There has been no shortage of epoch-changing twists so far this year. I mean, seriously, take your pick: even aside from the pandemic, we have riots on the streets of American cities, an alarming trade war, negative oil prices and gold briefly above $2,000/oz. These are just some of the loud, headline-grabbing changes that were once unthinkable but now form part of our new normal.

A much quieter shift, but equally transformative, started to make its presence more felt on Thursday, when the Chairman of the U.S. Federal Reserve, Jerome Powell, outlined a new focus for the institution: inflation will be allowed to run higher than the original 2% target “for some time” to make up for undershoots. In other words, inflation might rise in the short term, but don’t worry, we won’t raise rates.

You’re reading Crypto Long & Short, a newsletter that looks closely at the forces driving cryptocurrency markets. Authored by CryptoX’s head of research, Noelle Acheson, it goes out every Sunday and offers a recap of the week – with insights and analysis – from a professional investor’s point of view. You can subscribe here.

At first, the announcement seemed totally “meh” – the only surprise was that his remarks were not more remarkable. Given the colossal government debt, no one expected rates to be raised in the near future, no matter what inflation does.

But zooming out, Powell’s comments cement a radical shift in the role of arguably the most powerful central bank in the world. This is likely to influence more than just yield expectations: it could trigger a greater transformation of the Fed’s role.

This will, directly and indirectly, support the work going on in crypto markets. But more on that in a minute.

Origins

First, let’s look at a bit of history.

The founding Federal Reserve Act of 1913 did not specify any macroeconomic goals – the institution’s original mandate was to provide liquidity in order to avoid financial panics. The 1946 Employment Act shifted the focus to “maximum employment,” and in 1978 a new Act added a parallel goal of “reasonable price stability.” After a decades-long drift towards focusing on that at the expense of everything else, the financial crisis of 2008 jolted the Federal Reserve into again prioritizing financial stability.

That role gave it plenty of leeway as the current crisis started to unfold, and let it move into new areas that highlight its false independence. This could become increasingly significant given what Chairman Powell himself has recognized as a weakening faith in large institutions.

With the buying of corporate debt, the Fed is no longer just limiting itself to the printing of money – it is now deciding where the money goes. This is political. And with initiatives such as the Main Street Lending program, it is opening itself up to an almost inevitable wave of defaults that the taxpayer will have to fund.

And that’s even before you consider the pain that a higher inflation rate will unleash on a public reeling from unemployment and foreclosures. The “average” target of 2% may not sound like much, but anyone who has been grocery shopping recently knows that the reported headline increases are meaningless to daily life in a pandemic. The Fed is effectively telling them that the whopping 10% reported annual CPI increase in July for meat, the over 8% increase in the price of eggs and the over 4% increase for vegetables (to choose just some examples) aren’t important.

We’re taught that the Fed is independent from the government, which gives it the power to focus on the economy without political interference. But its increasingly embedded relationship with the Treasury is turning the central bank into more of a political arm. Its head is a political appointee. And its powers come from Congress, which responds to voters, who could conceivably convince Congress to make some adjustments.

Let’s not forget that the U.S. Federal Reserve was created just over 100 years ago – the institution is not that old, in the grand arc of history. And its influence is not written in stone. For now, its role is significant and even essential as the global economy recalibrates debt and affiliations. But things change.

In place

Where do crypto markets come into this?

Crypto markets were born in a storm of change. In 2009, the year of the first bitcoin transaction, the role of the central bank was going through another profound transformation. The roiling markets were handing out unwelcome lessons in the hubris of assuming trends were constant and systemic institutions were immutable.

Just over 10 years later, we’re in a similar situation. What we knew to be true about finance and markets is now riddled with doubt. What we assumed just couldn’t be, now is. And the central banks that we understood to be the gatekeepers to the global economy, are struggling to define their place in a rapidly evolving chaos and rebirth.

Those of us working in this industry watch indicators of a new reality pop up almost weekly. Over the past few days, we saw a blockchain-based security token initiate an IPO with SEC approval, a long-standing and well-respected financial institution get involved in the launch of a crypto fund, and a state-owned energy giant partner to reduce flaring from operations through bitcoin mining.

These big steps forward take their place in the march towards the profound change that everyone working in crypto has been preparing for. Whatever our role, we are working on what we think comes next in the cogs of progress. Chairman Powell’s remarks this week reminded us that so are central bankers.

Progress is not just the realm of new technologies and business models, and change is not just about replacing traditional institutions with new ones. Everything evolves.

If 2020 teaches us one thing, it has to be that assumptions don’t last, and that we all need to be flexible. In a world where everything is undergoing a transformation, barriers come down faster. And, as uncomfortable as it may be, change is always an opportunity, especially when it comes from unexpected areas. In our industry, it’s what we’ve been hoping for.

The SEC is changing, too

Central banks aren’t the only venerable institution implementing profound policy changes that will impact crypto markets.

Earlier this week the U.S. Securities and Exchange Commission (SEC) approved the plan for the NYSE to allow companies to list newly issued shares directly, rather than via an IPO. Previously, direct listings were allowed for shares already held by insiders. This new ruling will enable companies to raise capital on public markets without the expense of an IPO, while still meeting certain compliance rules.

This is potentially a big deal for crypto markets, since a handful of well-known companies in our industry have been rumored to be contemplating a public listing. Going the direct route will make this a lighter lift for blockchain startups, give investors a regulated exposure to the crypto markets, raise the profile of the industry as a whole and give us analysts insight into the inner workings of previously opaque businesses.

The SEC also broadened its definition of “accredited investor,” for the first time in 40 years, to include those that had passed the Series 7, 65 and 82 exams, regardless of their personal wealth. As a CFA, I am miffed that CFAs aren’t included (what, are we not smart enough?), but I’m taking the glass-half-full approach of focusing on the fact that change is happening, albeit slowly on some fronts.

A much more significant move is the launch of the first SEC-approved security token listing. INX, a Gibraltar-based company building a crypto exchange, is issuing 130 million tokens that allow holders to receive a share in the company’s net cash flow, as well as trading discounts. The offering price is $0.90, which could net the company $117 million, making it the largest IPO in the industry to date.

That in itself is pretty cool, but let’s not forget that it’s a security token. It runs on the Ethereum blockchain. And it’s been approved for public trading – even for retail investors – by the SEC.

Whether the business fundamentals hold up to scrutiny or not, the issue is a phenomenal innovation, and not just because the token itself will blur traditional understanding of tradable assets. As it stands, it’s similar to equity in that holders can share in the business’ success, but without ownership rights. And it could confer operational privileges such as discounts, and possibly other features down the road, because it’s a programmable asset. What’s more, it can only be held by investors that have passed through the KYC process.

It’s also a big step forward for a regulator traditionally wary of blockchain-based offerings, one better known for its punitive decisions and high access barriers than its support for new assets and business models.

Anyone know what’s going on yet?

Although bond yields edged up in response to the Fed’s new inflation stance, the dollar hardly reacted, and even bitcoin’s and gold’s wobbles left them pretty much where they were before Powell’s remarks.

The S&P 500 hit a record high this week, having bounced back over 50% from its 2020 low in March. While gold has not managed to break its all-time high of $2,061 from earlier this month, it is still over 30% up from its March lows. For comparison, bitcoin’s price is nowhere near its all-time high, but it is almost 3x its intraday low on March 12.

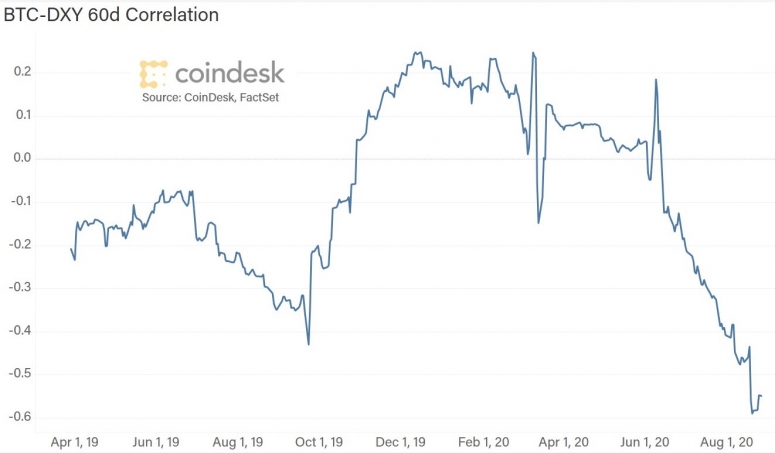

The correlation between gold and bitcoin continues to increase, as both are yet again acting as hedges against the dollar.

Speaking of which, the correlation between bitcoin and the dollar continues to head downwards.

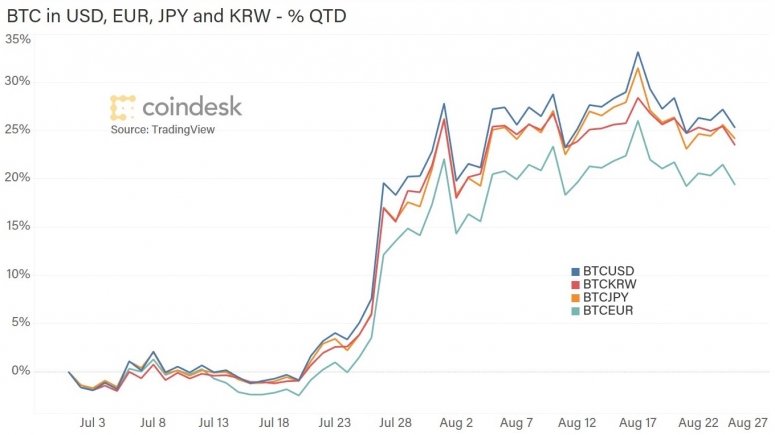

Just through pure math, a declining dollar will boost the bitcoin price denominated in dollars. But what about bitcoin in other currencies? Understandably, the performance is not as high, but it is still strong.

CHAIN LINKS

A filing with the SEC this week revealed that Peter Jubber, head of strategy and planning for Fidelity Investments, is the president of FD Funds GP, which is the general partner of Wise Origin Bitcoin Index Fund I, LP. TAKEAWAY: While Fidelity has not confirmed this, signs point to the fund being a Fidelity initiative, which would mean that one of the largest asset managers in the world, with almost 75 years of history, is launching a crypto fund. Let that sink in.

Blockchain investment firm Digital Currency Group (parent of CryptoX) has expanded into the bitcoin mining industry with a subsidiary called Foundry which provides cryptocurrency miners and equipment makers with financing and market intelligence. TAKEAWAY: This is yet another sign that the cryptocurrency mining industry is rapidly maturing, which should bring new investment, greater geographical diversification and innovative market products that should add liquidity and resilience to an integral part of the ecosystem.

And speaking of a changing crypto mining industry, listed multinational petroleum giant Equinor (formerly Statoil, 67% owned by the Norwegian government) is moving to significantly reduce natural gas flaring by mining cryptocurrency, according to screenshots from Equinor’s intranet received by Arcane Research Friday. TAKEAWAY: The firm will apparently do this via a partnership with Colorado-based Crusoe Energy Systems, which uses digital flare mitigation technology to convert waste natural gas that would be otherwise released into the atmosphere into electricity at the well site that can mine cryptocurrency at low cost.

Nasdaq-listed cryptocurrency mining company Marathon Patent Group has signed a letter of intent to acquire the mining-as-a-service company Fastblock Mining in an all-stock deal. After deploying Fastblock’s 3,304 ASIC miners, Marathon’s mining power will increase by 208 petahash per second, and its overall cost to mine bitcoin will drop from $7,400 per BTC to $3,600 per BTC due to Fastblock’s low electricity cost. TAKEAWAY: Lower mining costs not only give the operation a good cushion should the bitcoin price fall, but they also afford it considerable upside if the bitcoin price rallies. While listed companies generally have company risk on top of market risk, they can provide an alternative way to gain exposure to crypto prices for investors that don’t want to bother with crypto exchanges and custody.

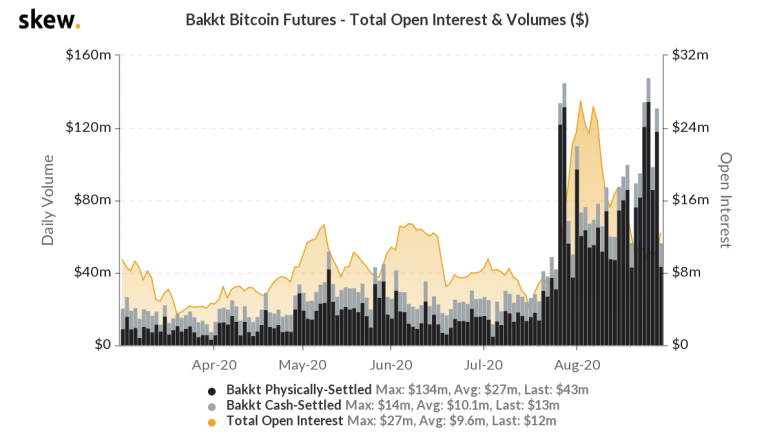

The average daily volume of physically settled bitcoin derivatives on Bakkt, a U.S.-based crypto derivatives exchange backed by the parent of the NYSE, has reached record levels this month, signaling growing institutional interest in spot bitcoin transactions. TAKEAWAY: Bakkt’s futures with physical delivery allow investors to take ownership of bitcoin via a regulated exchange. Spot exchanges may be licensed, but they are not regulated since spot crypto does not yet have a regulator. Derivatives do. And many institutions are limited to transacting on regulated venues.

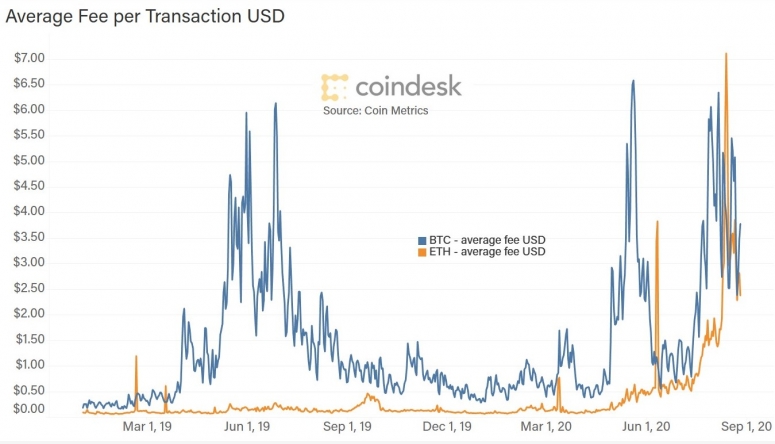

Nic Carter looks at the protocol architecture of Bitcoin and Ethereum, and the role of fees in each. TAKEAWAY: This is especially relevant given the soaring fees on Ethereum, which throws into question its goal to be a widespread, high-throughput application platform (although the upcoming shift to Eth 2.0 aims to support this). Bitcoin’s relatively high fees also have a role in shaping its narrative (more store-of-value than decentralized payment system) and technological development (sidechains and lighter data structures).

Antigua and Barbuda-based crypto exchange FTX has launched a futures index for the top 100 liquidity pools on Uniswap, the largest decentralized exchange by traded volume. And Binance, the world’s largest crypto exchange by volume, plans to offer fully synthetic derivatives based on a decentralized finance index. TAKEAWAY: You’ve heard me say this before: the innovation in terms of new types of assets in crypto markets is phenomenal. Here you have products that allows traders to use centralized crypto exchanges to access the performance of markets native to decentralized platforms, with leverage.

Ribbit Capital, an investor with a $2.6 billion portfolio of fintech startups including cryptocurrency and blockchain ventures (and a founding member of the Libra Association), filed a prospectus with the SEC for a $350 million IPO for a special-purpose acquisition company (SPAC) called Ribbit LEAP. TAKEAWAY: Ribbit LEAP does not yet have a business, but it intends to find one with which to merge, and could end up being an efficient public listing route for a crypto business looking to raise capital. As Nathaniel Whittemore explains in this great podcast episode, SPACs are not cheaper than IPOs, but they are more agile, which could become important if indeed we are heading into a bull market. In other words, with a SPAC, crypto businesses can raise funds faster, taking advantage of rising hype.

Podcast episodes worth listening to: