One of the Founding Fathers of the United States, Benjamin Franklin, once said: “But in this world, nothing can be said to be certain, except death and taxes.” While this phrase was realized in 1789, the same still holds true today. The only difference is that taxes are slowly but surely catching up with crypto assets.

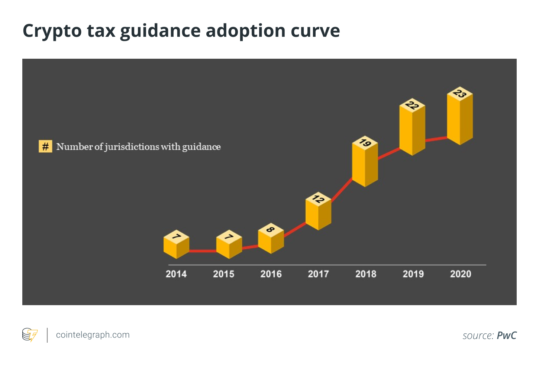

Therefore, it shouldn’t come as a surprise that Big Four accounting firm PricewaterhouseCoopers has just released its first annual Crypto Tax Index as part of the “Global Crypto Tax Report.” The detailed report contains the latest global crypto tax developments, along with crypto tax information for over 30 jurisdictions. Interestingly, 61% of jurisdictions surveyed have issued guidance on the calculation of crypto capital gains and losses for individuals and businesses.

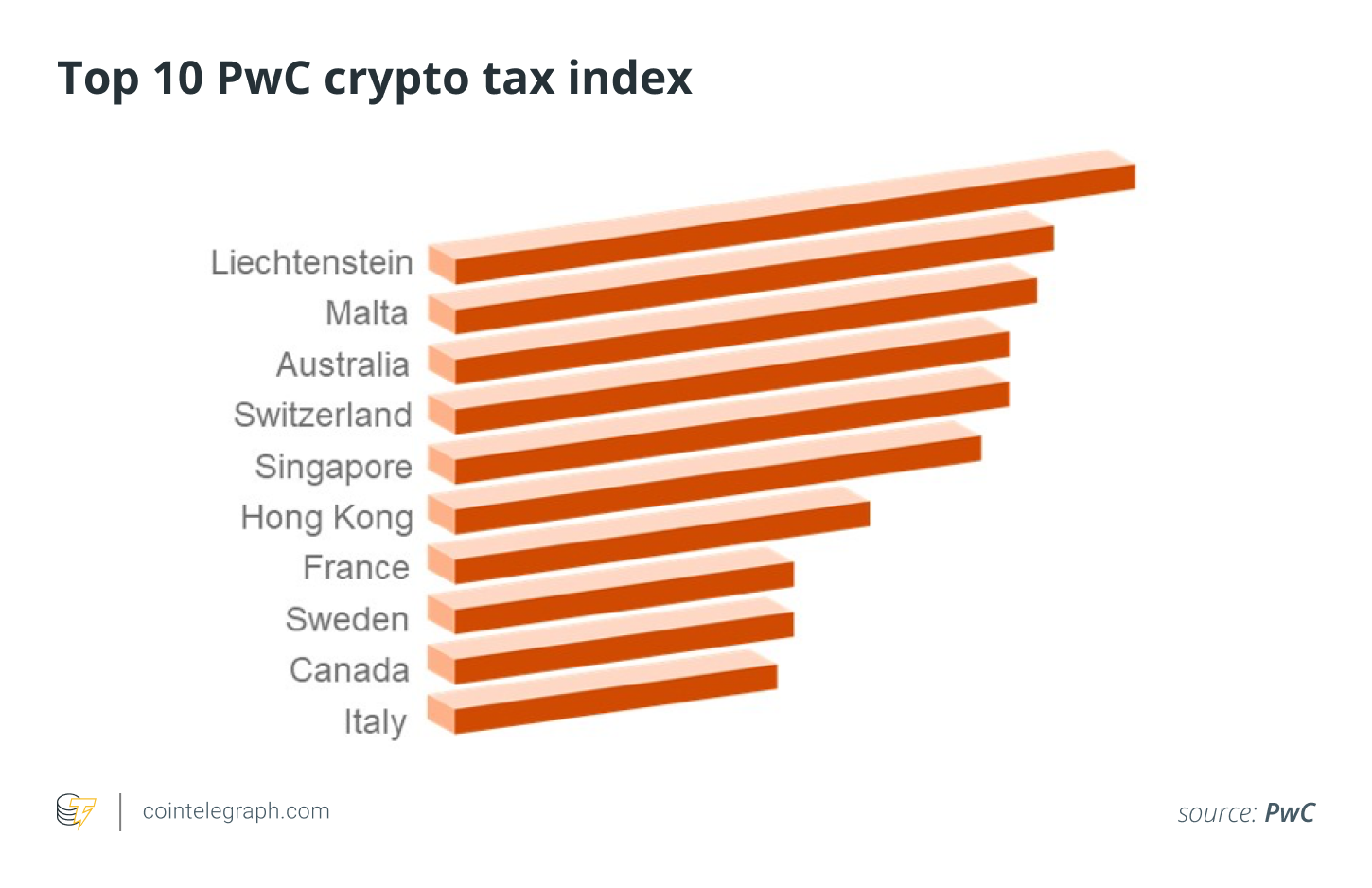

The survey’s Crypto Tax Index ranks jurisdictions based on the comprehensive structure of their tax guidance. The report shows that the tiny yet innovative European country of Liechtenstein tops this year’s rankings, closely followed by Malta and Australia.

Crypto assets are finally taken seriously

Peter Brewin, a tax partner at PwC Hong Kong and a report contributor, told Cointelegraph that the industry is finally starting to see more activity by some of the supranational policy setters like the Organization for Economic Co-operation and Development. As a result, tax authorities have been showing an increasing interest in crypto assets, but these guidelines are dated:

“What our research shows is that the guidance issued by many tax authorities is already getting dated. Yes, it is important that people know how to account for tax on the trading of Bitcoin and other cryptocurrencies, but that is really crypto tax 101.”

Although basic guidelines have been established on how to tax common crypto assets, Brewin points out that loopholes remain. “What we really need, and which is lacking in nearly all jurisdictions, is principles-based guidance that is fit for the new decentralized economy,” he said.

That being said, one key takeaway from the report is that no jurisdiction has issued guidance yet on topics that are shaping the future of an economy built around digital assets. For instance, there are no taxation guidelines when it comes to crypto borrowing and lending, decentralized finance, nonfungible tokens, tokenized assets and staking income.

This is alarming, considering the recent rise of DeFi and billions of dollars are being locked in DeFi contracts, as criminals may exploit the hype. While impressive, the PwC report highlights that without guidance, innovative companies and startups will be faced with significant tax uncertainty, especially in regards to cross-border activities.

The document provides some recommendations; for example, when it comes to the taxation of DeFi, it’s mentioned that this should include how income from the DeFi platform is taxed at the recipient level and whether jurisdictions may seek to tax payments at the source. This is similar to how withholding taxes are commonly applied to interest payments in traditional finance.

The report also takes into account the crypto industry’s ever-changing ecosystem, therefore, noting that future guidance should be principles-based and not overly prescriptive.

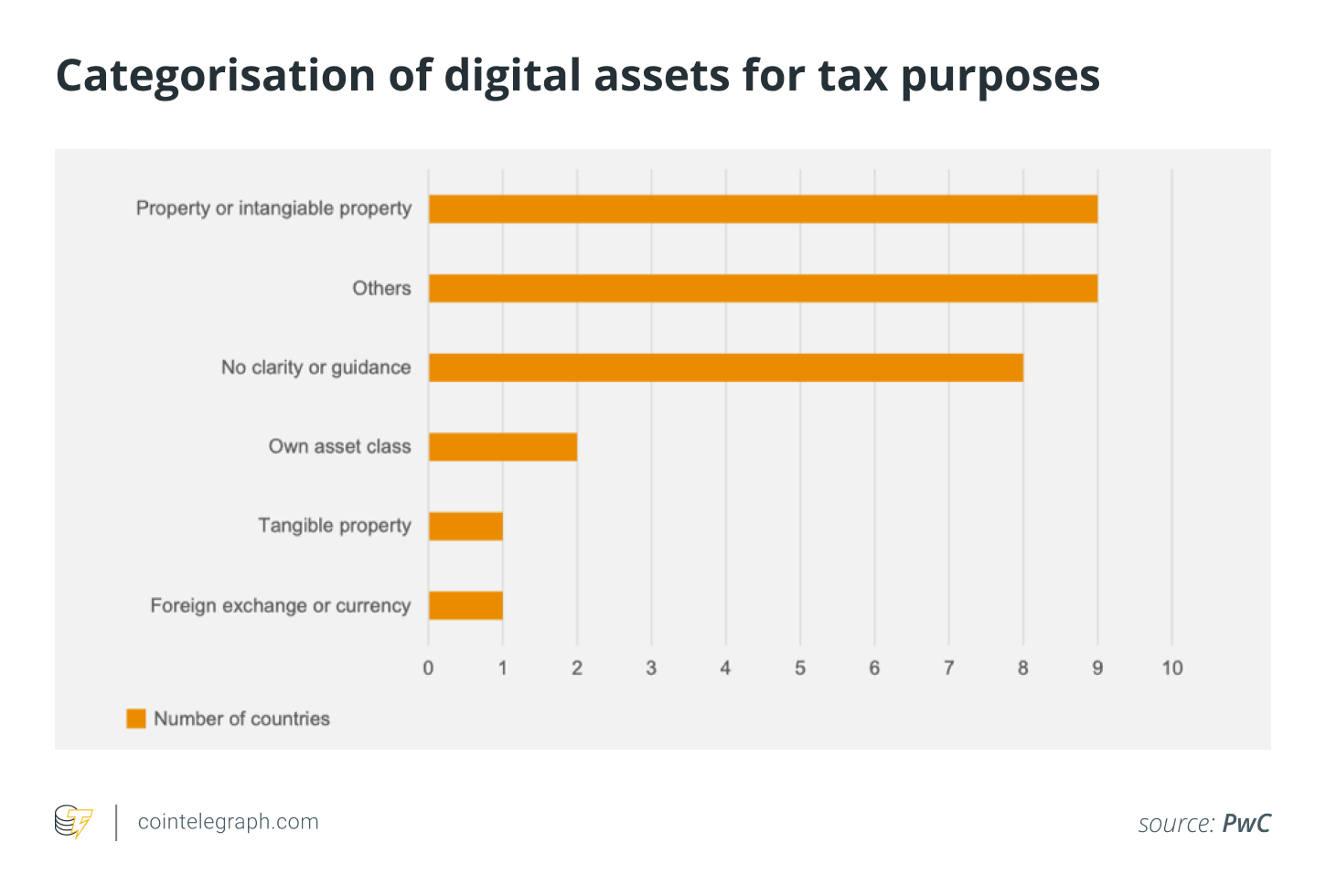

Crypto still primarily viewed as property

Another important finding in the report is that most jurisdictions view cryptocurrencies as a form of property from a tax perspective. In fact, very few consider digital assets as currency for taxation purposes. The report notes that this is because the disposal of property is considered similar to a barter transaction; therefore, results in a gain or loss could be subject to tax.

Yet this isn’t the case in all jurisdictions. For instance, countries such as Israel are starting to propose that Bitcoin should be taxed as a currency. If this proposal becomes a law, digital currencies such as Bitcoin (BTC) could be taxed at a lower rate in Israel than those currently in place.

Although, having cryptocurrencies taxed as a currency could also result in challenges. The report points out that a tax change could potentially be triggered each time an individual spends a digital asset. This is problematic because many consumers are not able to calculate their gains or losses from each of their daily transactions. This is generally not the case with fiat but could be if cryptocurrencies were to be used, resulting in another barrier to mass adoption.

Tax uncertainty will create challenges

Overall, PwC’s crypto tax report shows that while significant work has been done to provide guidance for the taxation of digital assets, the industry is not up-to-date with recent developments. In turn, businesses will continue to be faced with tax uncertainty, creating further challenges for adoption and innovation.

While this may be, authorities are aware of the fact that new crypto taxation guidelines are needed. Mazhar Wani, fintech leader at PwC U.S., told Cointelegraph that while it’s tough to estimate when official guidance will be issued in regards to topics like DeFi and staking, these points are being discussed by global tax authorities. “The OECD is also looking at many of these points since it falls within their broader initiatives, so we hope to see something soon,” he said. However, Brewin points out that when it comes to DeFi, taxation clarity could take much longer:

“Particularly when you have a fully decentralized platform, it’s not clear to me that approach will work, given that you are dealing with a completely different animal. We’ve not really seen a parallel for this when it comes to tax.”

Although this may be, Brewin suggests that today’s challenges can be overcome if the industry continues to work with policymakers to ensure that they understand the complexity and ever-changing nature of the crypto industry.