View

- Bitcoin fell 2.87 percent on Tuesday, ending the longest stretch of daily gains since July 2018. The long-term outlook, however, remains bullish with the 3-day chart calling a move to $10,000.

- On the way higher, BTC may face resistance at the key Fibonacci retracement level of $9,642.

- The hourly and 4-hour charts are reporting bearish indicator divergences. As a result, a correction to key support at $8,600 could be seen before a potential rally to $10,000.

Bitcoin’s (BTC) price closed on a negative note on Tuesday, snapping the longest daily winning streak in 11 months.

The leading cryptocurrency by market value fell 2.87 percent yesterday, having scored 2-5 percent gains in each of the preceding six days.

That was the longest stretch of daily price gains since July 2018. Back then, the price had advanced for seven successive days – from July 13 to July 19 – to hit highs above $7,500, as per data source CoinMarketCap.

The latest six-day winning streak saw bitcoin rise from $8,120 to $9,366, possibly due to the hype surrounding Facebook’s foray into cryptocurrencies, Binance.com’s decision to ban US customers and other factors, as discussed on Monday.

On Tuesday, the social media giant officially launched its cryptocurrency Libra to mixed reviews with many experts calling it a net positive development for bitcoin and cryptocurrencies in general.

Even so, BTC suffered moderate losses, possibly because Facebook’s Libra launch was priced in over the weekend.

Looking forward, the long-term outlook remains bullish with technical charts calling a rise to $10,000. However, in the next 24 hours, a correction to key support near $8,700 could be seen.

As of writing, BTC is trading largely unchanged on the day at $9,135, according to CoinMarketCap.

3-day chart

BTC’s previous three-day candle closed above the high of $9,006 hit on May 30, establishing another bullish higher high. It is worth noting that the cryptocurrency has charted a series of higher lows and higher highs since early February.

Further, the 5- and 10-candle moving averages (MAs) continue to trend north, indicating a bullish setup and the widely followed relative strength index (RSI) has maintained the bullish bias with a bounce from the ascending trendline connecting November and January lows.

Therefore, the path of least resistance is on the higher side. On the way toward $10,000, BTC may face stiff resistance at $9,642 – 38.2 percent Fibonacci retracement of the sell-off from $20,078 to $3,193.

The bullish bias would be invalidated if the price finds acceptance below the ascending 10-candle MA, currently at $8,477.

The outlook would turn bearish if the price drops below recent lows below $7,600, violating the bullish higher lows pattern.

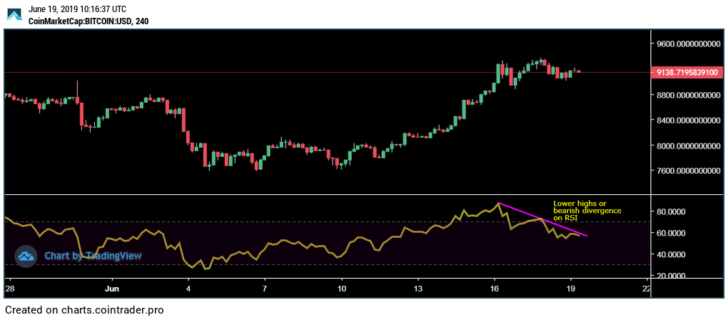

4-hour chart

The RSI has produced lower highs on the 4-hour chart over the last five days, contradicting the higher highs on price. That bearish divergence indicates scope for a price pullback.

The bearish RSI divergence would be invalidated if the indicator cuts through the descending trendline hurdle, currently at 60.

1-hour chart

As seen above, the price is stuck between the 50-hour and 100-hour MAs.

The cryptocurrency bounced up from the 100-hour MA in Asian trading hours. So far, however, the 50-hour MA hurdle, currently at $9,198, has proved a tough nut to crack.

A break below the overnight low of $9,005 would confirm bearish lower highs and lower lows pattern and allow a deeper drop to $8,600 – support of the trendline connecting June 10 and June 11 lows.

Disclosure: The author holds no cryptocurrency at the time of writing

Bitcoin image via Shutterstock; charts by TradingView