Bitcoin was flat to slightly lower after briefly climbing Wednesday above $18,000 for the first time since December 2017.

“There is a tsunami of buying power up against reluctant sellers,” Charlie Morris, CEO of the cryptocurrency fund manager ByteTree, wrote in a note to clients. “These buyers are putting real money behind Bitcoin, not the old dribs and drabs normally seen from retail investors.”

In traditional markets, European shares fell and U.S. stock futures pointed to a lower open amid concerns over new coronavirus-related restrictions and lockdowns. Gold weakened 0.5% to $1,863 an ounce.

Market Moves

Bitcoin’s breathtaking rally for the past couple of months has been attributed to all sorts of grand macroeconomic reasons, from the need for a safe haven as the pandemic ravages the global economy once more to marvelous projections about the future role of the cryptocurrency in finance.

Yet what if the recent run-up was merely the result of miners in China having a hard time finding a place to sell their inventory for the kind of hard cash that they need to pay the bills? In other words, fewer new bitcoin may be hitting the market and that’s what’s driving prices higher. That’s an explanation explored in Omkar Godbole’s article on CoinDesk Wednesday.

According to recent note from QCP Capital on its Telegram channel, miners in China are seeing their bank accounts and credit cards frozen as the government tries to crack down on money laundering. That’s a big deal for bitcoin because 70% of its mining power comes from China.

In the process, the government’s squeeze is also affecting a lot of cryptocurrency exchanges catering to Chinese customers, most notably OKEx and Huobi; some questions have been raised about what happened to a couple of executives at such firms, as CoinDesk’s Muyao Shen reported last week. OKEx suspended withdrawals on Oct. 16 when founder Mingxing “Star” Xu was rumored to have been taken into police custody. It announced Thursday that it “will be resuming withdrawals on or before November 27” as Xu is now said to be a free man again.

Over the summer, OTC traders in China also felt the heat, and they had a hard time getting access to cash as well.

For all the talk about how bitcoin is the future staring us right in the face with no social distance or mask, utilities companies, landlords and maintenance employees still need to be paid in fiat. Their bills aren’t denominated in satoshis but in yuan. Thus, there’s always a need for miners to trade into local currency and get on with whatever they do in their lives since many public service providers in China don’t exactly accept tether. According to QCP Capital, a survey done by Colin Wu showed that 74% of miners claim they have trouble selling their inventory to cover operating expenses.

To be sure, Wu’s survey may not have been conducted with the most rigid of standards. And the calendar still insists that this year is 2020. And if there’s one thing this year has taught the world it’s that surveys should be taken with a great of salt. Nonetheless, it’s a data point.

Bitcoin’s gains since the start of October have been nothing short of phenomenal. Its price is up about 65% since the start of last month. And over the past few weeks, some of China’s biggest exchanges started seeing accounts frozen and executives all of a sudden, er, out of the office at the moment.

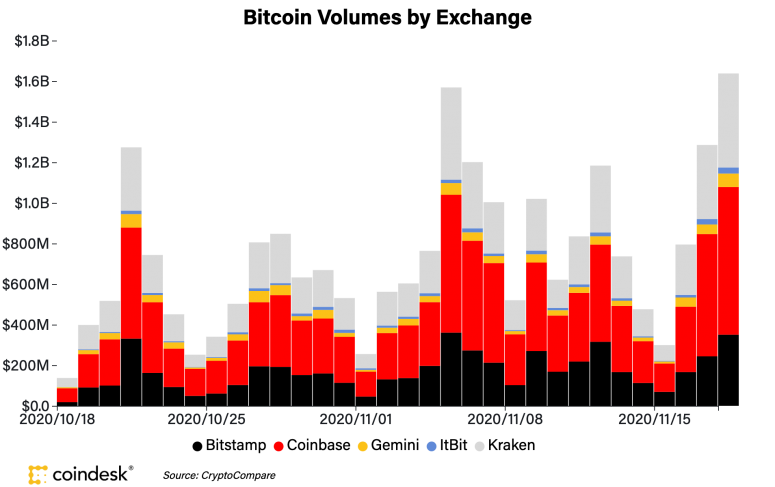

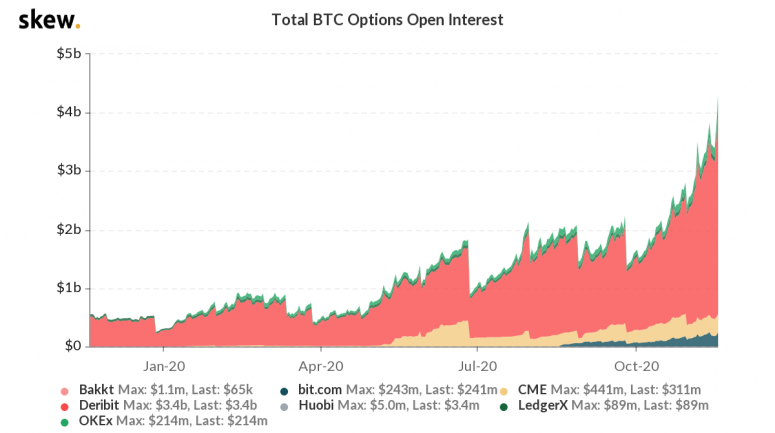

Meanwhile, volume on bitcoin has been healthy, with $1.6 billion traded Wednesday on some of the major exchanges, as CoinDesk’s Daniel Cawrey reported. Open interest in bitcoin options have shot up to a record high of over $4 billion, double what it was in mid-October. What’s more, positions in the options market are as bullish as they have ever been.

About 900 bitcoin are mined every day. At current prices, that’s worth just $16 million. However, in a month, it adds up to nearly $500 million and the lion’s share of that is from China.

This is an interesting case where the supply curve may be shifting inward just as the demand curve is shifting outward. Either one of those would, all things being equal, raise prices. And while we may now be witnessing both, it’s good to remember that a sudden return to the previous condition for either one of those curves could drop prices as fast as it raised them.

Bitcoin Watch

Bitcoin is taking a breather, having chalked out a steep rally to three-year highs above $18,000 in the past six weeks.

At press time, bitcoin is trading near $17,700, having faced rejection above $18,000 multiple times in the past 24 hours. Some investors are beginning to position for a deeper pullback with the cryptocurrency struggling to establish a foothold above $18,000.

The one-month implied volatility, which is mainly determined by the demand for call and put options, jumped from roughly 55% to a four-month high of 70.5% in the past two days, suggesting increased expectations for price turbulence over the next four weeks.

Alongside that, the spread between the cost of puts or bearish bets and calls eased, as evidenced by the recovery in the one-, three-, and six-month put-call skews. Notably, the one-month gauge bounced from -27% to 14%, according to data source Skew.

The numbers indicate increased demand for put options – a sign of investors hedging against a potential price pullback.

What’s Hot

- JPMorgan Chase CEO Jamie Dimon said blockchain will have a pivotal role in the future of finance even if bitcoin, the No.1 cryptocurrency by market capitalization that made blockchain famous, is not his “cup of tea.” (CoinDesk)

- Bitcoin’s price surge may be driven as much by a drying up in supply as by an increase in demand. That’s because Chinese miners are struggling to sell their crypto in ways that would quickly get them much-needed cash in the face of a government crackdown on local exchanges. (CoinDesk)

- Ethereum Classic Labs, the Ethereum Classic blockchain’s biggest supporter, released Wrapped ETC, which allows ethereum classic holders to participate in the decentralized finance (DeFi) space which is based on the Ethereum blockchain, the chain that Ethereum Classic split from after a contentious hard fork in 2016. (CoinDesk)

- OKB, the native token for leading crypto derivatives exchange OKEx, rallied more than 13% Wednesday on rumors that the firm’s founder, Mingxing “Star” Xu, had been released from police custody in China. (CoinDesk)

- Netherlands-based cryptocurrency exchange Bitonic says it has been “forced” to bring in extra verification measures due to requirements from the country’s central bank. (CoinDesk)

Analogs

The latest on the economy and traditional finance

- Dollar up on COVID-19 case rise, gains curbed by Fed easing expectations (Reuters) The dollar strengthened on Thursday as broad optimism about COVID-19 vaccines ran into worries about rising infection numbers and risks to the fragile global economic recovery.

- Stock Futures Slide Amid Fresh Lockdowns (WSJ) Weekly jobless claims data and existing-home sales numbers will offer fresh cues on the pace of economic recovery as Covid-19 cases rise.

- Treasury yields slump amid state coronavirus restrictions (CNBC) A handful of states and cities in the U.S. are closing nonessential businesses, limiting public and private gatherings and imposing mask mandates.

- Dollar Loses to Euro as Payment Currency for First Time in Years (Bloomberg) The euro was the most used currency for global payments last month, the first time it has outpaced the dollar since February 2013.

Tweet of the Day