When Bitcoin’s (BTC) price dropped 10% to $29,150 on Jan. 27, something unusual happened with the Chicago Mercantile Exchange (CME) BTC futures contracts.

As the price fell, these CME Bitcoin futures traded at a 1% discount to Coinbase, which signaled a disarrangement between both markets.

Good morning.

Bitcoin spot has almost full retraced the weekly.

CME bitcoin futs are both backwardian and expire Friday. That is all.

Immediately, traders suggested that futures contracts, which were set to expire in 48-hours, were responsible for the price dump. Now, before rushing to quick conclusions, one should note that every short sale needs a buyer (long) of the same size.

Thus, there can not be an open interest imbalance. Moreover, futures contracts can be extended (rolled over) for a future date, as long as its holder has enough margin to cover it.

Instead of assuming that one singular factor impacted Bitcoin’s price, it’s better to analyze the intraday movements of both markets (CME futures and spot exchanges).

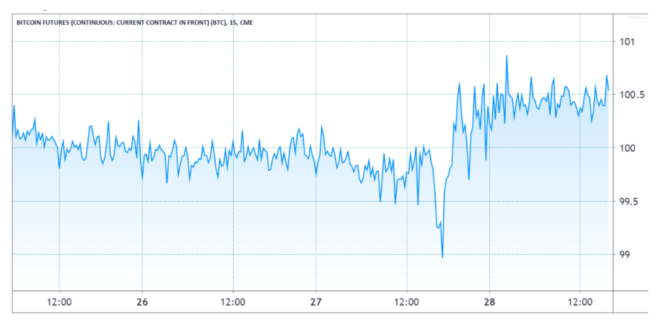

The futures premium (or basis) measures the premium of longer-term futures contracts to the current spot (regular markets) levels. Whenever this indicator fades or turns negative, this is an alarming red flag. This situation is also known as backwardation and indicates bearish sentiment.

CME futures premium. Source: TradingView

These fixed-month contracts usually trade at a slight premium, indicating that sellers request more money to withhold settlement longer. On healthy markets, futures should trade at a 5% to 15% annualized premium, otherwise known as contango.

The unalignment between each market could have been caused by long contracts liquidations driven by traders with insufficient margin, thin order books, or an intense price action ahead of the remaining spot markets.

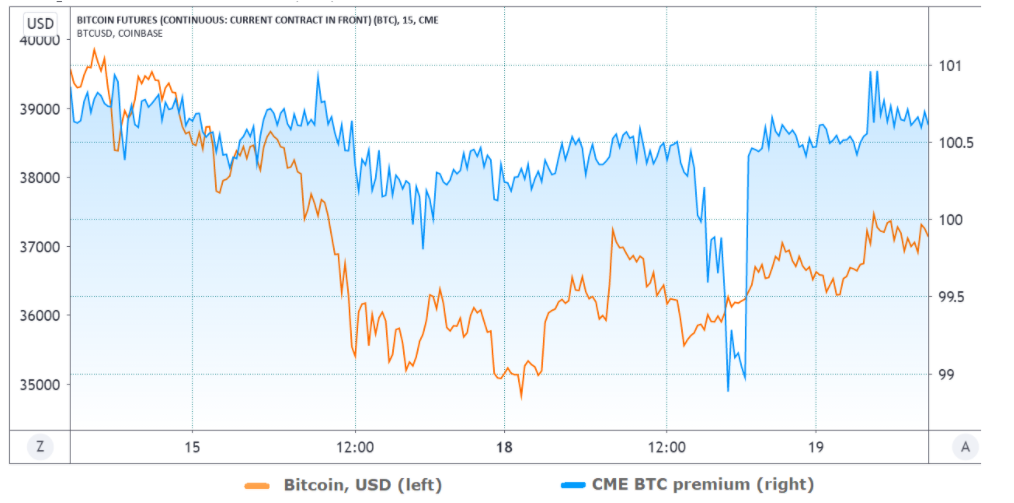

Therefore, this data by itself does not uncover a cause or a consequence. Furthermore, a similar movement took place on Jan. 18.

CME futures premium vs. Coinbase BTC USD. Source: TradingView

Take notice of how the CME BTC premium collapsed to a negative 1% despite no apparent volatility taking place on the BTC spot exchanges. It is safe to say that this event held zero relation to the market’s price action.

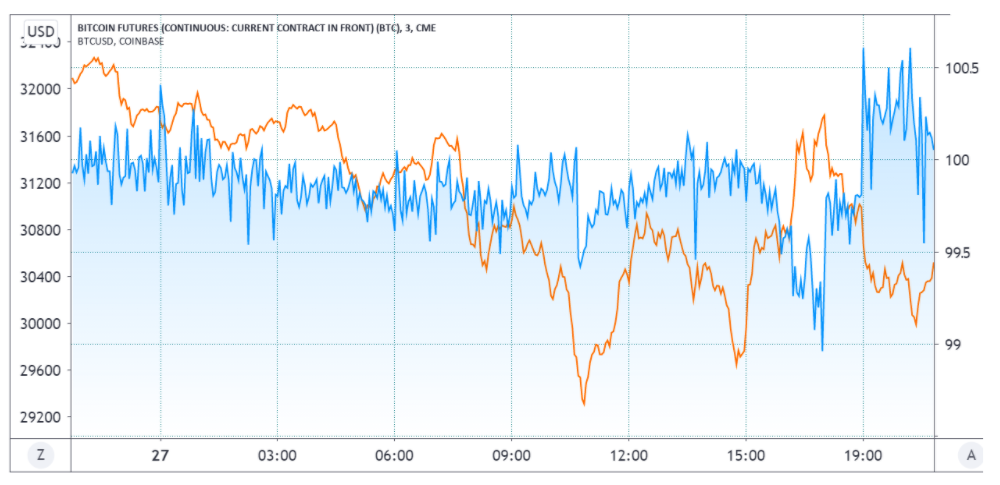

By analyzing the Jan. 27 crash on a more granular view, it is possible to determine whether the negative CME premium preceded the market volatility.

CME futures premium vs. Coinbase BTC USD. Source: TradingView

The above data levels show that instead of acting as a leading indicator, the CME Bitcoin futures premium plunged much later in the day. As Bitcoin tested the $31,800 resistance, the sell pressure at CME continued, causing the momentarily price difference.

Multiple reasons could be behind this effect, so comparing the intraday price on multiple exchanges might explain if CME led the downturn.

To summarize, there is no evidence of any price anticipation by the CME Bitcoin futures. These markets are incredibly arbitrated and will typically move in tandem. Moreover, the usual premium might face some momentary discrepancies similar to those that occurred on Jan. 18, regardless of Bitcoin’s volatility at the time.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.