- Strong demand for homes suggests the market is strong.

- Several factors have the potential to bring the housing market crashing down.

- A significant factor moving forward will be affordability.

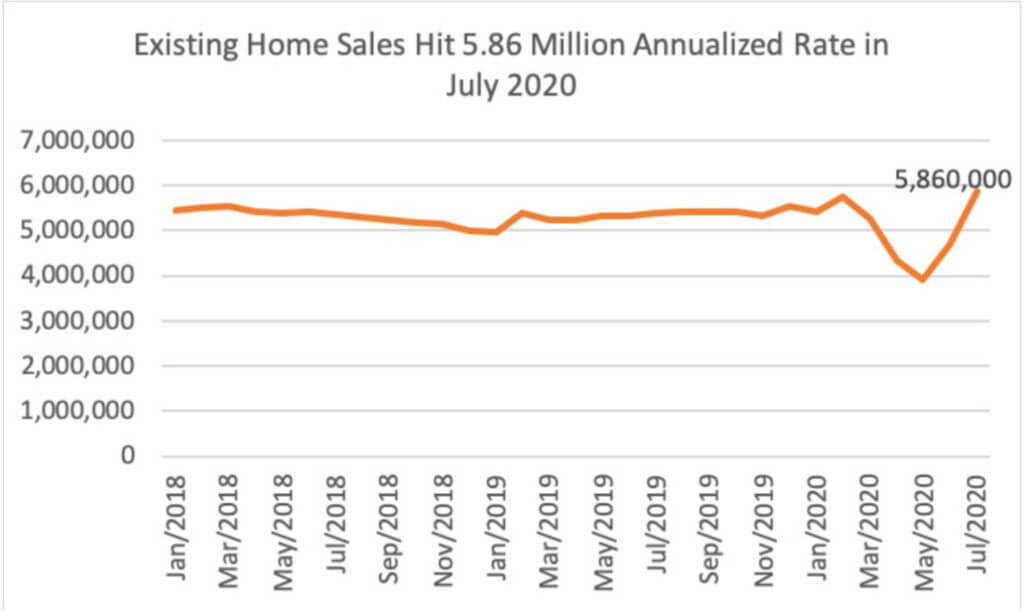

Bears have been predicting an impending housing market crash for some time, and the pandemic seemed to be the perfect catalyst for a downward spiral. But another strong month of rising existing home sales suggests the U.S. housing market might make it through the coronavirus crisis unscathed.

It makes sense that people are rushing out to buy houses. After being stuck inside for a month, many are heading out of densely populated cities in search of more space.

On top of that, you have thousands of workers with a flexible work-from-home scheme that allows them to live further from the office. Some are probably looking to up their square footage to set up a home office.

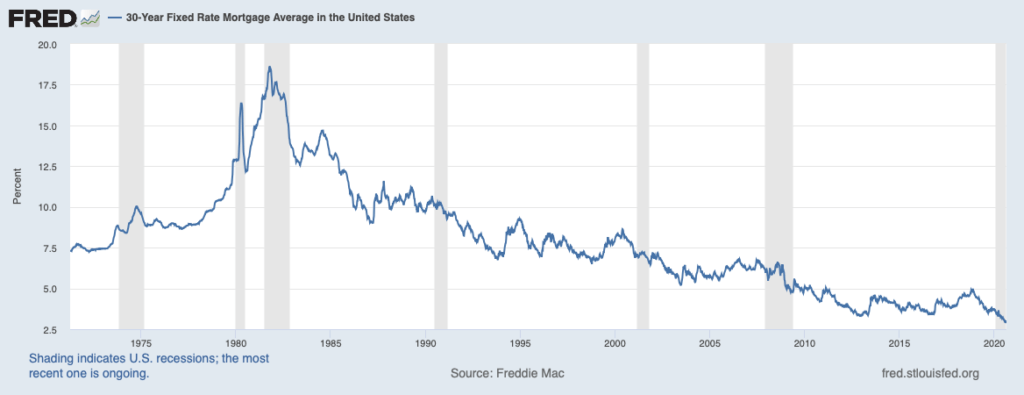

Ultra-low mortgage rates have helped accelerate demand for suburban homes as families upsize using cheap borrowed cash. Bulls contend that with mortgage rates settled below 4% for the foreseeable future, the housing market is on solid footing.

But not everyone holds that view. Others, who lived through the previous housing boom and bust say this sudden acceleration in demand feels eerily familiar.

Ed Pinto, the director of the housing center at the American Enterprise Institute, worries that policymakers have only delayed the inevitable with their generous coronavirus support programs.

We’ve delayed the crash, but at the same time we’re inflating the boom

Housing Bust Catalysts

In a perfect world, the strong demand would hold up through the rest of the year. But there are still several significant downside catalysts hanging over the housing market.

Many Americans appear to be taking advantage of low mortgage rates to acquire more space. Anecdotal evidence suggests that some of the demand is coming from first-time buyers who are escaping high-rent costs and densely packed towns. They’re using Federal Housing Administration loans, which require small down payments.

A spike in demand among first-time buyers hoping to get into the suburbs has been met by enthusiasm from developers, who are keen to capitalize on this new wave of eager buyers. But Homebuilder Jimmi Previti, whose business is one of the few to survive the 2008 housing crisis, says demand feels “frothy.”

Is this the little runup before everything runs off the rails? Nobody can tell.

Housing Market Risks

Previti’s experience isn’t the only red flag for the U.S. housing market. Affordability is another crucial aspect that could bring the housing market’s ascent to a grinding halt. Even before coronavirus hit, many questioned how much longer house prices could continue to rise without wages making a significant advance.

That’s even more concerning now, as many workers have their hours cut or are laid off entirely. The government’s added unemployment insurance is tapering off, a move that could see a wave of foreclosures in 2021. For now, those struggling to make ends meet amid the pandemic are allowed to postpone mortgage payments, but like unemployment benefits, that program will end eventually.

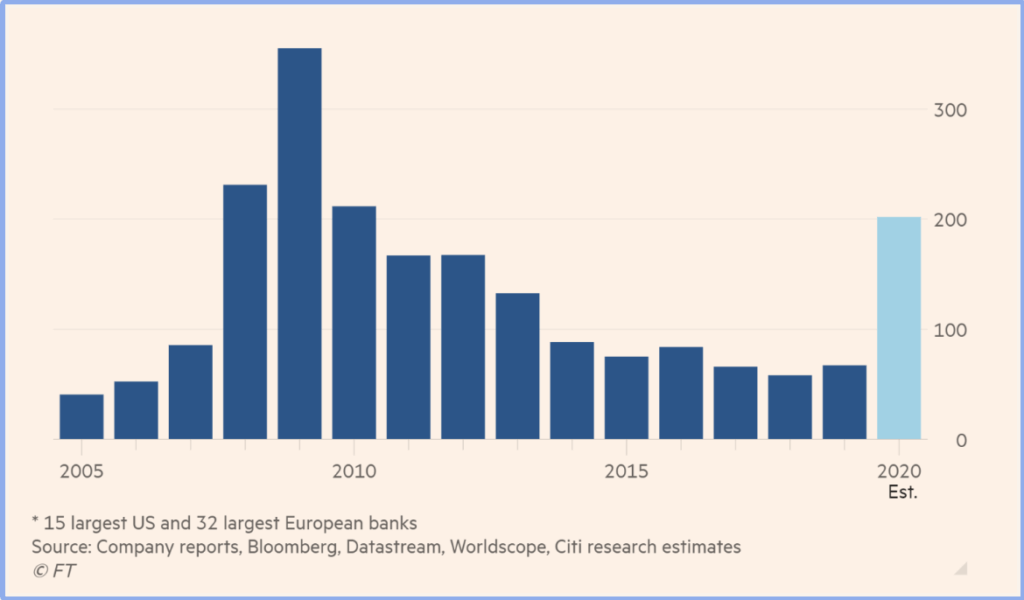

Banks have already started shoring up their balance sheets to cope with a wave of defaults. U.S. financial institutions have already put aside $76 billion to cover bad debts—a telling sign of what’s to come in the housing market.

The Bottom Line

Can the housing market survive a pandemic? The recent data suggest the answer is yes. But as with everything else in the economy at this point—only time will tell. With Americans staring over an income cliff and house purchases on the rise, the housing market is starting to look very frothy.

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com and should not be considered investment or trading advice from CCN.com.