Today Bitcoin (BTC) price blasted through the $20,000 level and in the process, a record $7.9 billion in futures open interest was set.

Although the price increased by 74% over the past two months, the total accumulated short-seller liquidations amounted to $4.3 billion, which is lower than the $4.8 billion from longs.

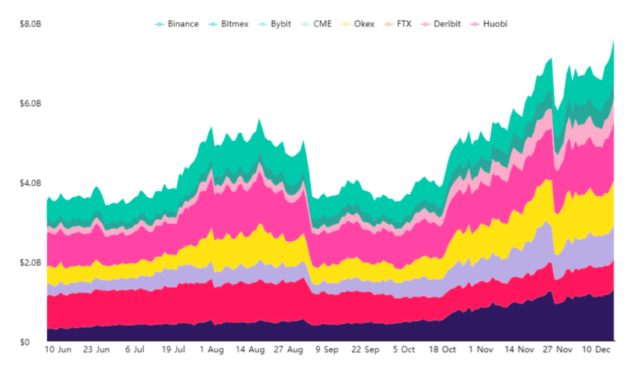

BTC futures aggregate open interest. Source: Bybt.com

As shown in the chart above, the futures aggregate open interest increased by 90% over the past two months. Thus, signaling that investors are increasing their positions, which in turn allows even larger players to participate.

It is also worth noting that the Chicago Mercantile Exchange (CME) now holds over $1.3 billion of these contracts, indisputable evidence of the growing institutional participation in BTC markets.

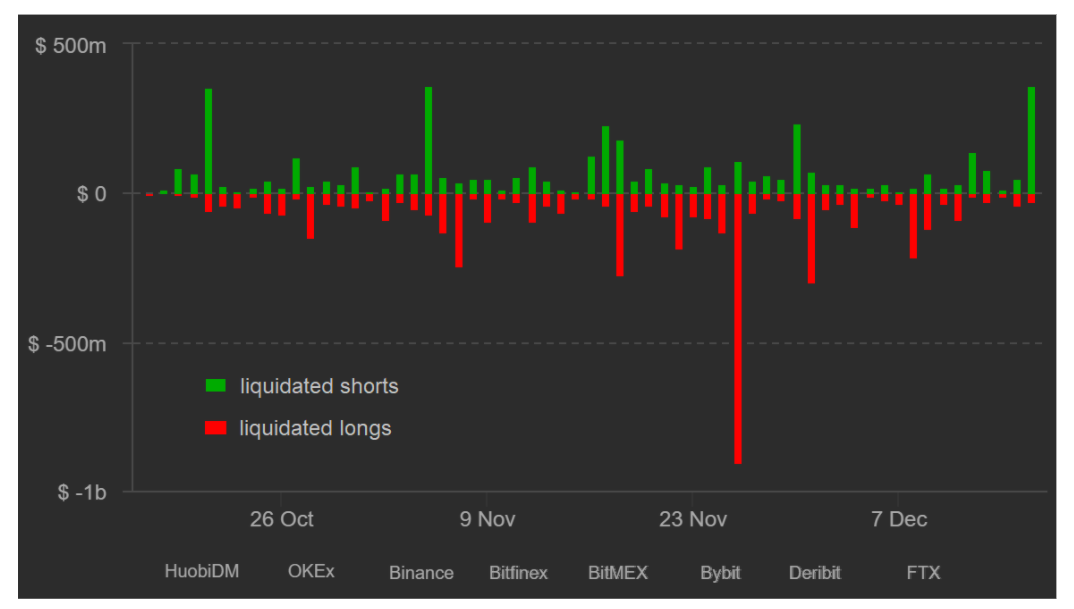

By looking at daily liquidations, investors can better assess how traders have been using leverage. Unexpected price swings will tend to cause higher liquidations than those ongoing trends, such as the recent Bitcoin breakout to $20,800.

Take notice of the largest candle represents longs getting their positions forcefully terminated on Nov. 26 as BTC price dropped 14.4% in 12 hours. Today’s $20,000 resistance break caused $365 million worth of shorts to liquidate, but this is still no match to the previous month’s $902 million bearish movement.

Volume failed to keep up with the new BTC price high

The recent volume downtrend is another reason for bears to celebrate. Bitcoin’s non-adjusted total trading volume decreased by 40% over the last three weeks.

Total cryptocurrencies daily volume, USD. Source: TradingView

Bitcoin’s daily average trading volume on spot exchanges reached $45 billion in late November and has since declined to $25 billion. While there is the possibility that exchanges may have inflated their volumes, there could also be some bearish maneuvers in play.

Nevertheless, a similar 40% decline occurred at Coinbase’s BTC/USD and Binance BTC/USDT markets. Therefore, bears might hope that such volume weakness indicates a lack of confidence in $20,000 turning into a support level.

Perpetual futures reflect excessive leverage

Perpetual contracts, also known as inverse swaps, have an embedded rate usually charged every eight hours. Even though both buyers and sellers’ open interest is matched at all times, their leverage can vary.

When buyers (longs) are the ones demanding more leverage, the funding rate turns positive. Therefore, the buyers will be the ones paying up the fees.

Sustained funding rates above 4% per week translate to extreme optimism. This level is acceptable during market rallies but problematic if the BTC price is sideways. A high carry cost might force longs (buyers) to reduce their positions, therefore increasing sell pressure.

In situations like these, high leverage from buyers increases because of the increased risk that large liquidations will occur on surprise price drops.

Thus, bears might be holding their cards close to their chest, awaiting the best moment to test the market.

It’s possible that this could either happen closer to the Dec. 25 futures and options expiry or during weekends when order books are usually thinner.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.