Short-sellers, who make money when the price of a targeted financial instrument declines, aren’t always popular with corporate or government leaders. Those on the receiving end of contrarian bets against stocks or currencies tend to portray them as sharks undermining people striving to build, grow and create value.

This, if you’ll excuse the pun, is short-sighted.

Short-selling is a necessary part of any functioning, efficient financial system. It provides liquidity, ensuring there’s a seller on the other side of each bid. And when viewed in totality, those occasions where the short-seller ends up winning offer invaluable signals on how society should better allocate resources.

I say this because at a time when its price is again soaring, bitcoin should essentially be viewed as a massive short position against the entire financial system. (Even bigger than the “The Big Short.”)

Bitcoin is more than a hedge against inflation. Indeed, amid an extended period of historically low rates of increase in the consumer price index, there’s currently no clear correlation between bitcoin’s rising price and mainstream measures of inflation.

Rather, bitcoin’s core value lies in its decentralized governance design being divorced from the political system, a feature no other asset of its size and liquidity can claim, perhaps with the exception of gold.

Its positioning against inflation is an outcome of that, not its essence. If people lose confidence in their government’s capacity to sustain the trusted, social covenant on which fiat money is founded, the value of that money collapses, resulting in hyperinflation. Because of its depoliticized status, bitcoin gains in value in that environment.

So if you’re long bitcoin, you are positioned to benefit if the system of governance on which the entire world depends for security and well-being collapses. Still feel good about it?

I’m here to tell you it’s OK. Just as short-sellers of stocks have not destroyed the stock market, neither will bitcoin investors bring down that system.

Instead, what they’ll do, I hope, is pressure policymakers to reform the system in ways that better serve their constituents and sustain the social covenant of money.

Reading the signals

I don’t know about you, I like thinking the success of a long-bitcoin bet can lie in driving a constructive improvement in the incumbent system rather than destroying it entirely. After too many episodes of “The Walking Dead,” I can say with assurance that dystopia is not for me.

But let’s be clear: Bitcoin’s nice fat gains do reflect people’s rising fear that our century-old governance model for the global financial system is failing.

There are reasons: unsustainable debt levels; anemic growth despite masses of quantitative easing; economic inequality; the COVID-19 shock; and how, in a decentralized, social media information system where truth is being questioned, people sense a loss of agency in their and their communities’ lives.

Part of the problem is that elite conversations around the solutions are mired in the assumption the old system of government will continue as is. This feeds an expectation of failure, which bit by bit leads more and more people to believe that, even if they’re not “all in” on a bet against that system, they should hold some bitcoin in case the worst arises.

With all of that just-in-case hedging activity, the global short position grows and bitcoin’s price rises.

We need policymakers to recognize what those market signals are telling them: that the existing model is both failing and fragile. Currently, they do not. Let’s hope they get it soon because we all should care that the solution is not violent, destructive revolution but constructive evolution.

A new reserve asset

This is not an anti-establishment argument. It’s most definitely not an endorsement of the nihilistic ethos of Trumpism.

It’s a call to recognize that bailouts (socialized corporate losses) and monetary stimulus (put options for stock market speculators) have papered over deep problems in the economy and done little to raise the happiness of the world’s citizenry. It’s saying we need a new approach to secure an effective market economy, one that empowers everybody to seize opportunities on a level playing field.

And if we achieve that, if the national government-run system evolves to a point where it regains popular support, what role does bitcoin play in that modified system? What is its larger purpose beyond being a hedge against systemic meltdown? It’s hard to see where the sustained value would lie in an asset whose only purpose is to hedge against that worst-case outcome if that outcome doesn’t eventuate.

I think bitcoin’s purpose lies in it becoming a kind of societal reserve asset.

This is a concept beyond both the ideas of a government-held reserve currency and of gold’s long-running status as a citizens’ hedge against monetary meltdown. The early elements of it can be seen in how bitcoin has been incorporated into decentralized finance (DeFi) as a kind of uber form of collateral.

While we might not use bitcoin to buy cups of coffee, for which dollars or yen or something else will suffice, it could become a fundamental store of digital value upon which the overarching financial system rests.

Right now, if you look at the global bond market, that role is occupied by U.S. Treasury bills, notes and bonds. Those U.S. government debt instruments provide the base-layer collateral upon which Wall Street has built a hierarchical system by which financial institutions extend all other forms of credit to the outside world.

But in the future, once crypto ownership and market participation is sufficiently wide and digital asset markets are sufficiently liquid and sophisticated that price volatility declines, bitcoin could play a similar role. Its protocol-assured scarcity, along with its programmable qualities and its future capacity to interoperate with central bank digital currencies, stablecoins and other digital assets, will ultimately make for a superior underlying store of value than anything a trust-compromised government can offer up.

Don’t be distracted by strong worldwide demand for dollars. Confidence in the U.S. government-led global financial system is eroding, as the bitcoin short position itself demonstrates. Once that loss of trust reaches a tipping point, society will need another form of base-layer collateral to replace U.S. government debt.

Therein lies a post-crisis role for the world’s most important cryptocurrency.

Podcast: stablecoins in Africa and South America

This week’s accompanying Money Reimagined podcast looks at the adoption of cryptocurrencies and stablecoins in emerging markets, which over the past year has seen real signs of life. Is this finally the moment to realize one of the great hopes of this technology: to enable financial empowerment in developing countries where traditional finance is constrained?

To explore that question, my co-host Sheila Warren and I are joined by Elizabeth Rossiello, the founder and CEO of AZA, which has for seven years been developing digital payment solutions in African markets, and Sebastian Serrano, the founder and CEO of Ripio, which has been doing similar work in Latin America for more or less the same amount of time.

Joe six-pack, where are you?

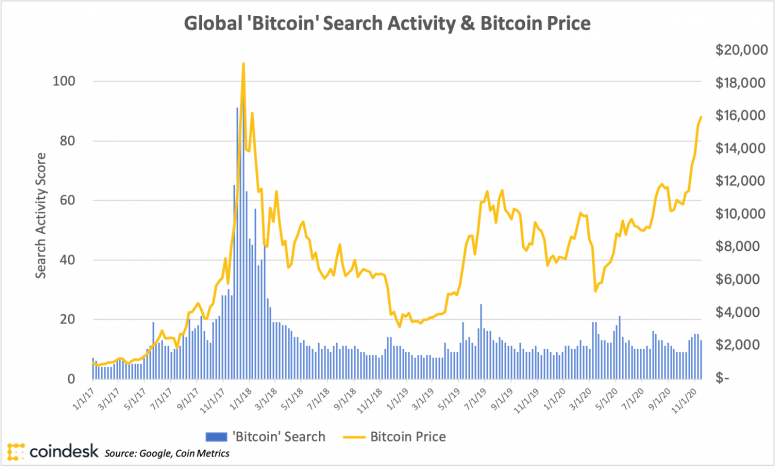

It has been a huge week for bitcoin, whose price is now closing in on the all-time high it hit in 2017 and whose market capitalization has already surpassed the high of that period. But in one very important way, this rally is quite different from that of three years ago. There’s a relative absence of the “FOMO” crowd, the retail investors who don’t want to miss out on the big winnings others are enjoying. And the following chart gives a pretty good representation of that. Unlike 2017, Google search activity around the term “bitcoin” – a proxy for the curiosity of the general population – has hardly budged from the levels of the past few years, even as the price has surged.

Instead of the retail investor commentary, this time the news around this up-cycle is dominated by big-name, deep-pocketed investors discovering bitcoin. It involves people like MicroStrategy’s Michael Saylor, hedge fund veteran Stanley Druckenmiller, Citibank analyst Tom Fitzpatrick and, earlier today, BlackRock CIO for Fixed Income, Rick Rieder, who hinted on CNBC that the world’s largest asset manager, with more than $7 trillion under management, now sees bitcoin as a better hedge than gold. This is a Wall Street rally, in other words, not a Main Street rally.

“Once bitten twice shy” may be the reason retail investors are sitting on the sidelines this time. Too many people lost their shirts by piling into the trade at the peak of the 2017 bubble. Another may be that without the initial coin offering (ICO) boom that fueled an accompanying surge in hundreds of ERC-20 tokens alongside bitcoin, the buzz around the crypto rally generally isn’t as loud.

But I think it’s also worth recognizing the logic of the rally is quite different. This one comes amid a backdrop of concern about the outlook for inflation, fiscal debt and political stability. Those concerns are being addressed by professional investors who are taking a long-term look at bitcoin’s potential as a hedge against all that (as per the column above.) This is less of a get-rich-quick rally, and more of an insurance play.

That’s not to say those bigwigs aren’t also looking to make a killing. It’s also not to say that at some point this “professional” rally doesn’t excite another round of FOMO among the masses. While some investors are starting to protect themselves against a correction, the fact that Joe Six-Pack has yet to jump in could suggest there’s still upside in this for bitcoin.

Global town hall

DIFFERENT KIND OF SAME. “Innovation” is a magic buzzword that conveys progress and daring. That quality makes it ideal for obfuscation. Case in point: a piece on the website of the Official Monetary and Financial Institutions Forum (OMFIF) this week with the title “The second wave of central bank policy innovation.”

If you’re looking for descriptions of radical new digital currency projects in places like the Bahamas, Thailand and China, you won’t find them in this report. What’s meant by “innovation” here is a variety of new means by which central banks are really just extending an existing playbook into new areas, specifically by buying a wider array of assets to pump money into their financial systems. It’s a more extreme, riskier version of the same new policy “tool” that arose after interest rates had been pushed to near zero after the 2008 crisis: quantitative easing.

The problem with endless “QE” is central banks are running out of government bonds to buy; fiscal debt issuance calendars can’t keep up. So, to keep the money expansion going, they are reaching into riskier asset classes, including municipal and corporate bonds. The U.S. Federal Reserve has set the example with its Secondary Market Corporate Credit Facility, with which it buys corporate debt, and with a separate program for buying municipal bonds. Now, we learn from OMFIF that after the Bank of England “introduced a term funding scheme for small- and medium-sized enterprises” in March, the same model has been adopted by central banks in Australia, Taiwan, New Zealand and elsewhere.

With these schemes, central banks, which are supposed to be politically independent, become creditors to entities whose interests can be politicized. If these new debtors face default in the post-COVID debt reckoning, they will be tempted to call on the support of politicians they’ve backed to pressure the central bank to forgive or restructure those debts. This is what will ultimately undermine fiat currencies. Those bonds, now sitting garishly on central banks’ balance sheets as private or political assets, are supposed to more than offset the principal liability: the monetary base. Politicizing those assets will raise concerns about their future value, which will weaken confidence in the currency.

So, whereas the OMFIF piece says these efforts show that “Central banks have shown a continued willingness to reinvent their monetary policy toolkits,” you could equally say they’ve shown a continued willingness to double down a 10-year old bet that’s reached the end of its usefulness.

ELITE FACTORIES. Biologists offer a unique perspective on complex systems such as economies. In studying how ecosystems and species populations can reach breaking points caused by dynamics of the supply and consumption of resources, they find patterns that human societies tend to mimic over time. In that context, the latest observations by Peter Turchin, a pine beetle expert turned cultural theorist, are somewhat alarming.

As laid out by Graeme Wood in The Atlantic, Turchin believes the hierarchies in Western societies like the U.S. are fueling tensions due to an “overproduction of elites.” Societies that have geared their education and professional systems toward rewarding a privileged but relatively large minority are struggling to find constructive uses for them, while the majority who lie outside of that elite bubble have no upward mobility.

This, Turchin suggests, is the root cause of the angst playing out in events such as the still unresolved 2020 election. It’s leading to a breakdown in trust and the failure of institutions.

What does this have to do with cryptocurrencies and blockchains? Well, in theory at least, those systems are supposed to reward people for their participation in open-source, collaborative development and, in their purest form, require no identification to participate. Crypto-based bug bounties, for example, can reward whichever developer finds vulnerabilities in software code without consideration of their identity or educational credentials.

To think a blockchain development community is utopian is, however, naive. There are all sorts of ways in which the privilege of circumstance and upbringing rewards certain people and not others. It is no accident that the vast majority of crypto engineers are white males. It’s a product of a societally formed superstructure – the very same hierarchical system that Turchin said is powering toward its own oblivion. The trick is to figure how to take the best of these open development models while proactively seeding them with newcomers from outside the existing elite production facilities at top-ranking universities.

THE TIP OF THE ICEBERG. The debt crisis fueled by the COVID-19 shutdowns remains in suspended animation. It will get worse once stop-gap measures like rent suspension and mortgage forbearance run out next year as stretched creditors start to demand what is theirs.

In fact, as shown by this Wall Street Journal examination of the U.S. government’s aggressive Payroll Protection Program loans to small businesses, the fallout may already be starting. The reporters found that “about 300 companies that received as much as half a billion dollars in pandemic-related government loans have filed for bankruptcy.”

These numbers will surely rise. And as any student of debt crisis knows, bankruptcies beget bankruptcies. Each debtor’s default leaves their creditors with less funds to pay their debts. A self-perpetuating cycle takes hold.

I think this looming problem is the core driver of why big-name investors are gravitating toward bitcoin. Governments the world over will be confronted with delayed bailout demands far bigger than those they’ve already faced. Can they afford to raise taxes to pay for those bailouts? Hardly. So, many will call on their central banks to do even more than they’re already doing to try to keep their economies afloat. (See the column and the item above for why that will be problematic.) The social covenant of money is at stake. Bitcoin offers an alternative.

Well, that’s a gloomy GTH this week! (My editor, Ben Schiller, suggests rebranding the section to “Apocalypse Watch.”) Sadly, soaring bitcoin prices tend to correlate with bad news for everyone but crypto investors.

Relevant reads

What the History of Airlines Tells Us About Blockchain Commerce. In 2014, when he was at IBM, Paul Brody wrote a groundbreaking piece on the role blockchain technology could play in regulating the internet of things. He opined then on how this would unleash an entirely new economy in which pretty much every asset and product would be in play within a fluid digital marketplace that greatly improved price discovery and resource allocation. Now, as blockchain lead at EY, Brody is a regular opinion writer for CoinDesk. In this piece he returns to his IoT thesis and offers a history lesson on how these shifts could massively disrupt different industries – in this case focusing on digitization in the airline industry.

The Dark Future Where Payments Are Politicized and Bitcoin Wins. I really don’t mean to take issue with JP Koning regularly. He is truly an excellent writer whose clear, BS-free thinking on money adds great perspective to our understanding of how it is evolving. But this is the second week running I feel compelled to counter one of his CoinDesk columns. As I lay out in this week’s column, I think it’s overly alarmist to assume that the only way bitcoin “wins” is for society to go into dystopian meltdown. It’s not an all-or-nothing bet. This is, as always, a good read, though.

Lightning Network’s New Liquidity Marketplace Attracts a ‘Surprising’ Mix of Individuals, Enterprises. The Lightning network has long been promised as a “layer 2” solution to increase the throughput and lower the cost of bitcoin transactions by removing them from the space-constrained main blockchain. The problem is that nodes need to always have pre-seeded funds available inside the payment channels they set up with counterparties. Now, it looks like there’s a decentralized system for resolving those moments when the bitcoin isn’t there. Colin Harper reports.

CoinDesk Daily News. Get your daily fix of crypto news from this brand new, fast moving feature on the CoinDesk videos tab, featuring our new TV anchor, Christine Lee.