For this special Halloween edition, CryptoX Executive Editor Marc Hochstein weighs in with a guest column about the spookier aspects of the banking system. It’s a perfect follow-up to last week’s newsletter on the harmful legacy of the U.S. Bank Secrecy Act.

Before you dig into it, let me remind you to check out this week’s Money Reimagined podcast. In this episode, Sheila Warren and I interview the newly reelected premier of Bermuda, David Burt, who is spearheading projects to use the island as a testing ground for stablecoins and to launch a communally-owned national digital bank.

With Halloween and the 12th anniversary of the Bitcoin white paper approaching, it’s an apt moment to consider a classic horror trope through a monetary lens.

From Mary Shelley’s “Frankenstein” to George Romero’s “Night of the Living Dead,” to Jordan Peele’s “Us,” some of the scariest tales suggest that “normal” people are more nefarious than the nominal bogeymen. This is a useful way to think about the allegedly abominable qualities of cryptocurrency when compared to the incumbent institutions it challenges – and the supposedly safer visions they are now putting forth.

Since CryptoX is a family publication, I won’t go into the details of those gory fictional works. Besides, because there’s an element of farce here as well, I’ve got an even better seasonally appropriate metaphor: “The Munsters.”

For the 99% of readers too young to remember, this was a 1960s sitcom about an eccentric family who live in a cobwebbed mansion and resemble iconic movie monsters. The patriarch, Herman Munster, is a dead ringer (ahem) for Frankenstein’s monster, his wife and father-in-law are vampires, his son a werewolf. They’re a friendly bunch but never quite understand why the neighbors act so strangely around them.

The most important character for this discussion is Marilyn, Herman’s teenage niece. She isn’t a monster at all; she’s the archetypal Girl Next Door. The running gag is that the other Munsters pity Marilyn for her looks, and even she somehow blames herself when boyfriends run away screaming upon meeting her relatives.

Just like Marilyn Munster, the Bitcoin network is a wholesome outlier among the frightening creatures of the legacy financial system.

The censorship monster

The cryotocurrency’s chief value proposition, censorship resistance, is not a radical departure from tradition as sometimes implied. On the contrary, it’s the way money’s been since the days of cowrie shells. All Bitcoin did was restore it for transactions over the internet.

You go to a butcher shop, you hand a few banknotes to the guy behind the counter, he gives you a steak. No third party who thinks you should be eating soy instead can veto the transaction. That’s normal.

What’s abnormal is busybody A pressuring intermediary B to prevent individuals C and D from transacting, even lawfully. Even more abnormal is moving to a world where every last C and D has no choice but to rely on a B and therefore lives at the mercy of the As.

None of this is to say that intermediaries are going away, nor that they should. They can add value. The problem is having no choice but to use one, which makes them choke points to be exploited by scolds and tyrants.

Possessed, like Linda Blair in “The Exorcist,” you might say.

The asset seizure monster

Another characteristic bitcoin (loyalists to other crypto tribes may substitute the asset of their choice) shares with older forms of money, and not the electronic kind that sits in your bank account, is that it is a bearer asset. Like cash, once you lose it, it’s gone, and it’s the holder’s burden to keep it secure through careful storage of their cryptographic private keys.

Yes, this is scary, as many crypto investors can attest. But also scary is cops seizing assets of people who haven’t been charged with a crime and putting the burden on them to prove an asset wasn’t involved in a crime. What’s even more terrifying is moving to a world where ALL money is held at intermediaries who must comply with such a regime.

In this context, the advantage of a bearer asset secured with public-key cryptography is that the authorities cannot unilaterally seize someone’s funds by subpoenaing a bank. They need the key holder to cooperate, even if under duress. As I’ve written before, this “claws back a modicum of power for the individual” from the lurking Leviathan.

The surveillance monster

One more commonality with cash is that bitcoin requires no personally identifiable information to handle – at least, the basic open-source software doesn’t, even if regulated exchanges demand it.

The pseudonymity of alphanumeric addresses, along with the aforementioned resistance to seizure and censorship, go a long way toward explaining the technology’s popularity among criminals and other unsavory types.

“Current terrorist use of cryptocurrency may represent the first raindrops of an oncoming storm of expanded use,” warned a recent report by a U.S. Department of Justice task force. The laundering of illicit funds, the report pointed out, “can be substantially easier when the movement of funds takes place online and anonymously.” That’s enough to give anyone goosebumps.

But remember that the demand for legibility of financial flows is a modern phenomenon. The U.S. Bank Secrecy Act only just turned 50 (with mixed results at best, as Michael J. Casey wrote last week). Depending on how you define it, money has been around for as long as 5,000 years.

Legibility is the aberration. Legibility is an ongoing experiment.

That experiment has spawned its own terrors. Consumers in today’s digital world must entrust sensitive personal data to an untold number of hackable organizations, Equifaxes-in-waiting.

Even more chillingly, the powers-that-be want to double down. U.S. regulators recently proposed lowering the threshold for the “travel rule” to $250 from $3,000 for international money transfers. Under the travel rule, if you wire someone money, not only does your bank know your name, account number and address, so must the recipient’s bank, and it keeps a record for five years. And if you receive money, there’s a chance the sender’s bank has your name and address as well. Perhaps this makes sense for high-roller transactions, but $250?

The inflation monster

Also, note that $3,000 in 1996, the year the travel rule was created, is equivalent to nearly $5,000 in today’s dollars.

So even if the regulators don’t follow through on their proposal to lower the threshold for international wires, it’s already been happening in slow motion, thanks to inflation. Every year the dragnet widens a bit automatically, just as it has for the cash transaction reports banks file to the government.

The upshot is that, by default, more and more personal information is likely to be captured over time.

And that brings us to the last way bitcoin is a return to form rather than a deviation, although this one is perhaps the most controversial.

While its exchange rate with the dollar fluctuates wildly from minute to minute, over time bitcoin has appreciated mightily in value. To detractors, the short-term volatility makes it useless as a currency; to proponents, the long-term appreciation and hard supply cap make it the ideal currency, one that incentivizes saving.

They have a point. “A penny saved is a penny earned.” That’s normal. Or was – it’s the kind of thing you hear parents say in black-and-white sitcoms.

“Stop whining about low interest rates, hoarder. It’s your patriotic duty to blow your discretionary income at the mall or wager it on stonks, we need to keep the economy moving.” That’s the stuff of nightmares.

Betting the company on bitcoin

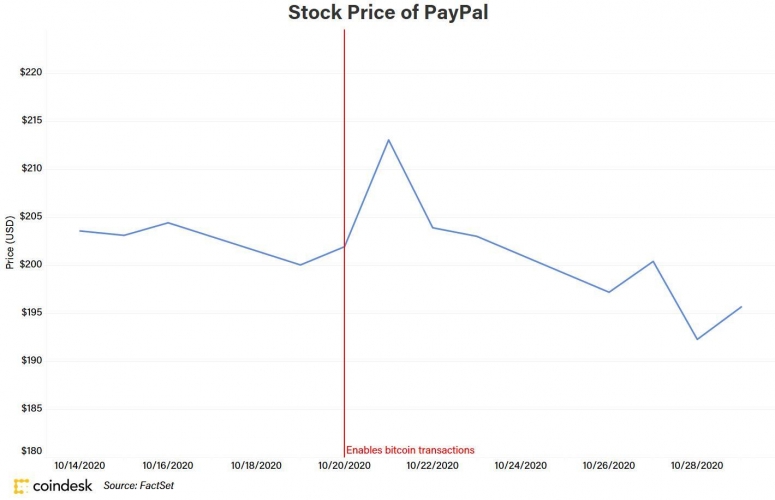

As the price of bitcoin has surged higher in recent months, a string of listed companies has announced they are engaging with the cryptocurrency. On Aug. 11, business intelligence firm MicroStrategy bought a whopping $250 million worth of bitcoin before adding another $175 million on Sept. 15. Three weeks later, payments company Square put $50 million into the cryptocurrency. Then, on Wednesday last week, U.K.-listed fintech firm Mode Global Holdings revealed a “significant purchase” of bitcoin for treasury management purposes and PayPal confirmed it would enable bitcoin transactions on its payments app.

In the first three cases, the companies essentially embraced the thinking of many bitcoin bulls, treating the cryptocurrency as a “digital gold” hedge with which to protect their liquid assets against future monetary stress. With PayPal, the action was likely more geared toward leveraging an anticipated rise in public demand for bitcoin. For all four, the announcements boosted the companies’ stock prices.

There have essentially been two reactions to these moves.

One camp saw them as smart, proactive steps to front-run a trend toward wider mainstream acceptance. That view holds that at least some amount of bitcoin belongs in everyone’s investment portfolio because it functions as a valuable, uncorrelated asset and that this is now of greater relevance as uncertainty grows around the future of the global financial system. The other camp saw it as a rather cheap, even cynical move to piggyback on bitcoin’s current rising price to boost the firm’s stock price. As of late Thursday, New York time, bitcoin was up 21% from the end of July and up 17% from two weeks earlier.

A chicken-and-egg problem complicates the assessment of these two perspectives. These high-profile announcements were not neutral; they directly contributed to bitcoin’s price gains and elevated the conversation around its relevance in hedging strategies. In turn, that boosted these companies’ valuations – especially of MicroStrategy, whose bet was so large that the rising price in BTC materially increased its book value.

But bitcoin is, of course, just one of a number of factors that will affect these companies’ share price, and a small one at that. So with that in mind, let’s look at their price charts as of Thursday to see how their shares performed around those announcements.

The global town hall

PANDEMIPRENEURS. Necessity is the mother of invention, or so the saying goes. There’s been an extraordinary large number of new U.S. companies created this past year, according to Bloomberg columnist Justin Fox. Some 3.5 million new business applications were registered by the Internal Revenue Service in the first 42 weeks of the year, up from 2.9 million for the same period last year, an impressive number given the doom and gloom around COVID-19.

Fox points out that this often happens during a recession, as individuals who can’t find jobs strike out on their own. But this time the trend has been reinforced by factors unique to this social and economic phenomenon. For one, credit has been easier to come by than, say, during the Great Recession of 2009, which stemmed directly from a debt crisis. In part, that’s thanks to the small business loans rolled out in the COVID-19 stimulus package, and in part due to rising home prices as city dwellers fled to safer work-from-home environments.

Yet, the trend may also reflect the inventiveness unleashed by the crisis. The unusual circumstances, whether it’s the challenges posed by the WFH scenario or surging hospital demands for protective equipment and respirators, entrepreneurs have confronted an array of problems to solve.

The cryptocurrency community has been a part of this. Witness the surge in DeFi innovation – not exactly saving nurses’ lives but seizing on the opportunity posed by the COVID-related debt problems that loom for centralized finance (CeFi) – or the frenetic efforts of blockchain engineers and cryptographers to build privacy-preserving contact-tracing solutions. As an industry with open-source development at its core, the sector is also something of an enabler of this trend. It fosters an environment of cross-border collaborative invention, which speeds up the entrepreneurial process.

We don’t know where all these ideas will go, but something good will surely emerge from them. Maybe one day we’ll view these dark days more favorably than we do currently.

Relevant reads

Iran Amends Law to Allow Imports to Be Funded With Cryptocurrency. One way to read Iran’s embrace of bitcoin to avoid U.S. sanctions is to see it as an advertisement for the cryptocurrency’s core value proposition as a censorship-resistant means of payment requires no third-party intermediation – such as a U.S.-regulated bank. The other way is to see all of that as a reminder of why bitcoin will continue to make U.S. regulators exceedingly uncomfortable. Read Daniel Palmer’s update.

All-In on DeFi: Why the Days of Centralized Exchanges Are Numbered. Binance, the most successful crypto exchange of all time, is based on a centralized model. So, you should sit up and take notice when its charismatic founder and CEO Changpeng Zhao says it’s time to go all-in on decentralized exchanges. Check out the op-ed he penned for CryptoX.

Bank of Canada Governor Says Digital Dollar Project Moving Past Trial Stage. Canada appears to have come out of nowhere with its digital currency, with its central bankers making increasing noise about the urgency with which they are developing it. Might Canada be on China’s heels with a real-world launch? Report by Sebastian Sinclair.

Avanti Financial Joins Kraken as a Wyoming-Approved Crypto Bank. The woman who almost single-handedly drove a dramatic legislative initiative in Wyoming to turn it into a crypto-friendly jurisdiction, is now reaping the benefits of that work. Caitlin Long, the founder and CEO of Avanti Financial saw its banking charter approved unanimously by the Wyoming State Banking Board on Wednesday, becoming the second newly chartered bank in the state in 2020 after Kraken Financial earned approval last month. Nathan DiCamillo reports.