As if the ructions of the year aren’t giving us enough cause to re-examine things we thought we understood, now we find ourselves questioning what a company is for, and what role it should occupy in society and in employees’ lives.

Earlier this week, Coinbase co-founder and CEO Brian Armstrong published a post in which he stressed the company’s focus on the mission of creating “an open financial system for the world,” and asked that political issues be left out of workplace discourse.

The questions this raises are huge, and the timing fits right into tectonic shifts already underway in the role of capitalism in our evolving society.

Let’s look at some of the questions, to which there are no clear answers.

- Armstrong says Coinbase has “an apolitical culture.” What does that even mean, in these times of growing polarization on practically everything? Even being apolitical can be taken as a political stance. What’s more, when a company whose mission is to bring “economic freedom to people all over the world” requests that activism and politics be left at the door, you get a glimpse of how institutionalized the crypto ethos is becoming.

- What is an employment contract? Some will answer that it is monetary compensation for certain output. Others will argue that you give up your time in exchange for payment. If the latter, can the organization paying you dictate what you do in that time?

- Does a company have the right to define its own mission? The answer might seem like an obvious yes, but an extension of that is, does a company have the right to ignore topics its employees care about? Here the issue gets more divisive.

- Related to the previous point, is a company’s responsibility to its shareholders or its employees? Armstrong believes that focus is core to achieving the mission, and that is what shareholders have a right to expect. But the success of intelligence-based businesses largely rests on the employees. We’re not talking about widget-producing factory floors here. This is an environment in which specialized talents and inspiration matter, and those are supplied by motivated people. So, some could argue that Armstrong’s responsibility is to his employees, because that will make the company more profitable and the shareholders happy.

There are many more, but I’m aware of pixel constraints.

As if to drive home the point, this week IBM released the results of its annual executive survey. Here’s an excerpt from the press release (my emphasis):

“Ongoing IBV [IBM’s Institute for Business Value] consumer research has shown that the expectations employees have of their employers have shifted amidst the pandemic – employees now expect that their employers will take an active role in supporting their physical and emotional health as well as the skills they need to work in new ways.”

This is at odds with a focus on the “mission,” whatever that mission may be. And it highlights the crucial role that employees play in a firm’s success. Also from the PR:

“Participating businesses are seeing more clearly the critical role people play in driving their ongoing transformation.”

This doesn’t come from some new-wave, millennial-driven, holistic social advocate. It comes from IBM, a standard bearer for legacy enterprise, and represents how much the concept of efficient management has changed.

Whether you agree or disagree with Armstrong’s position, you have to admit he was brave to wade into this, especially given the rumors of a planned public listing later this year.

Armstrong’s blog post is so much more than a corporate policy statement. It is likely to spark uncomfortable questions as employees seek clarification from companies struggling to navigate through issue-driven minefields. It could lead to a re-evaluation of the concept of a “social contract” between employer and employee, and whether the implicit understanding needs codifying. It could even end up being a trigger for a battle for the soul of corporations, and the meaning of value.

These are difficult times, in more ways than we can possibly realize. And the coming change in mores and expectations will be deeper than most anticipate.

BitMEX had a really bad day

The U.S. Commodity Futures Trading Commission (CFTC) and federal prosecutors have started the quarter off with a bang, charging crypto trading platform BitMEX with facilitating unregistered trading and other violations, and arresting co-founder Samuel Reed.

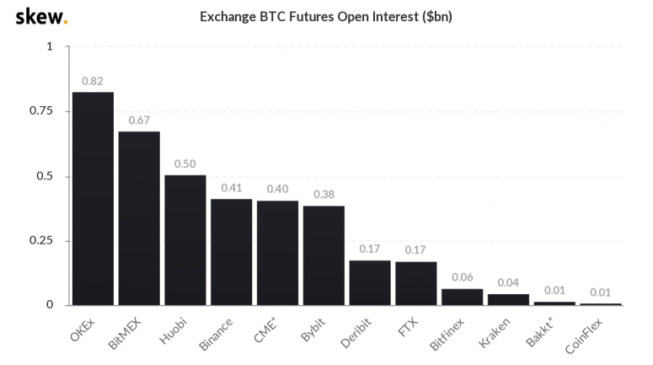

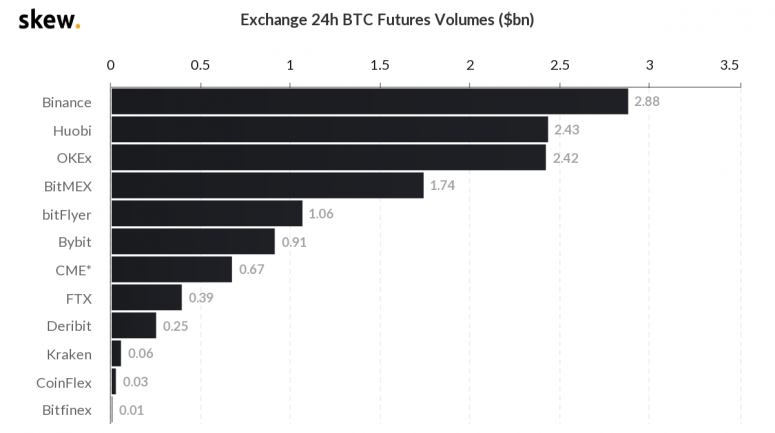

This is a big deal, as BitMEX is one of the industry’s largest trading platforms. In 2016, it introduced a derivative known as perpetual swaps (futures that don’t expire) to the market, with up to 100x leverage, and for many years was the market leader in terms of derivative volume and open interest.

This is an example of how market infrastructure can affect prices in a young asset class. In 2014, Mt. Gox – then the largest bitcoin exchange with approximately 70% of market share – collapsed, revealed a gaping hole where custodied bitcoin should have been. The bitcoin (BTC) price dropped by almost 50%, recovered a bit and then fell even further over the next few months. It took over two years to recover from the confidence blow.

As recently as a couple of years ago, BitMEX was the largest derivatives exchange, and this week’s news could have had a similar effect given the relatively high leverage in its contracts. Yet the BTC price initially fell almost 4% on the news, which is not insignificant, but nowhere near the systemic jolt many expected. It then recovered 1.5% before being blindsided by other market-shaking non-crypto-related news.

In other words, BitMEX’s run-in with the law will have an impact, but it is unlikely to be material.

In recent months, BitMEX lost its dominant position to OKEx, Huobi and Binance, and now ranks fourth in terms of daily volume and second in terms of open interest. Even if BitMEX ends up closing, the market repercussions will be felt, but will not be systemically damaging, as there are alternative trading venues.

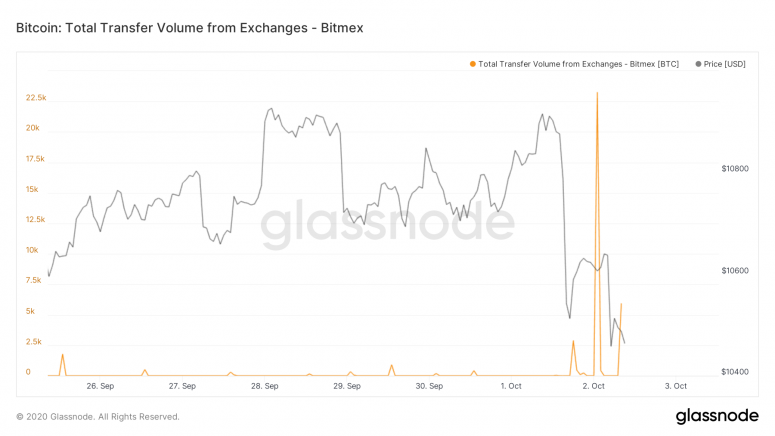

What’s more, while the domain name could be seized and withdrawals impeded (the exchange requires three of the four authorized signatories to approve withdrawals, and so far one has been arrested), BitMEX is unlikely to close – at time of writing, withdrawals were proceeding without hitch, and were significant but not catastrophic for the exchange.

Even more importantly, this news does not change the fundamentals of bitcoin. It may affect trading volumes as positions are closed and reopened elsewhere. But the underlying technology and the potential use case remain intact.

And, rather than weaken confidence in crypto market infrastructure, this news is likely to enhance it. One of the reasons cited by the SEC for its rejection of all bitcoin ETF proposals so far is the lack of surveillance on significant offshore exchanges. This action by the CFTC feels like part of a “bring out the broom” initiative that will improve the rigor and oversight of market players, which should boost institutional confidence and product range. It could even be a tentative step towards a bitcoin ETF approval.

3 things from Q3

As we are now into the final stretch of what has been a spectacularly tumultuous year, it’s time to look back at a few of the recent developments in crypto asset markets that I find particularly interesting. There are so many to choose from, as the speed of progress has been astonishing. Our CryptoX Quarterly Review 2020 Q3, which dives into some of the main market drivers, is out on Monday – keep an eye out for it in our Research Hub.

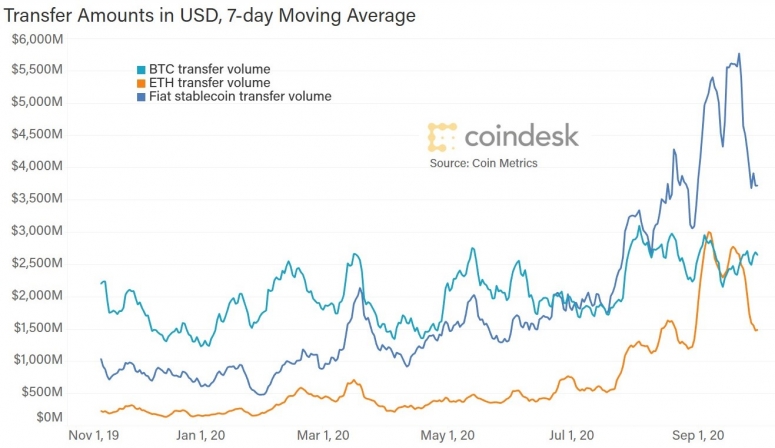

1) Stablecoins were the breakout protagonist in terms of market activity, and not just in terms of market cap growth.

Earlier in Q3 the on-chain transfer value of fiat-backed stablecoins passed that of bitcoin (BTC) for the first time. While there are many factors at play here, this does indicate a growing reliance on stablecoins as the industry’s settlement token.

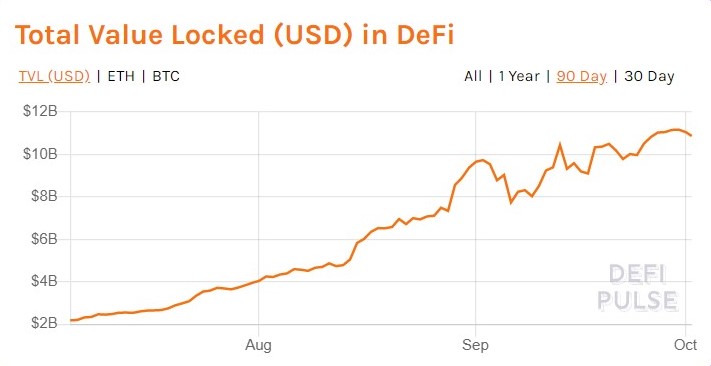

2) The value that has flowed into decentralized finance (DeFi) applications has astounded even those of us who work in the industry. I don’t talk much about DeFi in this newsletter, since it has so far been very niche and, well, untested. But it’s starting to affect the markets I do focus on.

While volumes have exploded (not literally, obviously, and it says a lot about the mood this year that I even have to clarify that), they are still small in terms of comparative market size. What is telling is the interest that centralized platforms such as crypto exchanges are starting to pay this area. And not just centralized platforms: At an event earlier this week, Brian Brooks, acting head of the US Office of the Comptroller of the Currency (OCC), said that he believes that traditional financial institutions will have embraced DeFi technology and principles within 10 years. I agree, and given the increasingly frequent signs this process is starting, you’ll probably start to hear more about DeFi in these columns.

Perhaps you have already been following the DeFi space, because you are interested in unusual yield opportunities, or because you enjoy the wacky packaging some of these applications come in (many of which are named after food, don’t ask). If not, and you’d like to start to get ahead of the curve, here’s a good introduction.

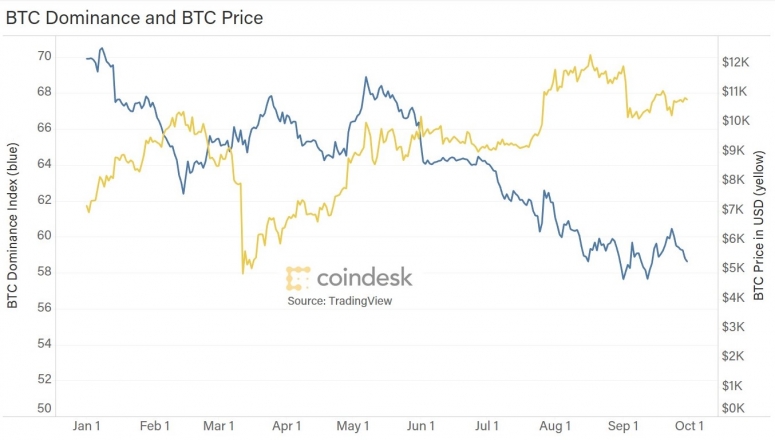

3) Bitcoin’s dominance of the crypto asset market has continued its decline. Five years ago, bitcoin was virtually all of the crypto asset market. Then came the 2017 ICO boom with a flood of new tokens surging in value, and bitcoin’s dominance fell to a low of 36%. As the bubble burst, most of the new tokens fell in value, eventually restoring bitcoin’s dominance to around 70%.

The dominance (as measured by TradingView’s BTC Dominance Index) has been steadily falling since around May of this year, largely due to the surge in the market cap of stablecoins and to the growth in DeFi tokens, not all of which were spurious memes.

Note that the index is trending downwards in spite of the upward trend in prices, which speaks to the level of growth elsewhere in crypto markets.

In other words, this is less to do with weakness in bitcoin and more to do with the expansion of the industry overall. That, in turn, is positive for bitcoin which, for many, will be the gateway crypto asset, the one that investors try out first.

Anyone know what’s going on yet?

Bitcoin yet again exhibited its split personality this week. I had a chart all ready to share with you that showed that its correlation to gold had been heading up for most of the quarter – and then Trump’s positive COVID test results sent gold higher while bitcoin headed lower. True, bitcoin had already had a shock earlier that day from the BitMEX indictment, and the slump could well have been continuing jitters from that. But it’s not unreasonable to expect market-shaking news like the President of the United States possibly being seriously ill (as far as we know, he only has light symptoms so far) to spark a rush to safety. It seems that the market is not yet convinced that bitcoin is a “safe haven” like its analog comparison.

Trump’s COVID test result seemed to have more of an impact on markets than Tuesday night’s debate, which says a lot about the debate’s inefficacy in moving the needle on divided allegiances. Zooming out, this is bewildering considering what its viciousness said about American democracy, and the importance of the election outcome. Unless, of course, the outcome of the election isn’t important at all? Like I said, bewildering.

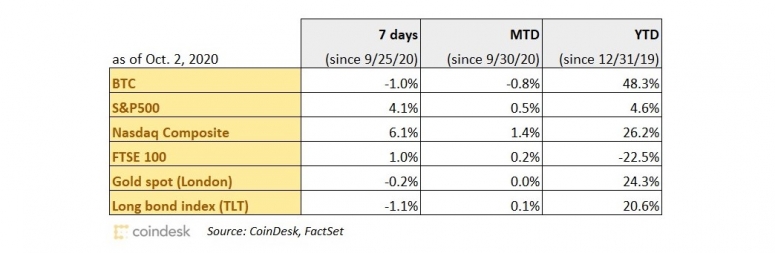

Bitcoin had a weak September (-8.4%) and has not exactly started off on a good foot in October. It did, however, achieve a positive record: it has closed above the $10,000 mark for its longest streak of 66 days and counting. This is significant inasmuch as this long a stretch above that psychological barrier hints that $10,000 has become the new price floor. Of course, floors have been broken before …

CHAIN LINKS

Cryptocurrency exchange Bitfinex has started trading perpetual contracts that track two European equity market indices and settle in the stablecoin tether. TAKEAWAY: You’ve often heard me talk about how I believe crypto assets will have a profound impact on traditional capital markets. Here is an example of how it will happen: We have a crypto exchange offering a derivative developed for the crypto markets to bet on movements in traditional indices. And to top it all off, it settles, not in fiat but in a fiat-backed stablecoin. Another notable aspect is the leverage – 100x is insanely risky, and is a feature largely limited to crypto exchanges. Few traders avail themselves of that much risk, however, as experienced market professionals know that it’s not wise.

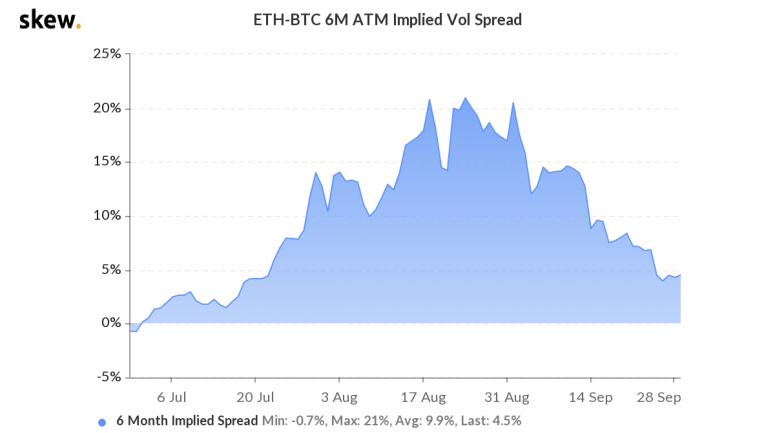

The spread between the six-month implied volatility (IV) for ether (ETH) and bitcoin (BTC), a measure of expected relative volatility between the two, fell to a 2.5-month low of 4% over the weekend, according to data source Skew. TAKEAWAY: This could mean that traders expect ETH to act more like BTC going forward. The ETH futures market is still immature, however, and the signals are not yet that reliable.

Arjun Balaji of Paradigm wrote an excellent overview of crypto asset market progress over the past two years, with a look at what needs to happen next: principally, major improvements in capital efficiency (which is gearing up with the emergence of institutional-grade prime brokerage and crypto-native repo, among other features), and the convergence of decentralized and centralized financial functions. TAKEAWAY: I totally agree, and hats off to Arjun for putting it all so succinctly. I have two needed developments to add: greater regulatory clarity on what is and isn’t a security, to encourage innovation in investment and saving opportunities for a broader range of people; and new rules to smooth the way for the new types of securities to list and trade in a compliant manner (the INX token is a start, but it’s just scratching the surface).

On a similar theme, Jill Carlson wrote an op-ed for CryptoX that talks about how recent focus has been on innovation in crypto asset infrastructure, and how the pendulum may soon swing back to emphasize innovation in assets. TAKEAWAY: Robust infrastructure is essential for a thriving market that can attract significant levels of investor interest. But investors don’t enter our industry for the infrastructure, they do so for the assets. The pendulum that Jill refers to seems to have already begun its swing – we can see this not so much in the meme-infused DeFi assets, but more in the SEC-registered INX token that gives holders trading advantages and a share in net cash flow, and in SEC Chairman Clayton confirming that the U.S. regulator would consider authorizing a tokenized ETF (one presumably not based on crypto assets, for now).

An amended filing with the Securities and Exchange Commission (SEC) last week showed that Bitwise’s Bitcoin Fundhas raised just under $8.9 million, more than double the amount it had raised last year. TAKEAWAY: According to Bitwise’s head of research, Matthew Hougan, this is largely because of growing concern over runaway inflation. Given the new Federal Reserve policy of allowing inflation to overshoot targets (the ECB this week hinted it will follow suit), these concerns are likely to intensify.

The Atari Group, the company behind such classic video games as Pac-Man and Pong, will begin publicly selling its Atari Token (ATRI) cryptocurrency in early November. TAKEAWAY: This ERC-20 token will be used in crypto casinos, blockchain-based games and the company’s video game distribution platform. I’m not clear on the economics behind the token, but the combination of Atari, games and tokens does sound a bit like a door to a mainstream use case. But I’m not a gamer, so I might be wrong. (Speaking of which, anyone see the Netflix documentary series “High Score”? Excellent.)

Nasdaq-listed mining equipment manufacturer Ebang reported a revenue slump in 2020 H1 of over 50% from the same period in 2019. According to the company, this was largely due to pandemic-related supply chain disruptions. TAKEAWAY: Supply disruptions are no doubt part of it, but as my colleague Matt Yamamoto pointed out in this report, Ebang’s product mix was inferior to that of its competitors anyway. You can’t blame COVID-19 for everything.

CryptoX Research has a new report out, authored by my colleague Matt Yamamoto, on Silvergate Bank, which looks at its financials and its business strategy in the light of growing competition.

Podcast episodes worth listening to:

And a reminder carried over from last week that CryptoX as not one but three new podcast series that are definitely worth checking out and subscribing to:

- Money Reimagined, with Michael Casey and Sheila Warren of the WEF – for the first episode, they talk to multimedia artist Nicky Enright and University of Virginia Media Studies Professor Lana Swartz

- Borderless, with Nik De, Anna Baydakova and Danny Nelson, which covers trends impacting crypto adoption around the world

- Opinionated, with Ben Schiller – for the first episode, he interviews Nic Carter, CryptoX columnist and partner of Castle Island Ventures