Recently, European central bank executives — Thomas Moser from Swiss National Bank and Martin Diehl from Deutsche Bundesbank — stated that central bank digital currencies don’t need a blockchain.

They expressed their opinions by saying that blockchains — especially public, or permissionless — make no sense for central bank digital currencies. The reason is that central banks are central parties; therefore, a blockchain, being a decentralized ledger, is not applicable. It is a pity, but the clerks seem to be unknowingly (or intentionally, who knows?) wrong in their conclusions to why and how blockchain technology can be used, especially with CBDCs.

There are two misconceptions widely spread in the general public. First, permissioned distributed ledger technologies are often erroneously called “a blockchain” because they have similar features. However, they are not fully decentralized, immutable and censorless, compared to permissionless blockchains (but we will not discuss this problem today).

The second is why we need blockchain technology and how it can be applied to real-world problems. It is time for the blockchain community to roll up its sleeves and start educating people, especially those who make decisions at state levels.

Any existing public blockchain can be used for a wide range of applications related to finance, property rights and copyrights, or anything that has an economic value and can be represented as a nonfungible token.

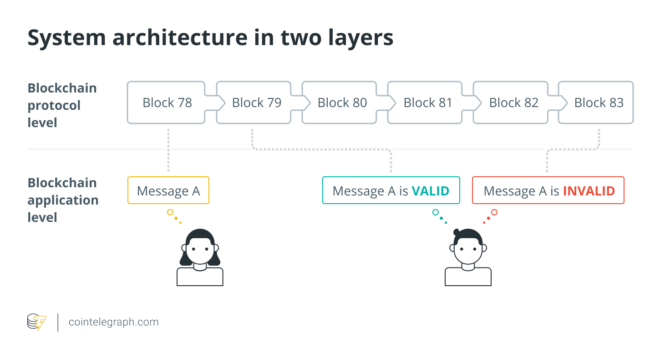

System architecture in two layers [Infographics]

First, there is the blockchain protocol with a cryptocurrency. At this level, we design nothing; we just accept it and use it as it is. It has all the necessary features to create the second layer: the application level and a transparent blockchain; it’s decentralized and immutable; it has its own cryptocurrency; and we can publish data on it.

Immutability and the ability to permanently store data, which users can insert in transactions, gave birth to everything we know beyond cryptocurrency: smart contracts, tokens, key-value entries and irrevocable records of arbitrary data. This is the application level. Here, we can design any interaction with any party, including central banks. And it absolutely does not contradict the nature of the technology because blockchain is a level of a decentralized public repository for transactions and data. With such a platform, both centralized banking and blockchain technology can coexist.

Let’s imagine a CBDC on a blockchain, for example, Bitcoin, Ethereum or any other ledger from the top 100 cryptocurrencies on CoinMarketCap (anything ranked lower should not be considered due to security concerns):

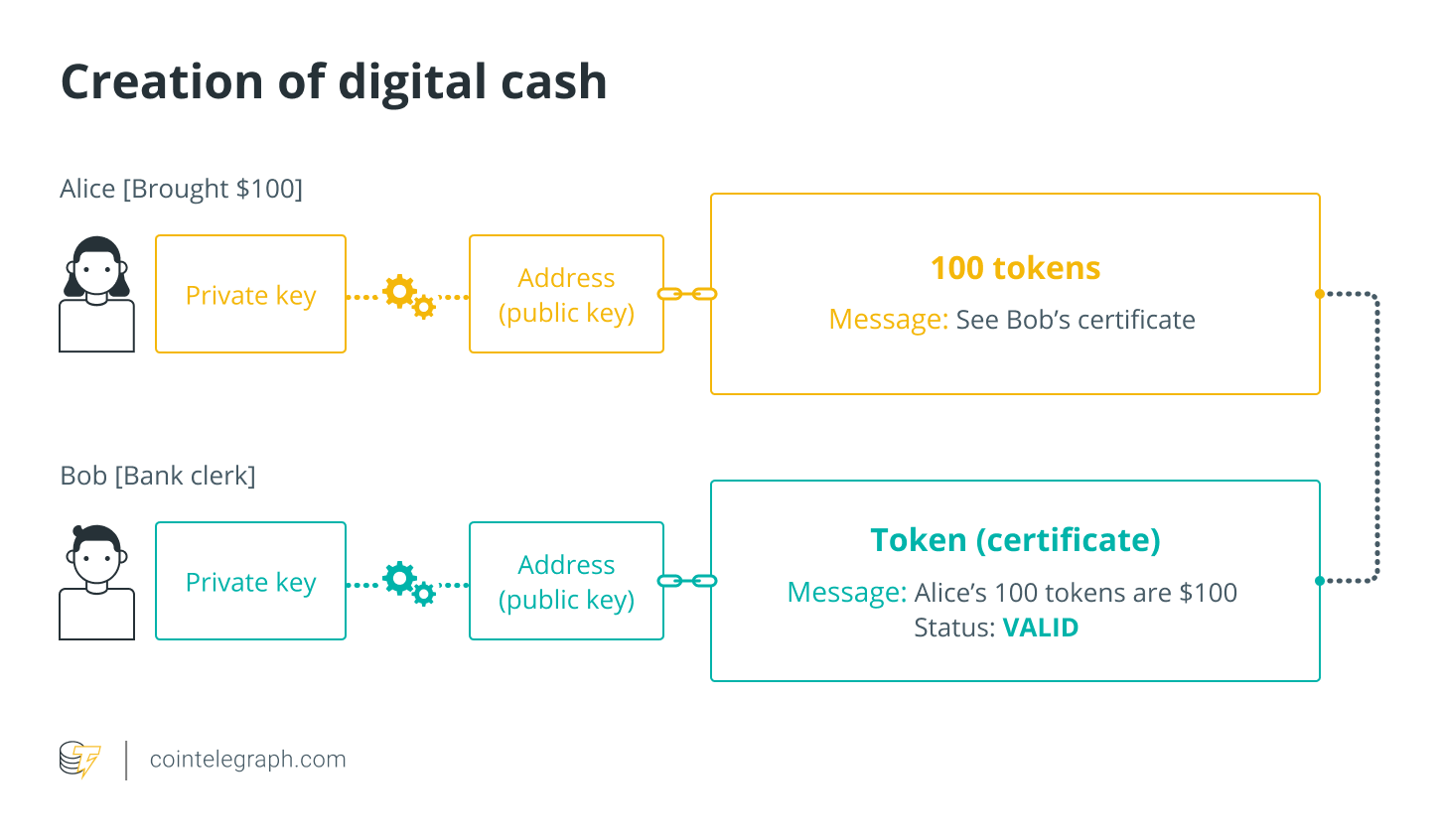

For example, Alice goes to a bank and gives a bag of cash, asking the clerk to issue tokens for the equivalent amount. Two transactions must happen on the blockchain. Alice creates her tokens (or colored coins), and in the transaction, she puts a reference to the bank’s transaction. The bank, in its transaction, confirms that Alice’s token represents money of that amount. Now, Alice has digital cash in her crypto wallet. She can exchange it into cryptocurrencies, other tokens, or buy anything else and use it as money as long as everybody trusts the bank. When other people go to the bank (or any other bank), they return previously acquired tokens in exchange for cash, which was first brought to the bank by Alice, and the tokens are then destroyed because they no longer represent value.

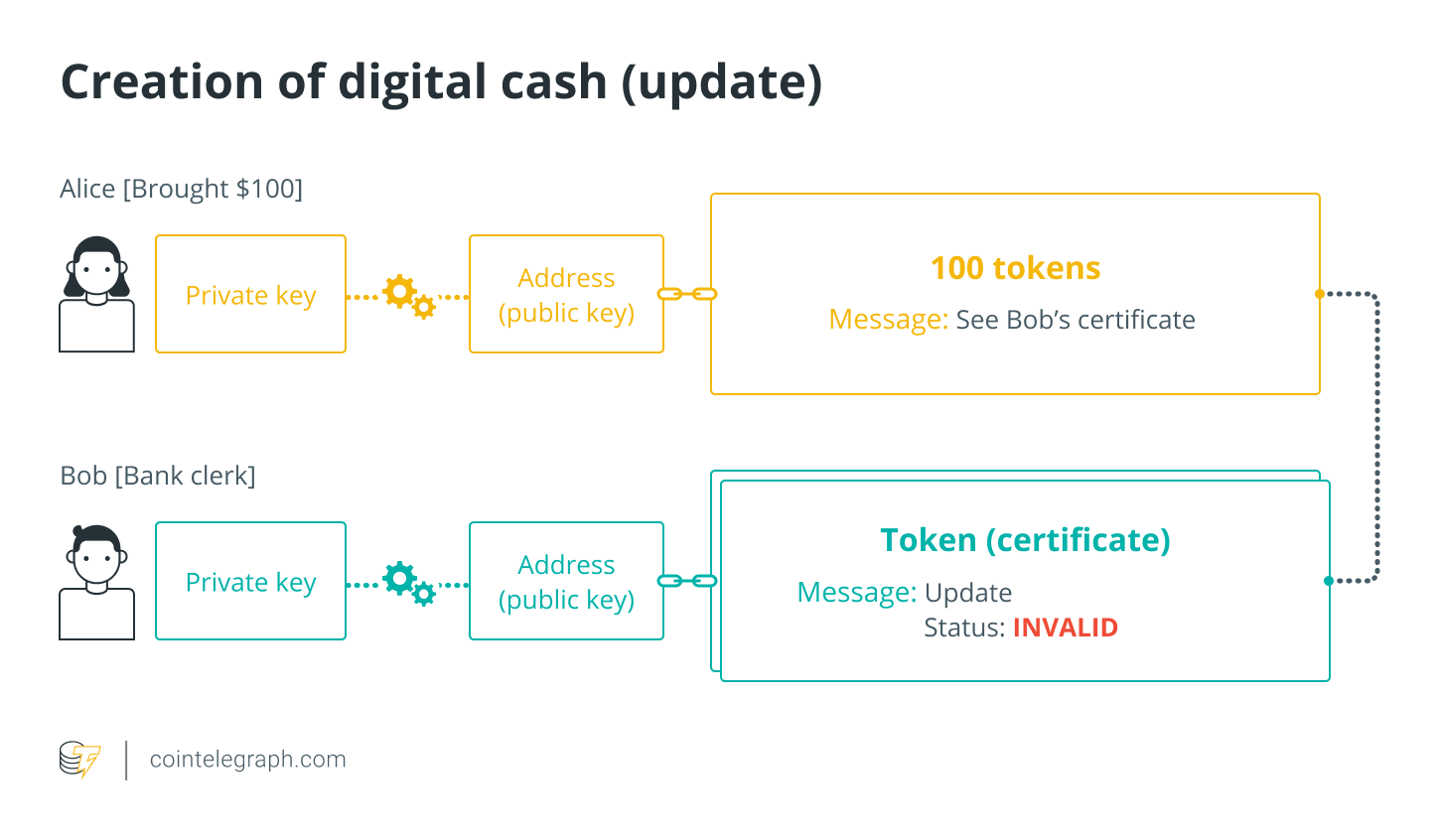

Why do we need the bank’s record? If Alice loses her private key, the bank will update its records and make it public that these tokens are no longer valid. The bank’s records are also needed to control money laundering and other unlawful activities. The tokens can be split and transferred many times to anyone. Here comes into play the rules: Know Your Customer, Anti-Money Laundering, counter-terrorism financing, etc. If Bob receives tokens from an unverified wallet and cannot prove the origin of the money, if there is a reason to believe that this money is involved in any illegal transaction, there will be no way he can cash it out. All transactions are transparent and traceable. The bank, through the prescribed lawful procedure, can trigger the transaction that will announce this money invalid. The coins will remain in Bob’s wallet, which he will still control, but they will turn into useless money.

Of course, this is a simplified scenario just to explain the general idea. The mature system will involve many elements: the cross-blockchain protocol to include many blockchains in the system to let users decide for themselves where they want to own their digital cash and transfer it from one blockchain to another. We will need another protocol layer of smart laws and digital authorities to publish patches to the banking protocol and to update the application level. We need this because in a situation where both private keys are lost — Alice’s and the bank’s — we need a third, which is the root address that belongs to the authorities in order to restore access or even to reset the whole system if something goes wrong.

But again, all this happens not in the blockchain protocol, but on the application level. We will also need to design protocols for digital identity and KYC, and it is better to look into the direction of new approaches: self-sovereign identity, decentralized identifiers and many other elements. And of course, instead of just having the bank and Alice involved, the central bank and the government must move in to interfere by applying their scenario.

Meanwhile, one thing remains the same. The blockchain that serves us as a pipeline to transfer value is, at the same time, an immutable repository as evidence of everything happening in the real world.

Conclusions

Through its native mechanism of transaction authentication by public and private key cryptography, blockchain technology allows users to perform transactions directly on a ledger, while in the centralized system, there is always a client-server architecture, and hence, a middleman; transactions are irrevocable and immutable, which no centralized technology is capable to ensure at a comparable level. Therefore, it is a reliable pipeline to transfer value.

Central banks and commercial banks perform multiple functions, and among them, blockchain technology can help to improve some of the most important ones to ensure a critical infrastructure.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Oleksii Konashevych is the author of Cross-Blockchain Protocol for Government Databases: The Technology for Public Registries and Smart Laws. He researched the use of blockchain technology for e-governance and e-democracy, and works on the tokenization of real estate titles, digital IDs, public registries and e-voting at the RMIT University. Oleksii co-authored a law on e-petitions in Ukraine, collaborating with the country’s presidential administration and serving as the manager of the nongovernmental e-Democracy Group from 2014 to 2016. In 2019, Oleksii participated in drafting a bill on Anti-Money Laundering and taxation for crypto assets in Ukraine.