Byrne Hobart, a CoinDesk columnist, is an investor, consultant and writer in New York. His newsletter, The Diff (diff.substack.com), covers inflection points in finance and technology.

The bull case for bitcoin as a store of value is simple: at first nobody owns it. Then it’s owned by people who are some combination of crazy and smart, but generally crazier than they are smart. Over time the craziness requirement drops, more investors buy it and it becomes dumb not to own a little. Since existing monetary systems are necessarily optimized for the status quo – and the dollar is, in fact, very well optimized for a globalized world with a hegemonic United States – an alternative system like bitcoin is necessarily a bet on a weirder world.

We certainly live in a weird world today.

And some sophisticated money managers are taking notice.

Paul Tudor Jones II, a well-regarded global macro investor, made headlines last week when he announced he’d bought bitcoin and planned to invest up to a single-digit percentage of his net worth in the currency. PTJ is not exactly a nose-ringed millennial day trading on Robinhood. He’s been running his fund since 1980 and has accumulated almost $40 billion in assets under management.

Jones is best known as a global macro investor, placing bets on interest rates, currencies and commodities. He founded his firm at the beginning of a golden age of macro investing, as the world worked through the implications of the collapse of the Bretton Woods system, volatility in oil and the rise of Japan. In one five-year period, Jones’ worst annual return was 99.2%. But since the heady days of the 1970s and 1980s, macro has gotten more challenging, and the pace has slowed. Aggressive traders used to be a powerful force (in the mid-1990s, U.S. President Bill Clinton was shocked by how powerful funds were, exclaiming to an adviser: “You mean to tell me that the success of the economic program and my re-election hinges on the Federal Reserve and a bunch of f—ing bond traders?”)

Since then, several things have changed. Central banks have gotten more powerful because declining inflation gave them more flexibility to raise and lower rates to stimulate growth, and their perceived success in averting crises gave them a broader mandate. Meanwhile, the macro market has gotten more competitive: There are more pure macro funds, and the banks and businesses that took the other side of their trades have gotten more sophisticated. Today, macro funds try to eke out modest gains instead of betting on the rise and fall of nations.

The endgame for Bitcoin as a reserve asset is that it has a place on central banks’ balance sheets, like gold and the Swiss Franc.

But their trading style remains intact. Paul Tudor Jones’ approach is well documented in interviews, including the classic documentary Trader. Jones’ approach boils down to two things: understanding fundamentals and believing prices. A purist might focus entirely on building the fundamental argument for why a given asset is a good purchase – looking at a company’s earnings growth and competitive position, or judging a currency based on its government’s fiscal and monetary policy. A pure speculator typically makes decisions entirely based on price action, ignoring the underlying reason. Jones’ approach synthesizes these: He assumes prices move for a reason, and that if you understand the reason you can accurately predict the rest of the move.

In bitcoin’s case, Jones starts with the premise that the money supply has massively increased but the supply of goods and services has declined. As he put it in his investment memo: “A large demand shortfall will prevent goods and services inflation from rising in the short term. The question is whether that will be the case in the long term with a central bank whose central focus will be repairing the worst employment crisis since the Great Depression.” (Emphasis added.)

If demand can’t meet supply – there’s money in your pocket but you can’t take a vacation or go out to a fancy dinner – the money still has to go somewhere. In most recessions, that money finds its way into savings accounts (in 2007, the average savings rate as a percentage of disposable income was 3.7%. By 2012, it had more than doubled to 8.8%). But savers are rational, and when rates are low they’ll look for somewhere else to put their money. Jones considers several vehicles for savings: stocks and bonds, cash, gold, and bitcoin. He ranks them according to criteria such as trustworthiness, liquidity, purchasing power and portability. He concludes that, based on those criteria, bitcoin is fundamentally the least desirable of all the savings vehicles, just based on its intrinsic traits.

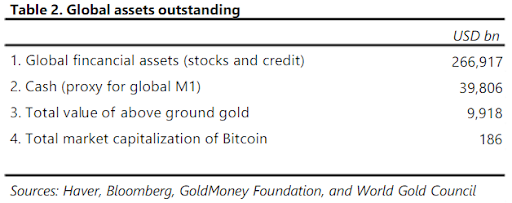

But that’s a value judgment; the other question is price. And on price, bitcoin is the winner; its value is under 2% of gold’s and less than 0.1% of the value of all financial assets.

So after careful due diligence, the famous trend-chasing macro investor ultimately treated bitcoin as a value play.

That’s not as crazy as it sounds. Currencies are always odd assets because their value is a self-fulfilling prophecy: A dollar is worth a dollar because people treat it as being worth a dollar, and people treat it as being worth a dollar because other people do. This makes every currency by its nature a slow-motion momentum trade (with a vicious unwind when the country loses control of its currency). On most of the traits that matter for currencies – stability and liquidity – bitcoin scores poorly. But the higher its value, the better it looks.

Since a working currency is a slow-motion speculation and a new cryptocurrency is a hyperactive speculative asset, it makes sense to think of the progress a currency makes as a process of rising in value and slowing down in volatility. And one way that happens – the way it has to happen – is that larger speculators with slightly longer time horizons accumulate positions. The endgame for bitcoin as a reserve asset is that it has a place on central banks’ balance sheets, like gold and the Swiss franc: In case of emergency, break open the cold wallet. And the intermediaries in that process are institutional investors.

Part of the way macro funds work is by keeping close tabs on the economy, and that means talking to academics and policymakers. Depending on your outlook this is either reasonable behavior – politicians consulting with relevant subject matter experts on complex topics – or it’s a conspiracy in which speculators make trades and then lean on the government to make those trades profitable. It’s probably a bit of both: Traders do have good information and can spend all of their time mentally stress testing an investment thesis. But they also have a strong incentive to talk their book.

A macro fund with a bitcoin position is one step closer to a central bank with the same kind of position. And while Jones’ $40 billion under management certainly sounds like a lot of money, it’s a tiny amount compared to central bank balance sheets.

It’s important not to get too fixated on any one trader, of course. Jones says he actually owned bitcoin personally back in 2017 when he played the bubble and sold out near the top. “It is amazing how well one can trade when there is no leverage, no performance pressure and no greed to intrude upon rational reflection! When it doesn’t count, we are all geniuses,” he says. (That’s right: 2020 is so weird you just learned a billionaire hedge fund manager is jealous of your trading opportunities.) Given short-term performance requirements and high leverage, a hedge fund is a naturally weak hand in the market.

But it’s a good sign that more funds are looking at, and acting on, the bitcoin opportunity. As Jones puts it in his letter to investors: “Something appears wrong here and my guess is it is the price of bitcoin.” He closes more ominously: “One thing is for sure, these are going to be incredibly interesting times.” Indeed.

Disclosure Read More

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.