This week the U.K.’s Financial Conduct Authority (FCA), which regulates the country’s financial services, issued a ban on the sale of crypto derivatives and ETNs to retail investors.

While this may not seem particularly material to crypto asset markets overall – U.K. retail investors weren’t that much into crypto derivatives anyway, and the market hardly reacted at all – it is worth paying attention to for the alarming message contained within.

This message loudly says: “We don’t like crypto assets.”

In case you think I’m exaggerating, the policy statement opens with the sentence: “There is growing evidence that cryptoassets are causing harm to consumers and markets.” (Actually, there isn’t, and to see a financial regulator make such a bold claim with no supporting evidence is jarring.)

The message itself is fine; not everyone likes crypto assets. But this is a financial regulator whose job includes protecting investors, not passing judgement on new asset groups. The documents accompanying the ban read like a reflection of the personal opinions of some senior members, and represent a gross overstep of the regulator’s mission and remit.

Ironically, this is exactly the type of unreasonable centralized control that crypto assets were created to circumvent.

Too difficult

A secondary message, also alarming, says the FCA thinks retail investors are incapable of understanding new topics.

The reasoning is couched in a “for your own good” tone – the FCA assures investors it is preventing losses of between £19 million and £101 million a year. This in itself insults retail investors’ intelligence, as whatever method they used to calculate this figure produced too wide a band to be even remotely credible. I wonder how much the same retail consumers lose on the National Lottery every year.

Let’s take a look at the five main reasons for the ban, according to the FCA bulletin.

1) First up is the “inherent nature of the underlying assets, which means they have no reliable basis for valuation.” Seriously, show me something that does in these markets. OK, that might be a slight exaggeration, but the idea that market prices respond to fair valuations went out the window months ago.

Plus, crypto assets are a new type of asset. They don’t respond to traditional valuation methods, but this does not mean they don’t have any value drivers. Plenty of work is being done to deepen and spread understanding of what these are.

2) Second, we have the “prevalence of market abuse and financial crime in the secondary market (eg cyber theft).” You may recall that, at the end of September, leaked documents known as the FinCEN Files showed that the U.S. Treasury has labelled the U.K. a “higher risk jurisdiction,” because of the relatively high incidence of financial crime that has nothing to do with crypto derivatives.

3) The cited “extreme volatility in crypto asset price movements” is also an unjustified excuse. Crypto assets are volatile, but bitcoin’s volatility has been heading down over the years, and is not as volatile as some equities on which investors can buy derivatives. Yet you don’t see U.K. retail investors being banned from buying or selling Tesla derivatives.

4) Throughout the statement, the FCA refers often to the “inadequate understanding of crypto assets by retail consumers.” This is just plain condescending. How do they know the understanding is inadequate? This assumption is tantamount to assuming retail investors are incapable of doing their own research and understanding the material. I’m certain there are many retail investors who understand crypto assets better than the FCA does.

What’s more, FCA consumer survey results released in July of this year found that “the majority of crypto asset owners are generally knowledgeable about the product, are aware of the lack of regulatory protection afforded and understand the risk of price volatility.” The FCA’s own research shows that retail crypto investors have done their homework. Deciding that homework is “inadequate” seems an inappropriate step for a financial regulator to make, especially when no justification is offered.

5) And finally, perhaps my favorite one, we have the “lack of legitimate investment need for retail consumers to invest in these products.” Is it the FCA’s job to determine what the market needs? Does the market really need more equity ETFs? Many well-known investors, with long track records of respectability and rigor, have argued that crypto assets do fulfill a need for a hedge against inflation and financial turmoil.

Too easy

As if more evidence was needed that this is not about a lack of disclosure or oversight and more about dampening interest in a new asset type, the ban includes Exchange Traded Notes (ETNs). This is likely to have a greater impact than the derivatives ban, as ETNs are a meaningful onramp into the crypto markets for retail investors. It is also more perplexing, as ETNs are much less risky than derivatives.

The risk profile is irrelevant, however. The FCA acknowledges that ETNs are sold with an information-packed prospectus, but even that “will not allow retail consumers to value crypto ETNs reliably.”

The FCA also acknowledges that ETNs trade on regulated exchanges. However, “retail consumers are still unable reliably to predict potential price impacts caused by issues in the underlying crypto asset markets” (as if it were easier in stock markets). This means, you guessed it, that they “cannot value them or the ETN reliably.”

And, ETNs are not leveraged. But that doesn’t matter, what is important is investors’ ability to value things correctly.

Within bounds

You’re probably wondering why the ban didn’t extend to crypto assets themselves, when it’s obviously the assets that are the problem, not the packaging.

The answer might lie in the same consumer survey mentioned above, which showed that 83% of U.K. residents that had purchased cryptocurrencies had done so through non-U.K. based exchanges. Perhaps the FCA realizes that an outright ban would be futile? Or perhaps the very same companies that finance the FCA (members of the U.K.’s financial services industry) have applied some pressure to save what could be profitable revenue streams in the future?

In banning derivatives, though, the FCA is failing in one of its principal remits. Making it harder for small investors to hedge their positions, and/or pushing investors to less regulated offshore platforms, does not sound like consumer protection. And removing the relatively safe onramps of ETNs from the range of crypto instruments available means that retail investors have to handle their own, possibly less secure, custody arrangements.

The ban is also hurting the crypto industry. Derivatives are an essential component of efficient markets. They help with price discovery by allowing expression of a variety of opinions, and they encourage liquidity by offering downside protection. Crypto derivatives are still available to institutional clients who dominate the markets, so the immediate impact is likely to be minimal. But measures like this exacerbate inequality, concentrating return opportunities in the hands of those that have financial power. Markets should not just be for the institutions.

Note that the ban extends to self-certified sophisticated investors and high-net worth individuals, on the grounds that these investors stand to lose even more. The FCA has decided that these experienced and/or wealthy individuals do not have the right to use their own money to take on financial risk of their choosing.

Doing the work

Now, fair, crypto assets are tricky to value. Many theories abound, yet no one “knows” how to do it. We have here a young market with totally different fundamental drivers, running on a technology that spins off totally different data sets that analysts across the industry are digging into.

This is one of the reasons we started our series of reports and webinars on crypto asset fundamentals, with a view to furthering the conversation about how to value crypto assets. It is also one of the most exciting aspects of our industry: the opportunity to “discover” uncharted (pun) territory in asset research, to set the bases for continuing exploration and to develop a new discipline in financial analysis.

As our knowledge evolves, valuation models will emerge, with additional insight provided by granular data unavailable to investors in traditional assets. Crypto assets will eventually be seen as a much more transparent and information-rich type of investment than stocks, say. One day we will look back and marvel at how we trusted information provided by issuing companies themselves, audited by contracted service providers, sold on platforms with hidden or hard-to-understand fees. And the emergence of crypto assets and their unusual data sets is likely to have the biggest influence on investment valuations since Graham and Dodd unleashed their security analysis framework in 1934.

Investors’ inability to fairly value crypto assets is not the problem. The FCA’s lack of foresight is.

Anyone know what’s going on yet?

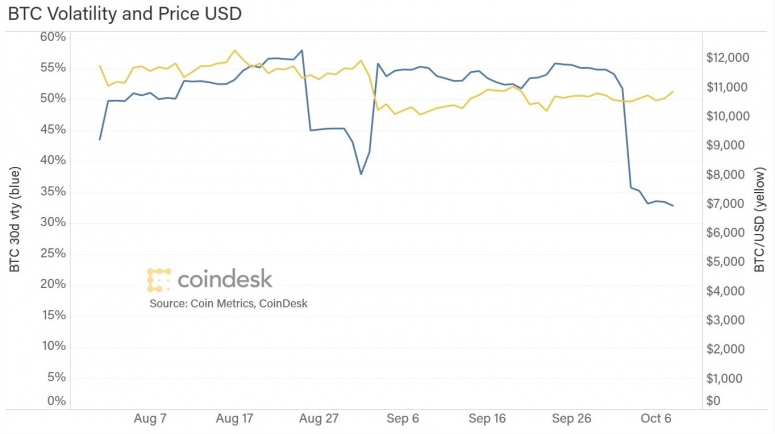

On Friday, bitcoin broke through $11,000 for the first time since mid-September, after a week languishing around $10,600.

This could partly reflect the weaker dollar toward the end of the week and the return of optimism to equity markets. It could also be as a result of the news that payments processor Square has purchased close to $50 million worth of BTC for its treasury – the purchase already happened, but the market seems to expect other corporations to follow suit.

Furthermore, it feels significant that the BTC price weathered several blows during the past two weeks (such as the criminal charges brought against derivatives exchange BitMEX, a notable hack on crypto exchange KuCoin and the disruption of stimulus talks in the U.S.) without notable declines.

Indeed, in spite of significant market news, bitcoin’s 30d annualized volatility dropped to levels not seen since the doldrums of the summer.

CHAIN LINKS

Payments company Square, led by Twitter CEO Jack Dorsey, has joined the ranks of companies putting part of treasury holdings into bitcoin. This week it revealed that it has purchased 4,709 bitcoins, a $50 million investment representing 1% of the firm’s total assets. TAKEAWAY: Square has done more than put part of its treasury into bitcoin. It has also written a how-to for other firms considering doing the same. This could end up doing even more as encouragement than the publicity around the investment, as I suspect that the idea of placing corporate funds on totally different rails, using unfamiliar intermediaries and confusing custody arrangements, must be terrifying for corporate treasurers. Square even explains how the holding will be accounted for on the balance sheet, detail I haven’t seen anywhere else.

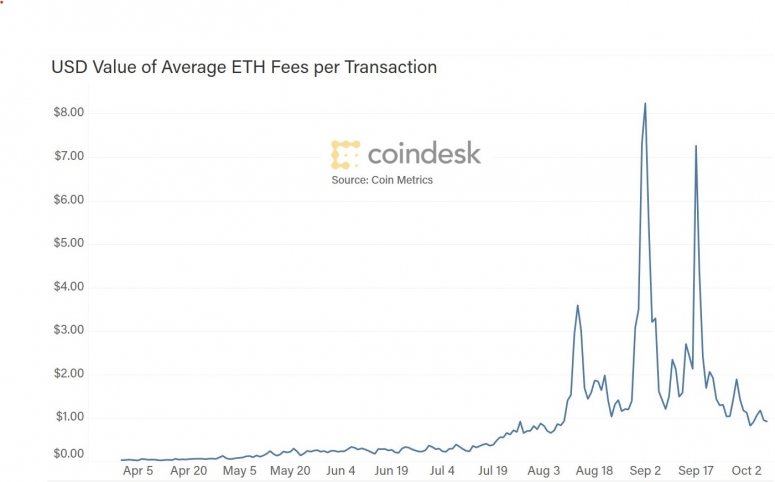

Tumbling prices for many decentralized finance tokens have eased congestion on the Ethereum blockchain, bringing fees back down to August levels. TAKEAWAY: The problem has not gone away, however – fees are still well above the levels seen in the first half of the year, and may still exert a dampening influence on network growth.

(NOTE: To learn more about the role fees play in the Ethereum ecosystem development, join us for a day-long virtual event focused on Ethereum and its upcoming update.)

The Chicago Mercantile Exchange (CME), the largest U.S. regulated market for bitcoin futures, has been sounding out cryptocurrency traders to gauge their interest in a listing of ether (ETH) futures and options. TAKEAWAY: Last year, the Chairman of the U.S. Commodity Futures Trading Commision (CFTC), Heath Tarbert, said on stage at a CryptoX event that he expected to see ether futures in 2020. At the time, I expressed skepticism, mainly because of the uncertainty surrounding the upcoming Ethereum 2.0 launch. I will be happy to be proven wrong, however, as ETH futures on a regulated derivatives platform will give institutional investors more choices in framing their investment theses.

Filings for the first half of this year show Charles Schwab Investment Management Inc. and two Vanguard funds purchased shares in crypto mining company Riot Blockchain. A handful of Fidelity funds invested in Riot, bitcoin mining services provider HIVE, mining company Hut 8 and Hong Kong-based digital asset platform BC Group. TAKEAWAY: This hints at a growing interest in listed companies with exposure to crypto asset markets, which can be held in a wider range of regulated funds than a direct crypto asset holding can. For deeper insight into some of these companies, check out our recent crypto industry company reports.

Ria Bhutoria of Fidelity Digital Assets explains the role of prime brokers in crypto asset markets – as with everything crypto, it’s different from the traditional counterpart.

Investor Lyn Alden takes an analytical look at bitcoin correlations, and how the bitcoin price fares in times of positive vs. negative real yields, and the impact of stimulus package talks. Worth a read.