With a key metric declining to record lows, bitcoin’s options market may be underpricing cryptocurrency’s future volatility. Analysts say the data is being distorted by “Black Thursday’s” 40% drop.

The spread between bitcoin’s three-month implied volatility (IV) and historical or realized volatility (RV) fell to -47% on Wednesday, the lowest since the crypto derivatives research firm Skew began tracking the data 18 months ago.

The spread turned negative in March and has continued to drop ever since. “Historically, RV has been lower than IV for bitcoin over the last 18 months, except for a short period in the months around September 2019,” noted analytics resource Arcane Research in its monthly report.

What the IV-RV spread usually signifies

Implied volatility is the market’s expectation of how risky or volatile an asset will be in the future. It is computed by taking an option and the underlying asset’s price along with other inputs such as time to expiration. Realized, or historical, volatility is the standard deviation from the average price of the underlying asset. It measures volatility actually realized in the past.

Volatility has a positive impact on options price. Higher volatility (uncertainty) leads to stronger hedging demand and a higher price for both call (bullish bet) and put options (bearish bet).

Bitcoin’s three-month implied volatility is hovering near its lifetime average of 4.2%, a sign options appear to be fairly valued.

Traders often expect volatility to be mean reverting, meaning it typically rises after it gets too low and falls after it gets too high, in the process influencing options prices. As a result, seasoned traders keep track of changes in the IV-RV spread, the differential between implied volatility and its lifetime average.

Options prices are considered to be cheap if the IV-RV spread suggests the implied volatility is too low compared to the realized volatility or the average implied volatility. Alternatively, options are considered to be overvalued if the implied volatility is too high compared to its lifetime average or historical volatility.

Put simply, options traders buy calls or puts when implied volatility is too low, the logic being that IV will rise back toward its mean, making options dearer. Meanwhile, traders sell options when implied volatility is too high on hope that IV will fall back toward its mean, making options cheaper.

The March 12 effect

Investors may read the recent drop in bitcoin’s three-month IV-RV spread as a sign the expected volatility is too low and options prices are very cheap compared to historical standards.

However, that is not necessarily the case because the three-month realized volatility is distorted and being held high by bitcoin’s 40% drop registered on March 12.

“The three-month realized volatility still includes that 12th of March point where bitcoin sold off around 40% in a single day,” said Skew’ CEO Emmanuel Goh, while adding that after mid-June the realized volatility would fall as the March 12 data point will be excluded from calculations.

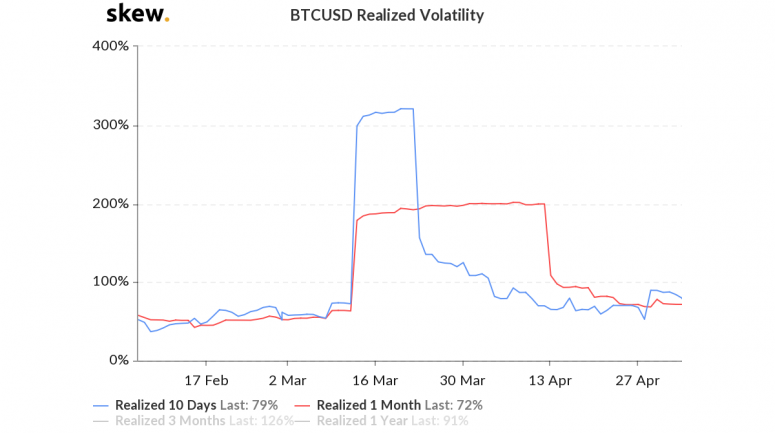

Validating Goh’s argument is the fact that short-duration realized volatility metrics have come down sharply from March’s lofty heights.

The 10-day realized volatility is seen at 80% at press time, down significantly from the high of 321% registered on March 21. Meanwhile, one-month RV stands at 72%, having topped out at 200% on April 21.

Options look fairly valued

Bitcoin’s three-month implied volatility is hovering near its lifetime average of 4.2% at press time, a sign options appear to be fairly valued.

However, both volatility (uncertainty) and option prices are likely to rise as we head closer to next Tuesday’s mining reward halving. The programmed code will reduce rewards per block mined to 6.25 BTC from 12.25 BTC.

While most analysts have hailed the supply-altering event as positive for bitcoin’s price, historical data indicates scope for a short-term pullback.

Uncertainty tends to rise ahead of such binary events, boosting demand for option prices.

Disclosure Read More

The leader in blockchain news, CryptoX is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CryptoX is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.