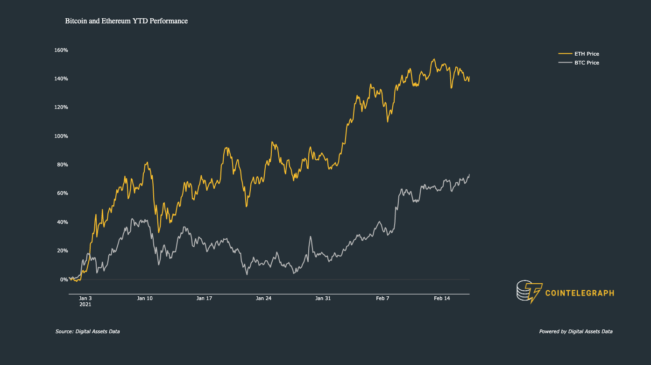

Ether (ETH) is up 150% in 2021, causing its market capitalization to soar above $200 billion. Most traders are fixated on the unitary price, even though it is entirely arbitrary, therefore missing relevant milestones and comparables.

Investors, mainly those coming from the traditional industry, are used to compare multiples of earnings, sales, and market share. Meanwhile, when valuing a cryptocurrency with multiple use cases, there is no single metric to gauge its potential. Ether might simultaneously act as a digital store of value while functioning as the token required to access the Ethereum network.

To evidentiate the myopia caused by unitary prices, Cardano (ADA) is priced below $1, although its market capitalization is over $26 billion. Therefore, the outstanding number of coins matters just as much. At the other extreme, Cover Protocol (COVER) unitary price is nearly USD 1,600, even though its market capitalization remains sub $100 million.

Although the merits of comparing different classes’ assets side-by-side are debatable, market capitalization works the same way for commodities, stocks and mutual funds. Some additional metrics are often used to analyze an asset size, including free float, the quantity effectively available for trading, besides the average trading volume.

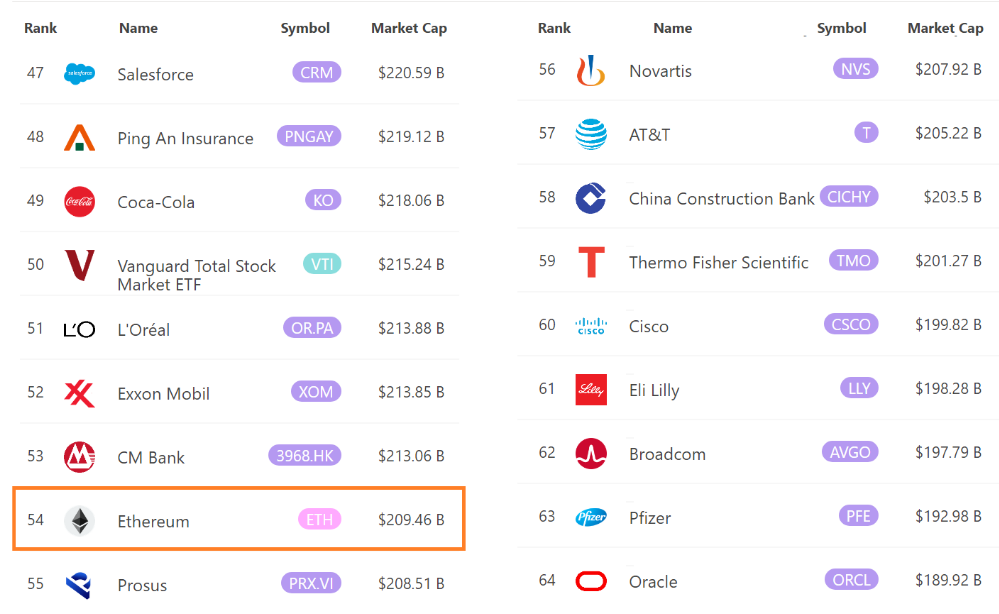

According to 8marketcap.com, Ether’s market capitalization has recently surpassed those of Novartis ($NVS), AT&T ($T), and Cisco ($CSCO). Thus, it is only fair to make general comparisons with those companies as investors might opt for one or another.

The Swiss-based Novartis International AG had its origins in 1857. With over 110,000 employees, the drugmaker posted an $8.1 billion net income in 2020. Therefore, comparing a 165-year company heavily dependent on research, production, and distribution with a technology-based protocol that doesn’t even have servers or development teams seems absurd.

Moreover, companies run risks of additional shares being created, as opposed to Ether’s fixed-supply calendar. Similar issues emerge on taxes, liabilities and potential government control. Decentralized protocols, however, are more insulated from such risks, thus justifying a much higher valuation.

Cisco Systems was ordered to pay $1.9 billion in a patent infringement lawsuit in Oct. 2020. In Jan. 2021, AT&T was sued for at least $1.35 billion by a Seattle company. There are endless ways a shareholder might be caught by surprise as one is heavily dependent on third parties.

To conclude, while it makes sense to compare various assets’ market capitalizations, cryptocurrencies’ purely technological nature provides a much broader upside.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.