Noelle Acheson is a veteran of company analysis and CoinDesk’s Director of Research. The opinions expressed in this article are the author’s own.

The following article originally appeared in Institutional Crypto by CoinDesk, a weekly newsletter focused on institutional investment in crypto assets. Sign up for free here. For a primer on crypto valuation concepts, you can download our free report here.

Most of us think we understand the term “volatility.”

We digest headlines about tense political situations around the world; we are wary of explosive chemical compounds; some of us have had relationships with their fair share of ups and downs.

“Volatility” implies sharp and unpredictable changes, and usually has negative connotations. Even when it comes to financial markets, we intuitively shy away from investments that would produce wild swings in our wealth.

But volatility, in finance, is usually misunderstood. Even the most commonly accepted calculation is often incorrectly applied.

Its desirability is also confusing. Investors hate it unless it makes them money. Traders love it unless it means too high a risk premium.

And few of us understand where it comes from. Many think that it’s the result of low liquidity*. This intuitively makes sense: with thin trading volume, a large order can push prices sharply up or down. But empirical studies show that it’s actually the other way around: volatility leads to low liquidity, through the wider spread market makers apply to compensate the additional risk of holding a volatile asset in their inventory.

(*The misconception also stems from our mistaken conflation of low liquidity and low volume – it is possible to have high volume and low liquidity, but that’s for another post.)

This confusion matters in the crypto sector.

Bitcoin’s volatility has often been cited as the reason why it will never make a good store of value, a reliable payment token or a solid portfolio hedge. Many of us fall into the trap of assuming that as the market matures, volatility will decrease. This leads us to believe in use cases that may not ever be appropriate; it can also lead us to apply incorrect crypto asset valuation methods, portfolio weightings and derivative strategies that could have a material impact on our bottom line.

So it’s worth picking apart some of the assumptions and looking at why bitcoin’s unique characteristics can help us better understand market fundamentals more broadly.

Changing uncertainty

First, there are different types of market volatility. Academic literature provides an array of variations, each with its distinct formula and limitations. Jump-diffusion models used to value assets hint at a helpful differentiation. “Jump” volatility results, as its name implies, from a sudden event. “Diffuse” volatility, however, is part of the standard trading patterns of an asset, its “usual” variation.

With this we can start to see that, when we assume that greater liquidity will dampen price swings, we’re talking about “jump” volatility.

“Diffuse” volatility, however, is a more intrinsic concept.

The standard deviation calculation – the most commonly applied measure of volatility – incorporates the destabilizing effect of sharp moves by using the square of large deviations (otherwise they could be offset and masked by small ones). But this exaggerates the effect of outliers, which are often the result of “jump” volatility. These are likely to diminish as transaction volume grows, leading to a misleadingly downward-sloping volatility graph.

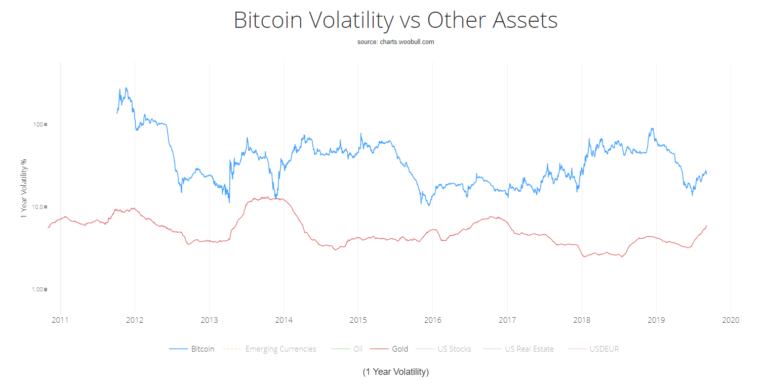

JP Koning proposes an alternative calculation that uses the deviation from the middle value rather than the average, which reduces the effect of outliers and shows a more intrinsic volatility measure. As the below chart shows, this has not noticeably decreased over the years.

Now let’s look at why this might be. A clue lies in the methods used to value bitcoin.

Fundamental value

Bitcoin is one of the few “real assets” traded in markets today, in that it does not derive its value from another asset.

What’s more, it is a “real asset” with no discernible income stream. This makes it very difficult to value. Even junior analysts can calculate the “fair value” of an asset that spins off cash flows or that returns a certain amount at the end of its life. Bitcoin has no cash flows, and there is no “end of life,” let alone an identifiable value.

So, what drives the value of bitcoin?

Many theories have been put forward, some of which we describe in our report “Crypto’s New Fundamentals.” And as the market evolves, some may rise in favor while others get forgotten or superseded.

For now, though, the main driver of bitcoin’s value is sentiment: it’s worth what the market thinks it’s worth. In the absence of fundamentals, investors try to figure out what other investors are going to think. Keynes likened this to a contest in which “we devote our intelligences to anticipating what average opinion expects the average opinion to be.”

Gold is in a similar situation, in that it is also a “real asset” with no income stream and a market value largely driven by sentiment.

So, why is its volatility so much lower?

(chart from Woobull)

(chart from Woobull)Because of “radical uncertainty.”

Changing narratives

In his book “The End of Alchemy”, Mervyn King explains that under “radical uncertainty,” market prices are determined, not by fundamentals, but by narratives about fundamentals.

Bitcoin is a new technology, and as such, we don’t yet know what its end use will be. Everyone has their theory, but as with all new technologies, no-one can be certain, which makes its narrative changeable.

Gold, on the other hand, is neither new nor a technology. It has been around for millennia, and its narrative is not uncertain. Sentiment plays an important part in its valuation, and scientists may yet uncover an innovative use for the metal that affects both demand and price. But its “story” is well established, which gives it a lower volatility profile.

For now, bitcoin’s fundamentals are its narrative, and the uncertainty about bitcoin’s “story” means that its volatility is unlikely to diminish any time soon.

A more prominent role

This matters for its eventual use case: will it always be too volatile to be used as a payment token, store of value, etc.? This in turn impacts its narrative, which affects its valuation and volatility, which affects its eventual use case. The self-perpetuating loop will eventually be broken as the sector matures and bitcoin’s role as an alternative asset class becomes more firmly consolidated – when uncertainty diminishes and its “intrinsic value” becomes easier to quantify.

But until then, its price will continue to be driven by market sentiment, which is susceptible to changeable narratives that in turn are formed by global developments and also by market sentiment.

Until then, market shifts will continue to be amplified in either direction, whatever the trading volume.

Rather than fret about this, we should accept and even embrace it. Increasingly sophisticated providers are working on improving the access to and interpretation of sentiment data, which strengthens our analytical tools. Crypto Twitter provides an engrossing platform to gauge the sector’s mood. And the identification of the impact of narrative and sentiment on an asset class will open up new avenues of investigation that is likely to spill over into other areas of investing.

What’s more, volatility may be inconvenient for some and uncomfortable for many. But it is also an important component of superior returns. Perhaps the tools and skills we develop to hone our bitcoin valuation techniques will enable a more masterful handling of volatility’s inherent uncertainty, and allow for a deeper appreciation of what it has to offer.

Roller coaster image via Shutterstock