For Australians of my generation, historian Geoffrey Blainey’s phrase the “tyranny of distance” was the defining descriptor of our place in the world, a place that seemed awfully far from everyone else.

In September of 2020, with hundreds of millions of broadband-connected homes using global video-conferencing services like Zoom and with remote work the norm for white-collar workers everywhere, we might believe distance is now a non-issue – not just for Aussies but for anyone. In the COVID-19 era, geography seems irrelevant.

But while the internet has removed location as a constraint on communication and leveled the playing field for building human and business connections, we can’t say the same for how we exchange value with each other – at least not yet. The cost of using money and the capacity for middlemen to charge transfer fees very much depends on where you are.

Location will determine how much it costs you to move money around the world: 1% transaction fees for sending to London from New York, for example, versus 19% from Botswana to London.

Just as important, it dictates the power structures within the management and control of money. After centuries of controlling the terms of the world’s financial deals, cities like New York and London have developed influential banking industries, which in turn have made those places powerful in their own right.

But for the first time, we have a vision for how this could change. The great promise of cryptocurrencies and stablecoins is that they could do for money what the internet did for communications. They could make the geography of finance obsolete.

Internet protocols like TCP/IP for data routing, VOIP for voice transmission and HTL for video streaming, combined with constant advances in file compression technology and cheap recording devices, have allowed people to exchange information directly, bypassing the telcos and other gatekeepers. They’ve made peer-to-peer communication available to all at essentially the same low cost.

Similarly, when everyone is using peer-to-peer money and intermediaries are no longer taxing and controlling our exchanges, barriers to entry will fall, as will the cost of payments. The capacity to transact will no longer vary according to where you are. And, in the long run, it will eat into the power of the world’s great financial centers.

KYC geography

Why hasn’t this happened already? Why hasn’t the rise of crypto forced the banking titans of New York, London and other financial centers to succumb to a more open system in the way that the telecom monopolies had to?

Because banks are completely entangled with political power. And, thanks to the continued dominance of nation-states, power is still tied to place.

The leaders of our financial system derive far greater advantages from their incumbency than the telcos ever did, in large part due to the barriers to entry that industrialized country banking regulations impose on potential competitors.

Some of those regulatory barriers exist in what appear to be benign and seemingly justifiable circumstances. Nonetheless, they create imbalance in geographic power.

Consider the asymmetric impact of know-your-customer and anti-money-laundering (KYC/AML) compliance rules. Installed at the behest of developed-world governments to track the money flows for rogue regimes, terrorists and international criminals, they impose big barriers on people living in much of the developing world, where regulations and enforcement aren’t as trusted.

After the Sept. 11 attacks in 2001, and then following the financial crisis seven years later, a ratcheting up in compliance requirements and fines made U.S. bankers more risk averse. The upshot: “de-risking.” Investment flows to supposedly risky jurisdictions in developing countries slowed down, which meant fees on remittances and other financial transactions there rose, adding to the already high cost burdens that people in those countries face in trying to participate in the global economy.

Exemptions, in theory, allow people to send or receive funds up to $3,000 per day with only limited requirements for reporting their identification. But banks, chastened by massive fines imposed on HSBC and Standard Chartered and now heavily staffed with compliance officers whose instinct is to say “no,” don’t want to take any chances. So they apply blanket bans on people and businesses in places from Somalia to Venezuela. It also means bankers tend to view cryptocurrencies as tools to get around such rules, rather than focusing on their many advantages in reducing transactional friction and costs. It meant that crypto startups also got de-risked by banks.

Appeals to lighten such restrictions fall on deaf ears. The poor have no lobbying power; the politics of playing tough with international criminals carries much more populist appeal.

If anything, rules are getting stricter. The extension of the Financial Action Task Force’s “travel rule” to cryptocurrency exchanges is bringing in a vast new ID and reporting framework for the industry, which will make it even harder for people without trusted IDs to use them to send or receive money to or from abroad.

It’s frustrating because some of the most innovative solutions for controlling illicit finance, while still keeping payment corridors clean, come from crypto developers. By combining cryptographic privacy solutions such as zero knowledge proofs with the tracking capabilities found in blockchain provenance solutions, new AML modeling approaches promise to give both financial institutions and regulators a rich view of criminal money flow patterns without, for example, requiring Somalians to furnish IDs they don’t have. Check out this study by researchers at the IT-IBM Watson AI Lab, which ingested a giant trove of pseudonymous bitcoin transactions to draw conclusions on how many were illicit and where they were going.

But officials and banks simply aren’t open to anything that softens existing ID requirements. When I was at the MIT Digital Currency Initiative, we explored a privacy-protected tracking project to help crypto exchanges stay compliant while allowing undocumented Mexican immigrants to send money home. The project stalled when, after various meetings, U.S. Treasury officials made it clear they thought we were just peddling naive crypto-anarchist ideas that would help only bad guys.

Preserving US power

The reality is that political resistance is about more than fighting drug dealers. It’s also driven by a desire to project and protect American power.

The reserve-currency U.S. dollar is the intermediary for nearly all other cross-border payments, which means a huge chunk of the world’s transactions pass through U.S. correspondent banks whose headquarters are typically in New York. In a clear expression of the geography of financial power, that gives the state’s New York City-based enforcement agents outsized power worldwide. Witness the crypto community’s obsession with the New York Department of Financial Services’ “Bitlicense.” No other state or provincial regulators command that kind of attention anywhere else in the world.

Together, Washington and New York leverage the banks’ gatekeeper role to police the world’s transactions and project U.S. power. It allows them to impose sanctions on foreign entities doing business with U.S.-sanctioned states such as Cuba, Venezuela and Iran, even when those entities have no business of their own in the U.S.

There is very little political will to end this nexus of power between U.S. regulators and New York’s banks. So inefficient, costly, and restrictive banking intermediaries will hang onto their privileged position for some time, while the rest of us pay them fees that we’d be better off applying to real-world expenses.

Yet, just as the telcos eventually lost their gatekeeper status in telephony, so will the banks inevitably lose their stranglehold on finance.

Various factors could bring this about. The rise of China’s and other countries’ central bank digital currencies will create new avenues for foreigners to bypass dollars in their international transactions. The rising popularity of bitcoin and stablecoins for payments in dollar-starved developing economies during COVID-19 will limit U.S. banks’ capacity to control money flows there. And a surging gold price hints at waning confidence in U.S. financial leadership overall as the Federal Reserve continues unprecedented money issuance.

Meanwhile, the experimentation with new crypto-based mechanisms for moving money around the world is exploding, whether in the Lightning Network, new algorithmic “crypto-dollarization” plays, or in decentralized finance (DeFi).

Here’s the thing: Money is information. It’s just that it’s a special type of information requiring trust if it is to be exchanged meaningfully.

So as cryptocurrency decentralizes trust on the internet, money will also detach itself from geography.

American Dream, bifurcated – in four charts

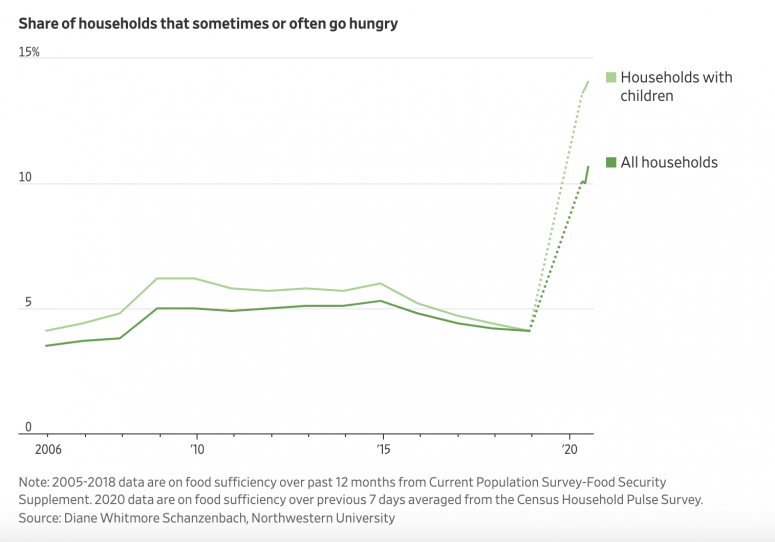

Reading a Wall Street Journal article on the challenges faced by poorer U.S. households during the COVID-19 pandemic, a chart based on work by Diane Whitmore Schanzenbach of Northwestern University, jumped out at me. I’ve pasted it below. The pandemic has spurred a sharp jump in the number of households reporting that they sometimes or often don’t have enough to eat, and that it’s especially pronounced for households with children. Strikingly, these trends are occurring as the stock market reaches record highs. What a statement on how divided U.S. society has become in this era.

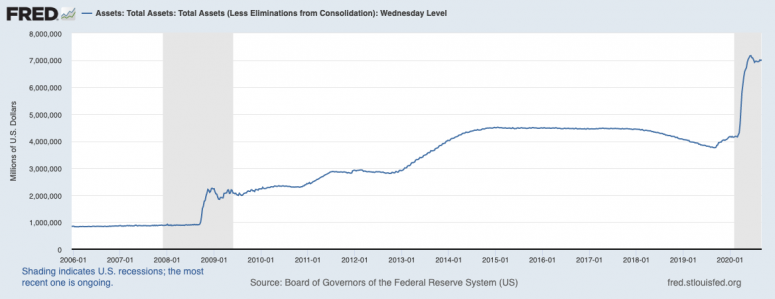

As Money Reimagined and many others have written, the stock market surge during a period of mass unemployment is a function of the easy monetary policy enjoyed by the financial sector. So, to emphasize the disparity in U.S. economic fortunes, let’s juxtapose that household hunger chart with one an illustration of what the Federal Reserve has been doing. Here’s the latest on the Fed’s balance sheet – a measure of how much new money it has pumped into markets in return for bonds and other assets. Per the St. Louis Fed’s FRED database, we’ve matched it to the time frame in the WSJ chart:

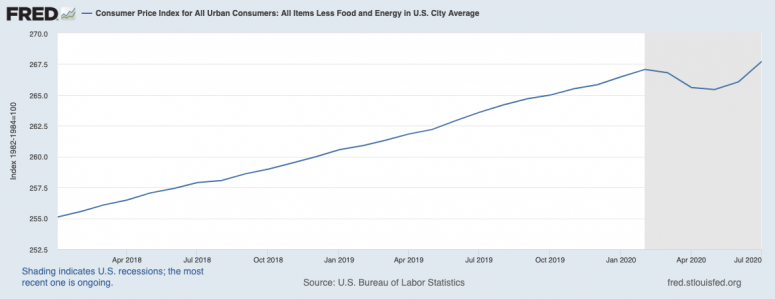

The Fed, according to its mandate, is focused on inflation. If it gets too high, the central bank will eventually have to start selling those assets to suck up all the excess liquidity it has pumped into the market (though the latest change in policy suggests it will wait a bit longer than previously intended before doing that.) Right now, inflation is not only benign but below trend, as seen in the Fed’s preferred metric, which takes the consumer price index and extracts volatile food and energy prices to create a smoother measure of ongoing trends. (For this chart we asked FRED for a shorter time frame, starting in early 2018, to more clearly reveal the dip in the CPI.)

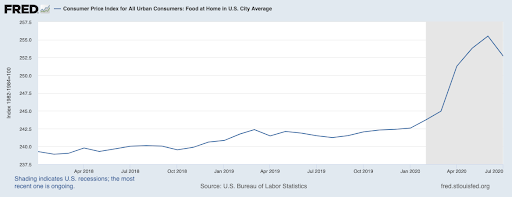

But there’s a disjuncture here, no? If the Americans who’ve lost their jobs in the pandemic are struggling to put food on the table, surely we need to look at how much food itself costs. This is where the inequity really gets stark. Here’s what FRED says was the CPI for “food at home” over the same period.

Together, these four charts paint a picture of American policy-making gone wrong. Could there be a bigger measure of a society’s failure than a near-tripling in the proportion of children facing malnutrition at a time when financial asset holders have never owned more wealth?

And in case you’re wondering whether the distribution of federal funds (via the Fed or national government) can make a difference, there’s some telling details in the U.S. Census Bureau’s weekly household survey that Whitmore Schanzenbach used to construct her time series on hunger. In just one of the weeks in the bureau’s surveys running from early May through mid-July, there was a sharp interim dip in the number of households reporting insufficient food – down to normal, pre-COVID levels. No prizes for guessing that it was the week after the first round of $1,200 stimulus checks were mailed out by the federal government, a check for which most well-to-do beneficiaries of the Fed-fueled stock market surge should not have been eligible.

The global town hall

BITCOIN’S AFRICA MOMENT. The story of bitcoin adoption in Africa this year keeps getting more interesting. This week, Reuters pushed out a well-syndicated story on the rapidly growing adoption on the continent, citing data from Chainalysis that showed a 55% jump in transfers to and from Africa of under $10,000 and a similarly sized increase in the number of transfers. Together, the data offer an interesting insight: The driver behind Africa’s bitcoin awakening lies in small transactions and payments. It’s the other end of the spectrum from the “digital gold” narrative that dominates the more speculation-driven activity in the developed economies, where concerns about future inflation and the threat to the existing dollar-based financial system are cited as motivators for investments, not payments. The question is how efficiently these smaller-value crypto transfers are taking place, given the state of bitcoin transaction fees now and in the future? Is the rollout of off-chain Lightning Network-based solutions helping make transactions more affordable? Or are Africans just recognizing that, amid a shortage of dollars and highly volatile local currency rates, bitcoin transaction fees are a price worth paying? The answer matters because advocates for bitcoin for developing world payments will continue to confront high on-chain costs as activity on the network grows.

HOW TO OWN (ONLY) THE MONA LISA’S SMILE. As discussed in previous editions of Money Reimagined, periods of monetary extravagance, like the current one, often result in a run-up in fine art prices. With nowhere else to go as yields keep shrinking, the excess dollars go toward things of proven scarcity, value and tax benefits. The art market hits all three.

For centuries, though, the high-end art market was only an option for the super wealthy. Now, in an age where Robinhood day traders are a key part of the stock market frenzy, a similar retail-driven surge is happening in the ownership of art and luxury assets. So says this Bloomberg article on the startups doing a surging business selling people fractional ownership of Warhol paintings and racehorses with just a few thousand dollars invested.

What’s not mentioned is that at least two of the startups involved, Masterworks and Acquicent, use blockchain technology to create the fractional ownership securities they sell to investors. It’s a booming blockchain use case that no one seems to realize is a booming blockchain use case. Perhaps that just speaks to how far we’ve come from the ICO boom days when the Long Island Iced Tea company added the word “Blockchain” to its name to get a surge in its stock price. Now, firms are pushing the technology into the background of their marketing efforts.

For these kinds of products at least, that’s as it should be. Blockchain is just the back-end architecture piece. Companies don’t talk about their websites or apps as “TCP/IP sites” or “HTTP apps.” The less the consumer knows about how the sausage is made the better.

BIKERS BEWARE. Last week a report was released by four economists finding the 466,000 attendees at last month’s Sturgis Motorcycle Rally in South Dakota were responsible for the spread of 266,796 cases of COVID-19. It’s a tally worth 19% of all cases at that time and which, by the economists’ estimates, would have cost the public $12.2 billion in health-care costs. Not surprisingly, the story, which was ripe for “told you so” responses, went viral among more liberal-minded social media participants. But it also got some inevitable blowback. The Wall Street Journal complained that bikers were being blamed for irresponsible behavior while Black Lives Matters protesters were getting a free pass. And with Slate finding holes in the assumptions the economists used for their calculations, South Dakota Governor Kristi Noem called the report a “fiction” based on “back of the napkin math.”

It’s interesting to think about what could have been achieved if the researchers could take their work to further technological extremes. The economists used anonymized cell phone data to track the movements of out-of-stake Sturgis attendees back to their homes and then drew conclusions about their role in case surges that happened to appear in their home counties following their return. But there are just too many other unaccounted variables that potentially contributed to those gains and the numbers are just far too big to make the model seem realistic.

Even so, just imagine if access to that cell phone data were extended into the kind of per-person contact-tracing efforts many are calling for. What could we learn about the dynamics of “super spreader” events and how might it help schools and businesses find the right balance as they endeavor to reopen this fall? To get there, especially with a community of fiercely “pro-freedom” anti-maskers such as those at Sturgis, we’re going to need privacy-protecting software. Alas, despite numerous startups developing blockchain-based apps to help that pro-privacy contact-tracing effort, we are no closer to seeing such solutions in the wild.

Relevant reads

DeFi Is Hot but Retail Interest Nowhere Close to ICO Frenzy. For those of us who lived (and survived) the boom-bust mania of the 2017 ICO boom, much of what’s currently happening in decentralized finance (DeFi) seems familiar. But after taking a look at the data, CryptoX markets reporter Omkar Godbole is here to tell us that the kinds of mom & pop investors who jumped on the ICO bandwagon are not to be found this time, at least not in the same numbers. I think that’s a good thing. The fewer mainstreamers who can lose their shirts, the better DeFi can function as a kind of living lab for financial innovation.

First Mover: SushiSwap’s Billion-Dollar ‘Rug Pull’ Is Thriller to Crypto Geeks. There is a key parallel with DeFi and ICOs that investors must be cognizant of, however. That is DeFi founders – helped by anonymity – similarly hold the potential to run off with their investors’ pumped-up winnings. That’s what DeFi protocol SushiSwap’s pseudonymous founder Chef Nomi did when they sold all their SUSHI tokens and triggered a 73% plunge in their price. Here, the First Mover team breaks the saga down for you.

CryptoX 20 Update: OXT Is In, BAT Is Out. The CryptoX 20 is now three months old. That means that it’s time for this new curated list of market relevant digital assets to go through its first quarterly review. After applying the “real volume” criteria that establishes membership of the list, our team found that one change was required to the rankings: decentralized VPN provider Orchid’s OXT is now in the 20, replacing the outgoing basic asset token (BAT), Brave Software’s tradable unit for a new decentralized digital media economy. Here, Galen Moore explains the methodology.

Bitcoin, Mescaline and Parallel Worlds. Money is imaginary, but that’s what gives it its power. In this review of David Z. Morris’s book, “Bitcoin Is Magic,” CryptoX columnist Leah Callon-Butler dives into a world of memes, iconography, religion and Aldous Huxley’s mescaline experiments to explore how the bitcoin community uses its collective imagination to imbue it with value.