One reason I feel privileged to write about digital money is the ideas and technologies it seeks to disrupt aren’t just a few years or decades old. They date back centuries, even millennia.

Like gold, for example.

As bitcoin’s price has soared to new all-time highs and a parade of big-name investment professionals such as BlackRock CEO Larry Fink and hedge fund legend Stanley Druckenmiller have talked up its prospects as a provably scarce store-of-value, a war of words has sprung up between gold bugs and bitcoin fans.

Peter Schiff, one of the loudest proponents of gold as both a store-of-value investment and as a global standard for backing currencies, has been especially triggered. This past week saw a flurry of tweets from Schiff, labeling bitcoin a speculative instrument that lacks gold’s physical safe haven properties and complaining about the lack of airtime given to gold advocates versus bitcoiners. (Check the replies for colorful responses from bitcoin fans.)

This fight reflects something much bigger than a Twitter troll spat. It stems from an audacious effort by the crypto community to rewrite an ancient narrative.

Ultimately, winning the narrative is what will matter in this competition. As we’ve discussed before, a currency can have a host of worthy properties, but if there’s no belief in it, if the story doesn’t resonate, it won’t be accepted as money among a community of users.

Gold: Of kings and conquest

Gold’s proponents frequently mention the qualities that make it a sound store-of-value with which to hedge against fiat currency debasement. Let’s run through them:

It’s durable. Gold can’t be destroyed.

It’s fungible. In its pure state, bullion holds the same value regardless of which bar you have in your hand, enabling its acceptance as both a medium of exchange and store-of-value.

It’s divisible. After smelting, gold can be broken down into coins and ingots of any size.

It’s portable. Within limits, you can transport gold from one place to another.

And most important, it’s scarce. Setting aside the future viability or otherwise of asteroid mining, the slow and expensive pace at which the world’s known gold reserves can be extracted means that, unlike fiat paper currencies, its supply can’t be expanded at will.

Note, these properties are also ascribed to bitcoin – rightly, in my mind, and with a superiority to gold. (Bitcoin is certainly more portable and more easily divisible, and its scarcity is arguably more reliable.)

But while durability, fungibility, divisibility, portability and scarcity are necessary preconditions for sound, non-fiat money, they’re not enough on their own. There are other precious metals, such as silver and platinum, with similar qualities. And there are altcoins literally built from the same code as bitcoin. What ultimately distinguishes both gold and bitcoin from their competitors is the wide collective belief in their shared value.

For gold, this belief is not only widely held. It runs deep. Very deep.

Gold is the stuff of fairy tales such as the one about King Midas. It powered the conquest of the Americas, encapsulated in the search for El Dorado. It became synonymous with wealth and power.

And with beauty – to the point where we talk of gold’s beauty as if it’s innate or intrinsic. But beauty is culturally constructed. While evidence suggests gold’s use in jewelry preceded its use as money, there’s a circular, reinforcing logic to the aesthetic idea. Centuries of associating gold with wealth and power elevated its beauty in our minds.

In other words, there’s a powerful feedback loop arising from the “all that glitters is gold” story. It reinforces its cultural power – an ephemeral, intangible concept that’s actually more important than those five aforementioned physical qualities in giving gold its longstanding status as a universal store-of-value.

Bitcoin: Math for the masses

So, as you can tell, those driving the bitcoin narrative face a daunting competitor, a phenomenon with millennia-old cultural heft.

Yet, this moment feels ripe for a new story. We’ve entered a digital age, where the physical world is increasingly shaped and managed by a separate computing world. That world needs a “digital gold,” not a physical gold.

And it turns out the way to create that digital gold is by combining the power of math – another ancient, all-powerful human invention that rules how we live – with the power of collective human activity. That combination is what makes the bitcoin story so compelling.

At its essence, the proof-of-work consensus model (which lets us trust the transactions recorded in bitcoin’s distributed blockchain ledger) hinges on the fact that it’s mathematically really, really hard to find a randomly chosen number within a data set comprising quadrillions of other numbers. There’s something quite universal – literally, of the universe – in that.

But bitcoin’s claim to provable scarcity, which is fundamental to the store-of-value narrative that institutional investor big shots are now globbing onto, depends on more than its math – which, after all, can be and has been replicated in altcoin forks of the code. It also stems from mass human engagement and investment (of time, money and energy).

Bitcoin’s predictably scarce money supply depends on it being prohibitively expensive for anyone to take control of the network and on there being a sufficiently large, committed, international pool of developers working on keeping its code secure.

That’s where the widening resonance of the narrative becomes self-fulfilling. As more and more people believe in bitcoin, more and more will invest in it, which makes it increasingly expensive to attack it. Meanwhile, wider belief means more and more developers care about protecting bitcoin’s value. Both factors make it increasingly secure, which in turn increasingly strengthens its scarcity claim.

To me, this is what makes the bitcoin story more appealing than that of gold. Rather than stories of kings and conquest, it’s about human engagement under the governance of universal mathematical principles.

This epic narrative battle has a long way to go. I look forward to chronicling its development.

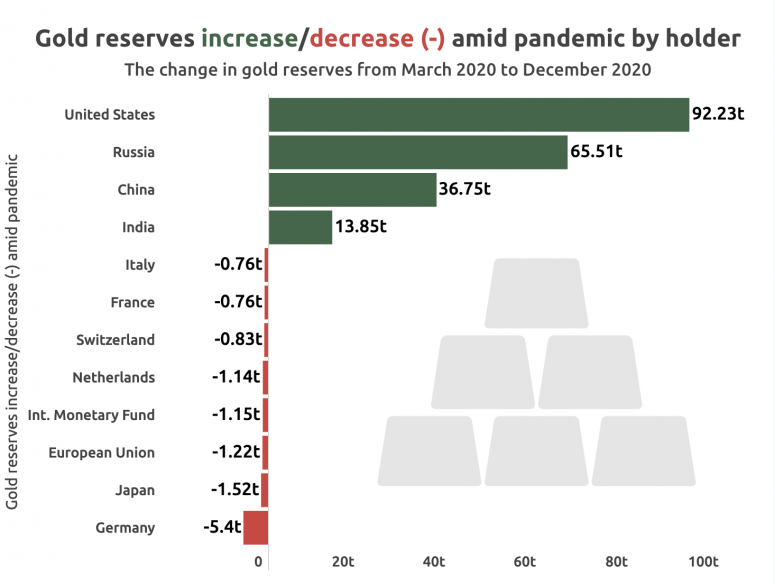

Central bank gold-buying spree

Speaking of gold, this chart in a story by financial news outlet Finbold jumped out at me. From a survey of the 12 largest economies in the world, Finbold found the central banks of U.S., China, Russia and India had accumulated a whopping 208.34 tons of gold between March and early-December this year. Their combined tally dwarfs an aggregate liquidation of 12.78 tons by the eight other countries in that list. It’s not clear where Finbold got its data from and it should be noted that central bank gold reserve information is notoriously difficult to confirm. But with that caveat in mind, the numbers are worth exploring.

Why the big buildup in gold holdings by these four countries since the COVID-19 pandemic became a global crisis? The natural answer is that, like people, governments see gold as a hedge against economic and monetary stress, and the crisis has elevated the risk of that. But thinking about the four countries’ individually offers some other hypotheses.

The U.S. and Indian numbers are somewhat self-explanatory. For the U.S. Federal Reserve, its massive mid-pandemic monetary expansion necessarily required the buildup of a giant balance sheet of financial assets, of which gold was a part. And India, mostly for cultural reasons, has always been a giant gold buyer, so these numbers are perhaps just an extension of that.

The Chinese and Russian stories are potentially more interesting. Typically, these two countries buy dollars, held in U.S. government Treasury bonds, as their reserve asset. That they’re also accumulating gold could point to something of a loss of confidence in the dollar. More important, the question is what they might do with that gold in the future.

And that’s where an insight from Jennifer Zhu Scott, executive chairman of The Commons Project, makes this interesting. Speaking during a recent Money Reimagined podcast episode, she noted that although it’s clear that China has been growing its gold reserves significantly, no one knows for sure how much it holds. That, she speculates, could put China in a powerful position to give the digital yuan clout in the international marketplace.

“When the digital [renminbi]is launched, China doesn’t even need to say this is backed by gold. China might just make an announcement saying ‘Oh, by the way, our real gold reserve is actually 4,000 tons.’” (According to Finbold, China’s total holdings currently stand at 2,196 tons.) That would give the new digital currency a solid basis, which may encourage other countries to use it. At the same moment, it would allow China to avoid the volatility it would otherwise face when it ends capital controls, a step it must take if it is to achieve wider international usage of the yuan.

What about Russia? Well, like China, one of the reasons it is thought to be keen on creating a digital currency is to have a mechanism by which it can reduce its dependence on the dollar – in its case, to achieve the explicitly expressed goal of avoiding U.S. sanctions. A hefty gold reserve might also help it do that.

The bigger question, as per the column above, is whether these countries will eventually be better off accumulating bitcoin, rather than gold, as the backstop to their currencies.

Global town hall

THUMBS DOWN. A column by Sarah Frier in Bloomberg’s daily “Fully Charged” newsletter this week highlighted the excessive power Facebook wields over advertisers and the audiences they seek. Small businesses that have become dependent on Facebook ads for lead generation are now frustrated to find themselves in “Facebook jail” – locked out of the platform by an algorithm that’s supposed to police inappropriate content across its 3 billion users. The problem, Frier writes, is that “tiny glitches or misfires of this system can take down innocent users, who then have to hope a real human sees the mistake and resolves it. That’s a process that can take days, if it happens at all.”

The article is another example of the growing recognition that big centralized Internet platforms such as Google and Facebook have de facto monopoly powers that can harm the economy, a mindset that is feeding into the increased risk of antitrust action against them. As Frier writes, “For a company that’s fervently trying to convince lawmakers it’s not a monopoly, some advice: It’s usually a bad thing when an entire sector of the economy is dependent on your service in order to survive.”

What’s still missing from the mainstream conversation about these problems is a discussion of how more decentralized models of media control might better address them. Whether it’s a blockchain solution or something else, we need to recognize that the centralized architecture of internet platforms is the root of their gatekeeping powers. Whatever the solution, that context is vital for how society thinks about a redesign of the social media and digital content industry.

STABLECARD. The expansion of stablecoin payments was given another boost this week when Forbes’ Michael Del Castillo ran a story saying card network Visa would give its 60 million merchants worldwide access to USDC, the stablecoin token developed by Circle Internet Financial and CoinBase. What’s interesting about that is USDC, as a bearer token, can move across borders from one party to another without the need for an intermediary. What it didn’t have was the network of users Visa offers. This looks like a solution for moving money internationally without using correspondent banks and the SWIFT messaging system. Another step toward disintermediated global finance.

BTC YIELD. Dan Held, who heads up growth at crypto exchange Kraken, has done a favor for everyone interested in turning their otherwise static bitcoin into an interest-earning asset. There are a host of ways to earn yield on your bitcoin these days and Held, who has been experimenting with them over much of the past year, created a summary of experiences and results in a useful tweet thread.

What I find interesting is that Held’s thread gives you a sense of the DIY nature of an emerging, decentralized financial system. In this system, bitcoin becomes a universal reserve asset, a form of collateral against which loans and speculative positions form.

Note: Interest payments in bitcoin markets are mostly derived by speculators, who borrow bitcoin from entities such as BlockFi to place short-selling bets. One way they do so, as Held points out, is to play the arbitrage between spot market prices and those quoted on derivative assets such as the CME bitcoin futures of the Grayscale Bitcoin Trust, or GBTC. (Grayscale is owned by Digital Currency Group, which is also the parent company of CoinDesk.) That’s quite different from, say, earning interest on your dollar deposits at a bank, but it does look like how a lot of funding happens in the interbank market. Banks obtain short-term funds by lending out Treasury securities and other collateral, which are then used in short-selling operations.

For now, at least, it’s people, not institutions, who are providing the collateral and liquidity need for the back office aspects of a capital market system.

Relevant reads

Why Ethereum and Bitcoin Are Very Different Investments. News you can use. The soaring price of bitcoin has in recent weeks coincided with concurrent gains in ether and other tokens. This gave the impression that retail investors are simply buying the latter as a substitutable alternative to the former. Here, CoinDesk’s Muyao Shen explains why that assumption is wrong.

Bitcoin’s Price Is a Poor Proxy for Its Utility. As bitcoin investors celebrate its new all-time highs, CoinDesk columnist Jill Carlson is here to tell you to chill out and focus on what matters. Crypto, she reminds us, is supposed to be about expanding access to money, payments and finance, not earning legacy currency-denominated gains.

US Lawmakers Introduce Bill That Would Require Stablecoin Issuers to Obtain Bank Charters. This bill, introduced by Rep. Rashida Tlaib (D-Mich.) and others, may be a well-intended effort to protect consumers. But the overwhelming backlash from crypto experts, including many sympathetic to Tlaib’s interest in curtailing abuses of the little guy and boosting financial access, shows how badly it was thought out. Imposing high compliance costs on innovative startups trying to boost financial access will ultimately benefit banking behemoths that have failed to service the poor adequately. We need better-informed legislators. Nikhilesh De’s write-through looks at some of the fallout.