facing one of the largest buy-side liquidations in a single day as $1.5 billion was wiped off the books. Interestingly, futures contract traders appear to have returned with an even larger appetite.

After such a large liquidation event, an increased appetite from futures traders is somewhat unexpected but professional investors are skilled at hedging their positions and executing complicated strategies involving options.

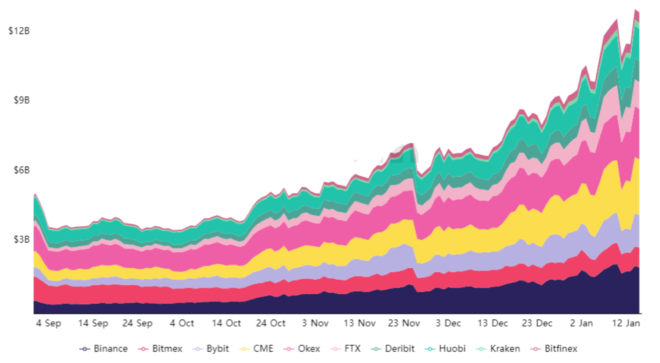

To measure the impact of the recent liquidations and better understand how these futures traders have been positioned, one should start by analyzing the open interest. Large reductions in this indicator could show that traders were caught by surprise and currently unwilling to add positions.

As the above data indicates, BTC futures open interest reached a $13 billion all-time-high on Jan. 14, a 74% increase from the previous month.

For those unfamiliar with futures contracts, buyers and sellers are matched at all times. Every long contract is betting on further upside and has been traded against one or more entities willing to short it.

The futures markets survived the crash test

Bitcoin’s swift recovery from its recent low signals that either traders are risk-takers and hence unaffected by those large price swings, or that most of this activity is composed of hedge and arbitrage trades.

Hedge strategies are used to provide traders with protection. For example, selling futures contracts while simultaneously holding a larger BTC position in a cold wallet. Meanwhile, arbitrage strategies also involve little to no directional exposure, meaning price swings do not impact the trading performance. One could sell longer-term BTC futures contracts while buying the perpetual one, aiming to benefit from eventual price distortions.

The best way to analyze whether directional trades and leverage bets have been dominating the scene is to look at the futures premium and the perpetual futures funding rate.

These indicators tend to oscillate massively during unexpected price swings if leverage trades have been behind the move. On the other hand, those metrics will remain relatively steady if traders have no directional exposure because they are primarily deploying hedge and arbitrage strategies.

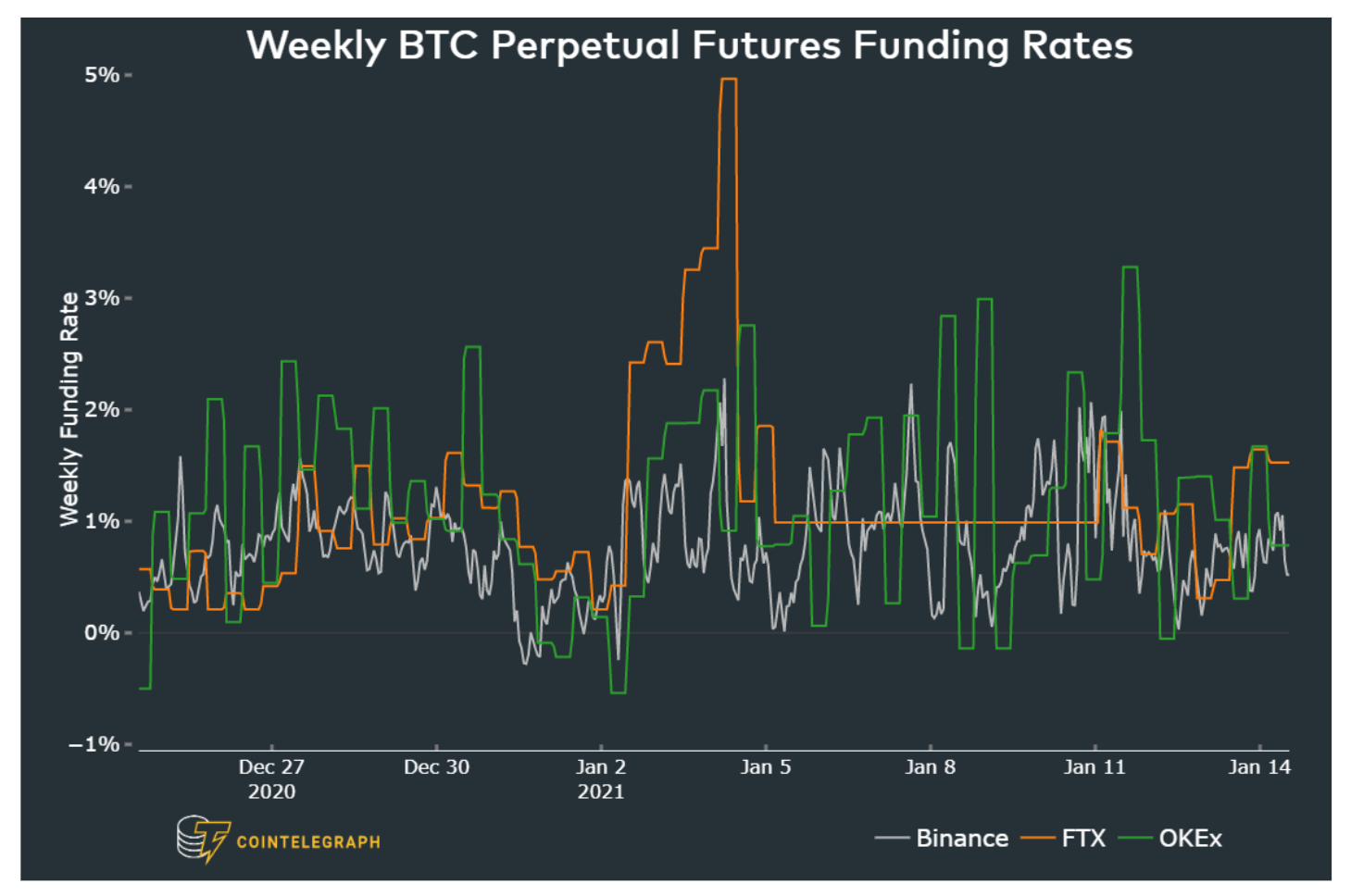

The perpetual futures’ funding rate hardly moved

Perpetual contracts, also known as inverse swaps, have an embedded rate, usually charged every eight hours. When buyers (longs) are the ones demanding more leverage, the funding rate turns positive. Therefore, the buyers will be the ones paying up the fees. This issue holds especially true during bull runs, when there is usually more demand for longs.

As shown above, the funding rate has been ranging from 0% to 2% since Jan. 5, thus indicating that no anomaly took place. Had there been moments of panic among perpetual contract traders, the rate would have shifted to the negative side, as those betting on the downside (shorts) would be paying the fee.

The average 1% weekly funding rate seems exceptionally modest considering Bitcoin’s 74% rally over the past three weeks.

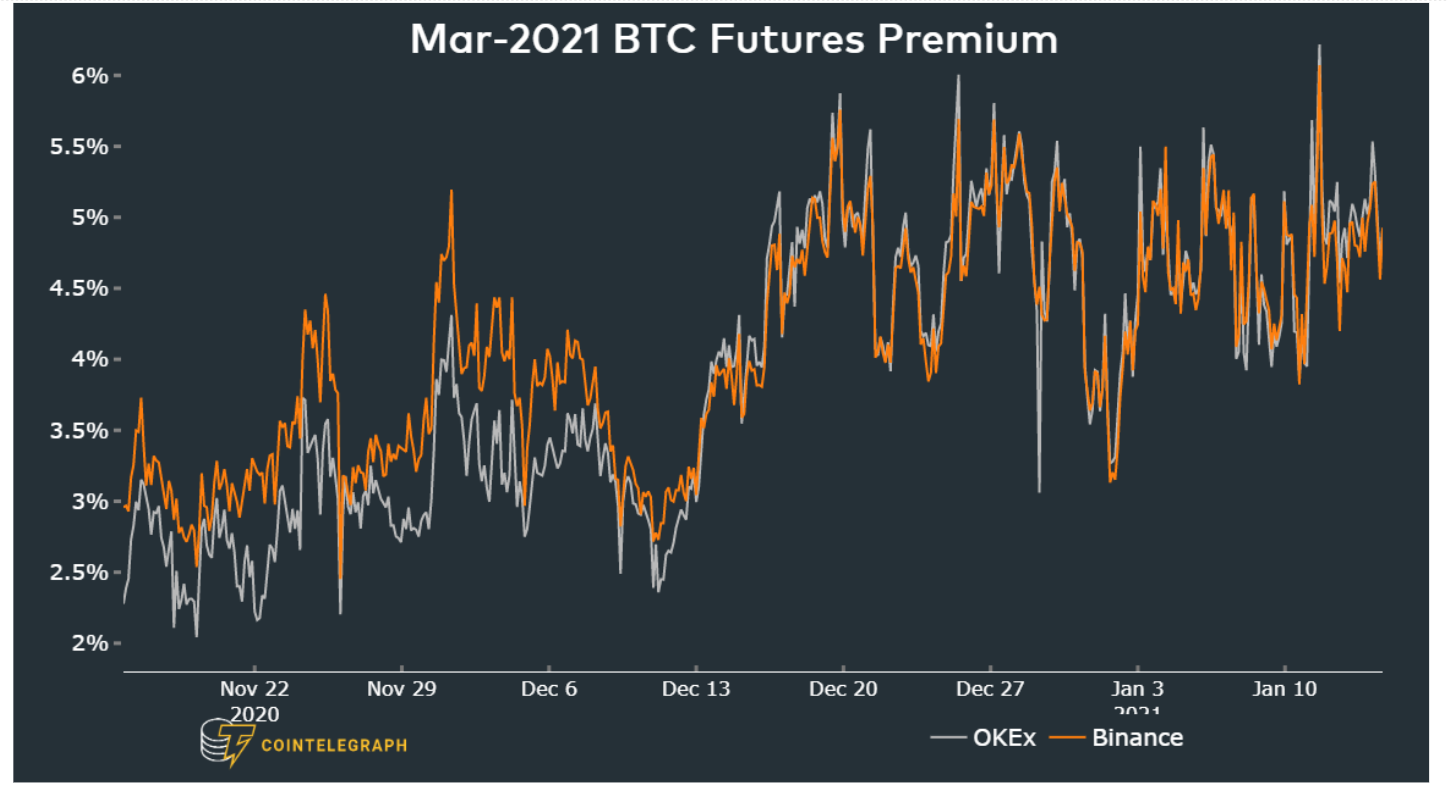

The 3-month BTC futures premium is still high

Professional traders tend to dominate longer-term futures contracts with set expiry dates. Thus, by measuring how much more expensive futures are versus the regular spot market, a trader can gauge how bullish they are.

The 3-month fixed-calendar futures should usually trade with a 2% or higher premium versus regular spot exchanges. This equals an 8% annualized yield, which can also be interpreted as a lending rate, as the seller is postponing settlement.

Whenever this indicator fades or turns negative, this is an alarming red flag. Such a situation, also known as backwardation, indicates that the market is turning bearish.

The above chart shows that the indicator has been holding a 4% minimum. Meanwhile, a 5% rate translates to 21% annualized, which is higher than most decentralized finance applications are returning for stablecoin deposits.

Therefore, the indicator has been flirting with overbought levels, indicating optimism from professional traders. This data is a positive reading, as the recent unexpected swings have not reduced their appetite.

At the moment, it’s clear that the recent volatility has not shaken out derivatives traders. Meanwhile, the growing futures open interest and the 3-month premium indicate that there are no sizable bets on a downturn or lack of confidence in the market.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.